Not Just a Bad Thing! Rising long-term interest rates increase interest payments on the “national debt”… but is it a plus for families?

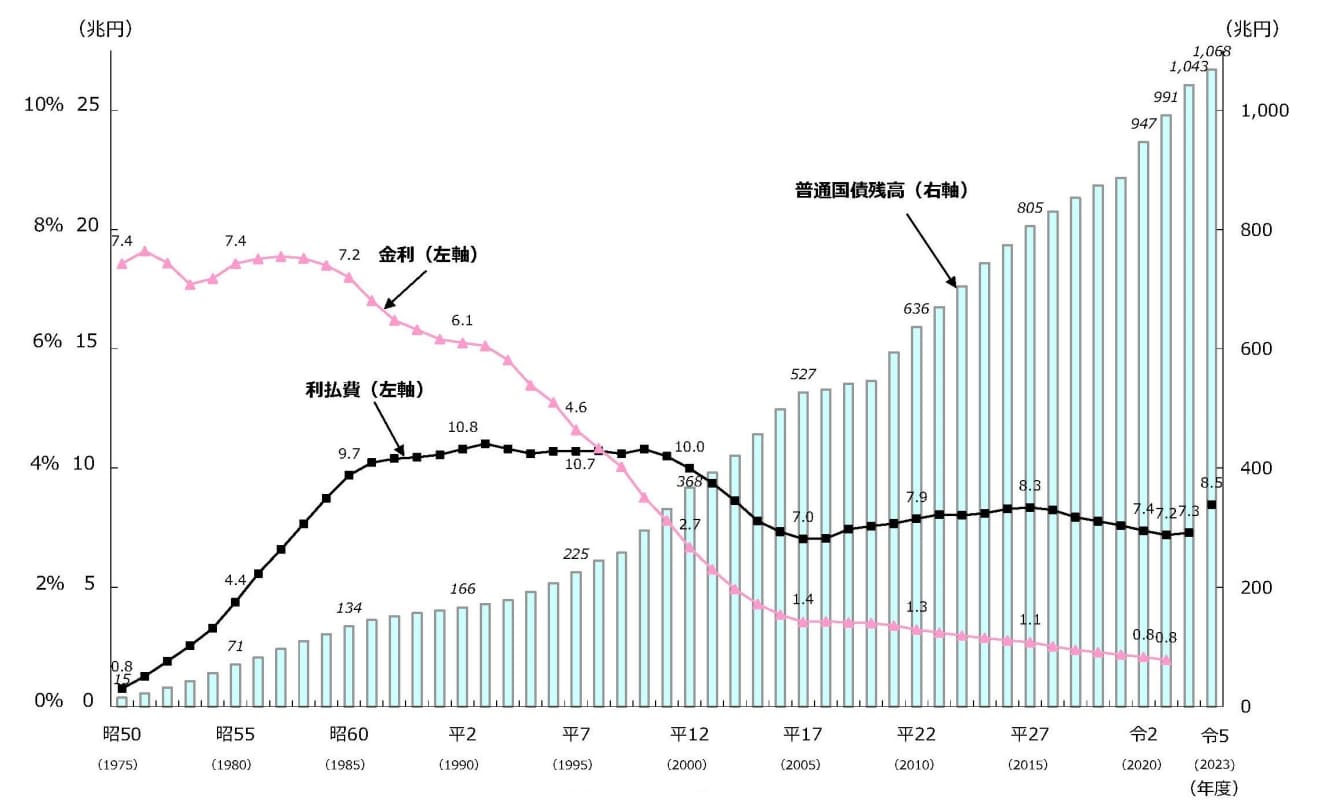

Interest Expense” for the current fiscal year is 8.5 trillion yen was expected to be…

With interest rates rising, how much debt does Japan have? According to the Ministry of Finance, the “national debt” is the total of government bonds, borrowings, and FBs, which totaled 1,275.6116 trillion yen at the end of September. Of this amount, over 1,131 trillion yen was in JGBs, most of which are called “ordinary JGBs,” the main source of funds for interest payments and redemptions being taxes, and the outstanding balance of these was over 1,027 trillion yen.

For example, a graph showing the outstanding amount of JGBs and changes in interest payment expenses and interest rates published by the Ministry of Finance shows that while the outstanding amount of JGBs has expanded due to Abenomics, interest payment expenses have been kept at around 7 or 8 trillion yen annually for the last 20 years as interest rates have been guided to lower and lower levels. For the current fiscal year, the initial plan was expected to be approximately 8.5 trillion yen.

On the other hand, the Ministry of Finance has been raising the interest rate on JGBs it issues in response to trends in the financial markets: the 10-year JGBs had been at 0.1% for several years until March 2010. Since July of this year, the rate has been 0.4%, and in October, it was raised significantly to 0.8%.

JGBs come in fixed-rate and floating-rate types, with fixed-rate maturities varying from 2 to 40 years. When JGBs reach their maturity dates, they are often refinanced. The cost of interest payments on fixed-rate JGBs is determined by the level of interest rates at the time of issuance, and future refinancing will increase the cost of interest payments due to rising interest rates.

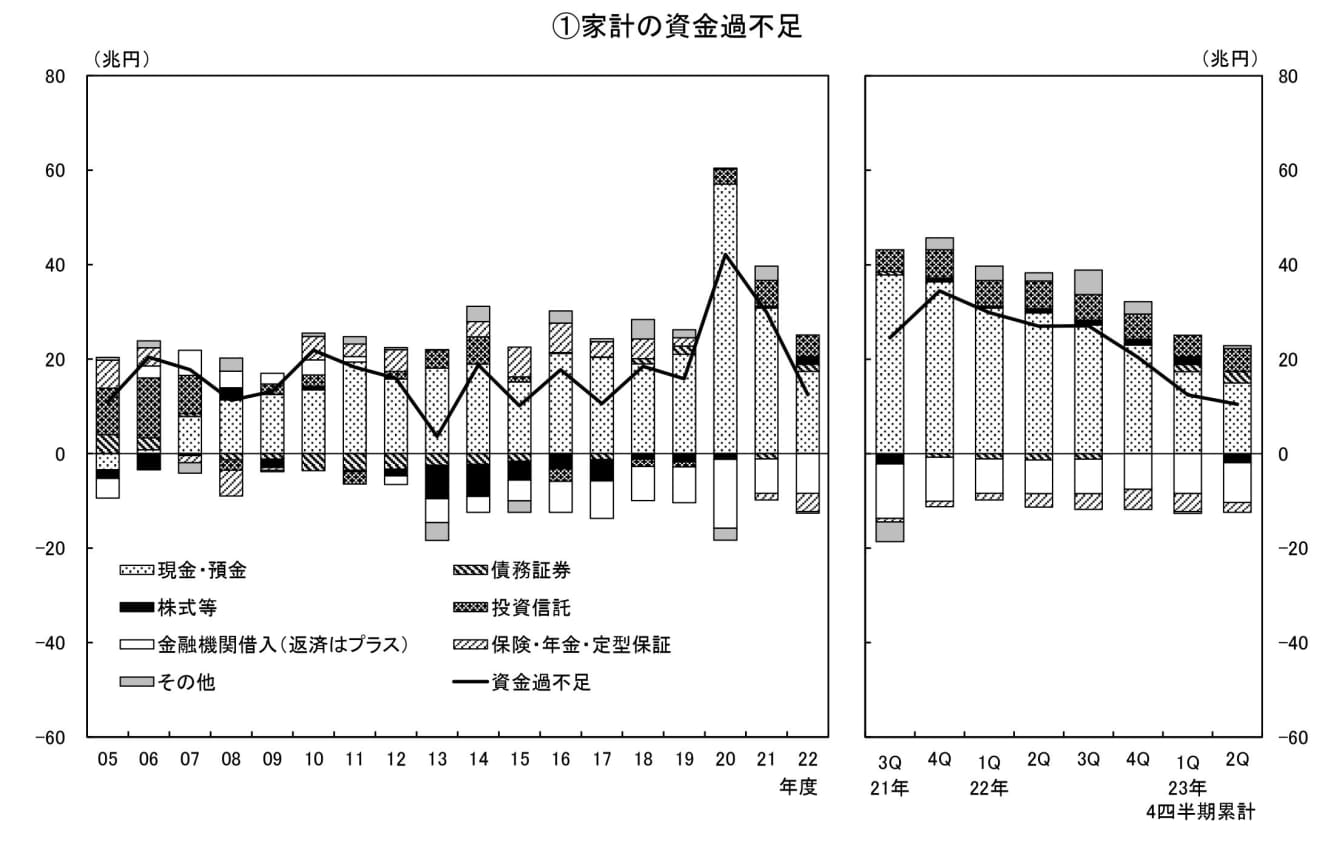

Is the household sector, which has more “deposits” than “debts,” on the contrary positive?

Some experts disagree with this pessimistic view of public finances, pointing out that there are ways to curb the issuance of government bonds. Taro Saito, Director of Economic Research at Nissay Research Institute, is one such expert. He believes that the BOJ’s decision to allow long-term interest rates to exceed 1% “came a bit too soon,” and that it “clearly shows that the YCC,” which has been guiding interest rates to ultra-low levels, has “become a mere skeleton. He then added, “The BOJ has been holding down interest rates.

I think the BOJ will continue to hold down interest rates. If left to nature, interest rates could rise to 2% or 3%, but the impact on the economy would be too great. I think the BOJ will continue to buy JGBs and keep interest rates at the 1% level for the next few years.”

Furthermore, Mr. Saito says that although interest rates will rise and interest expenses on JGBs will increase compared to the zero-interest-rate era, “we will just have to accept it. On the other hand, unlike the government and corporate sectors, which are heavily in debt, the household sector has more deposits than debts, and the rise in interest rates will be positive for the household sector as a whole, he said.