Unrealized profit” exceeds 30 trillion yen due to the weak yen…Reason to believe that the “special foreign exchange market” can cover the funding for the “1,030,000 yen barrier” of the National Democratic Party of Japan.

6 trillion yen” valuation gains in one year…why are they not returned to the people suffering from rising prices due to the weak yen?

The debate over the abolition of the “1,030,000 yen barrier” is hot. The main actor is the Democratic Party of Japan (DPJ), but the party has come under increasing criticism for not clearly specifying the source of revenue for the tax cut. In order to gain the public’s understanding, it is time for the party to present a solid source of revenue.

The most promising candidate for the source of funds is the “Special Account for Foreign Exchange Funds,” or the “Foreign Exchange Special Account. The depreciation of the yen has generated approximately 6 trillion yen in valuation gains (i.e., unrealized gains) in one year, totaling more than 30 trillion yen. The total amount exceeds 30 trillion yen, which should be returned to the people who are suffering from the rising prices of commodities due to the weak yen, but it is still being preserved. Why is it not being returned to the people? What are “unrealized gains on foreign exchange special meetings” in the first place? We ask an expert.

There is strong criticism of the abolition of the “1.03 million yen barrier” advocated by the People’s Democratic Party of Japan (KDP). Most of them dismiss it as “irresponsible” for not providing a revenue source for the tax cut. The government and the LDP have estimated that raising the income tax deduction to 1.78 million yen, which the KDP advocates, would reduce national and local tax revenues by 7.6 trillion yen, but the criticism of irresponsibility has followed them throughout the years because of the close attention paid to the statement by a senior KDP official that “the government and ruling party should be responsible for the financial resources. As a result, newspapers and television stations began to report on the situation.

As a result, when newspapers and television covered the issue, opinions such as “taxes will eventually be raised to make up for the lost revenue” and “administrative services by local governments will be reduced, lowering the standard of living” became prominent (some TV commentators said that “garbage collection will stop”). ) The pattern has been to conclude with the conclusion that the policies are “a popularity contest for the sake of elections.

If one listens to the explanation of Yuichiro Tamaki, the representative of the People’s Democratic Party of Japan (who has been suspended for three months due to an adulterous affair), it is clear that criticism of the government in terms of financial resources is misguided. The main reason is that the elimination of the “1,030,000 yen barrier” is not so much a tax cut as an “inflation adjustment” of income taxes to refund overcharged taxes.

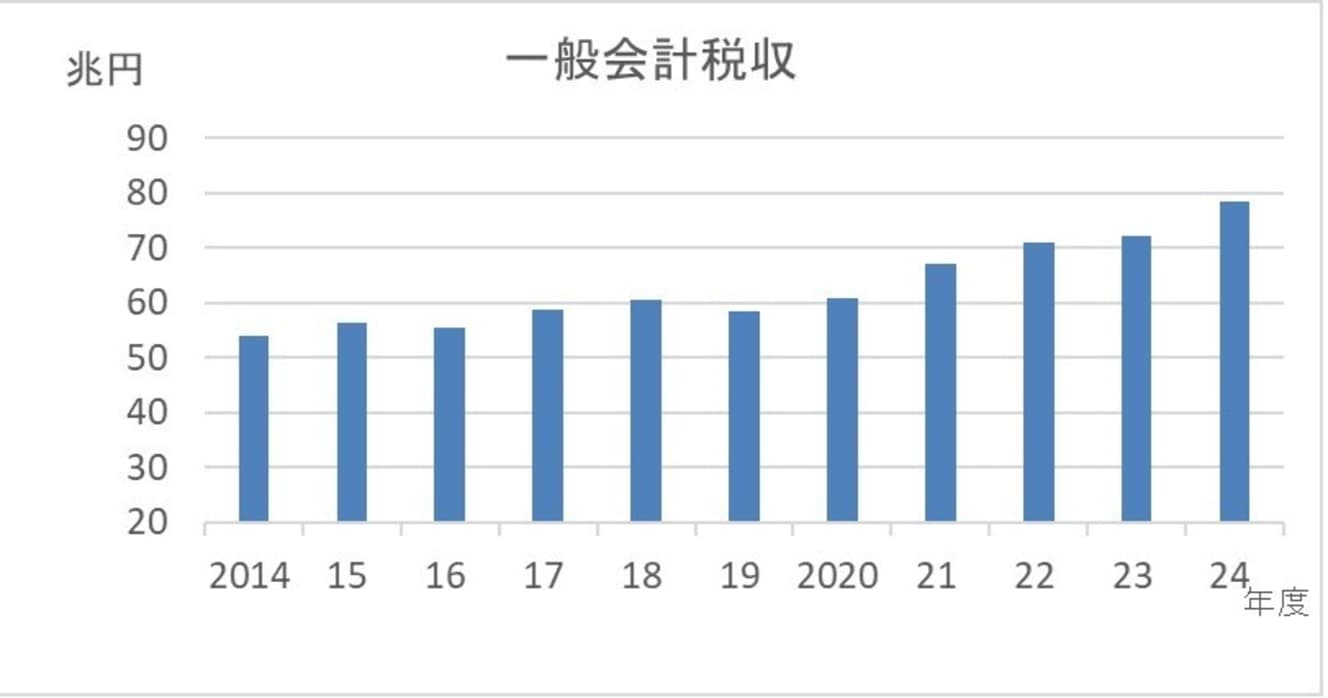

Japan’s tax revenues have been increasing for the past several years, and general account tax revenues have been at record highs for four consecutive years from FY 2008 to FY 2011. The main reasons for the increase in tax revenues are economic growth and rising prices. Particularly under inflationary conditions, income taxes tend to increase at a faster pace than price and wage growth, a phenomenon known as “bracket creep. This phenomenon is called “bracket creep.” Under bracket creep, income tax increases are larger than wage increases, and this is also known as a “hidden tax increase.

If bracket creep is left unchecked, prices will only rise and the benefits of rising incomes will not be passed on to households, possibly breaking the “virtuous cycle of wages and prices” as the Bank of Japan calls it. In order to prevent this, the DPJ’s argument is that the tax minimum should be raised in order to return the “too much” income tax to households. I would venture to say that the funding for the tax cut already exists in the form of tax revenue.

In order to eliminate bracket creep, “inflation adjustment” is a common-sense policy that flexibly revises the income tax minimum and the applicable category of tax rates in line with inflation. Germany and France have already implemented this policy recently due to the strong inflationary trend worldwide over the past few years, and in the U.S., it is customary to review it annually.

In Japan, inflation adjustment has not been implemented since 1995, but since around ’23, there have been scattered claims, mainly by economists, that it is necessary to respond to bracket creep. In other words, the elimination of the “1.03 million yen barrier” is a perfectly legitimate policy that emerged in the midst of this trend.

The Diet session from February to March is the critical point for “tax reform

This kind of argument has not been covered at all in the wide variety of news programs. Rather than trying to come up with difficult theories, it would be more appealing to viewers if they criticized the government for being irresponsible as a public party in not providing a revenue source! is more appealing to viewers and, unfortunately, more persuasive. As a result, the viewers are led to cite Greece, which is in a completely different economic situation from Japan’s current situation and is in the midst of a financial collapse, and to offer such absurd explanations as, “Garbage collection will be stopped.

This situation cannot be overlooked. The KDP is expected to submit a tax reform bill for Reiwa 2025 at the ordinary session of the Diet, which starts on January 24 this year, and a debate will probably take place in the Diet. The bill to raise the income tax deduction to 1.23 million yen was proposed by the ruling Liberal Democratic Party and New Kōmeitō, but not decided by the Diet. With the support of public opinion, there is room for a tax reform similar to the DPJ’s proposal, since the House of Councillors election will be held in July and the ruling party cannot ignore the trend of public opinion.

However, it will be difficult to win over public opinion with just the right arguments alone, as mentioned above. Representative Tamaki seems to be taking this point into consideration, and in a program on which he appeared, he began to cite “tax revenue upswing,” “non-tax revenue,” and “reduction of expenses” as sources of revenue. However, he has not been flagging in his criticisms, such as that “the tax revenue upswing will not be a permanent source of revenue. This is because the old media cannot easily reach the explanation of inflation adjustment.

Another bad move is the statement made on an Internet program that “the government may issue bonds to finance the budget,” which is also a bad idea. This is also a bad move, as it is likely to generate criticism that the government’s finances will deteriorate further and further, and that it will end up resorting to borrowing money.

Let me emphasize here that issuing JGBs makes sense. In addition to bracket creep, the fiscal situation is improving significantly due to increased corporate tax and consumption tax revenues. The government’s proposed budget for FY 2013 is expected to bring new JGB issuance to around 28.6 trillion yen, the lowest level in 17 years and the first time in four consecutive years that the initial budget has been below 30 trillion yen. On an initial budget basis, it has been below the previous year’s level for four consecutive years. There is plenty of room for JGB issuance (it is a mistaken perception that JGBs are national debt to begin with, but that is not the issue here).

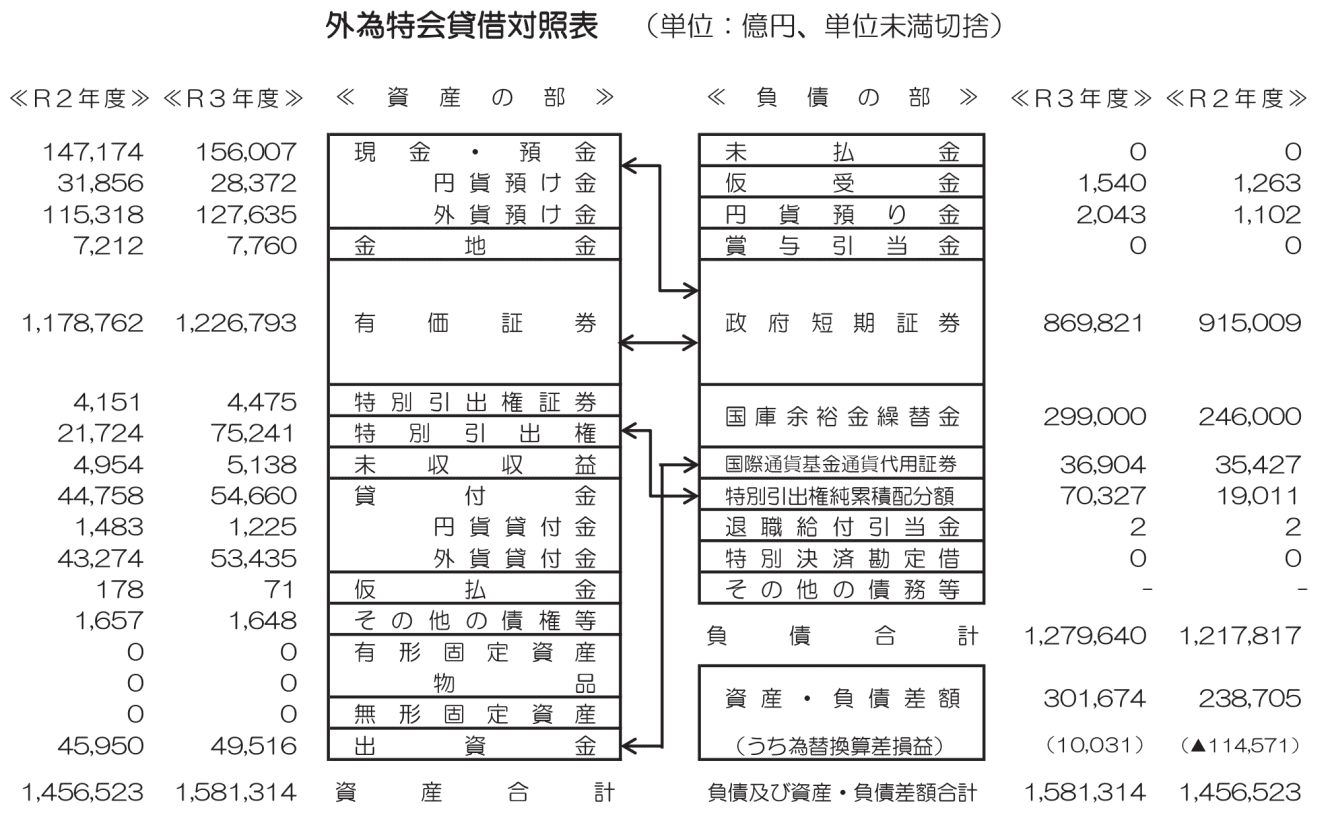

So, it is not as if there are no financial resources. The “Special Account for Foreign Exchange Funds” (hereinafter referred to as the “Foreign Exchange Special Account”) is the most promising source. The “Foreign Exchange Fund Special Account” (hereinafter referred to as the “Foreign Exchange Fund Special Account”) is like a “war chest” for intervening to stabilize the foreign exchange market in the event of a sudden change in the market, and a huge amount of money is being held in this account. As of the end of March 2010, the total amount was approximately 158 trillion yen.

In fact, the “non-tax revenue” that Representative Tamaki refers to is the “investment profit” of the Gaikai. The Foreign Exchange and Foreign Trade Special Account generates huge surpluses (i.e., investment gains) every year. According to the Ministry of Finance’s “Special Account Guidebook (Reiwa 2023 edition), the total amount for FY 2010 was approximately 3.5 trillion yen. However, about 2.8 trillion yen of this amount was transferred to the general account in FY 2011, 1.2 trillion yen was used for defense expenditures, and about 500 billion yen was transferred to the Special Account for the Government Debt Consolidation Fund. Even so, there is still a surplus, and every year the surplus is used as a source of revenue, but to be honest, one cannot deny the impression that this is “weak” in terms of gaining the public’s understanding.

Unrealized profits of the “Foreign Exchange Special Account” exceeding 30 trillion yen

What we would like to focus on here is “unrealized profit. As of the end of March 2010, approximately 30 trillion yen was recorded as the “difference between assets and liabilities” on the balance sheet of the Foreign Exchange Special Account. This is an increase of about 6 trillion yen in the year since the end of March 2009, and taking into account the current exchange rate, it is estimated to be at least 35 trillion yen. This is a whole lot of money that can be used as a financial resource.

There are objections to this. The main objection is that the U.S. will not allow it because it would effectively be a currency intervention to sell dollars and buy yen, and Finance Minister Suzuki has made a similar statement. Most of the assets of the Foreign Exchange Special Committee are U.S. Treasury bonds. Unrealized gains are generated when the yen depreciates against the U.S. dollar compared to when the U.S. Treasury bonds were purchased. The logic is that this is foreign exchange intervention itself. However, this raises several questions.

It is true that the Biden administration has spoken out against Japanese currency intervention. However, President-elect Trump has consistently expressed concern about the yen’s depreciation (in April ’24, he posted on a social networking site that it was “a disaster for the US” following the yen’s first depreciation in about 34 years). While he will not allow foreign exchange intervention to induce the yen to depreciate, he may be more receptive to a “yen conversion” to convert dollars into yen in the direction of yen appreciation.

Also, they will not convert 7 to 8 trillion yen at a time. If the US Treasuries are sold little by little, making a profit of 600 to 700 billion yen each month, there should be almost no impact on the exchange rate.

Furthermore, it is anticipated that some will argue that the sale of U.S. Treasuries itself will not be approved by the U.S. government. In that case, there is another way. If the Gaikai sells the U.S. Treasury bonds to the Fiscal Investment and Loan Special Account, a separate special account, at market value, and then buys them back from the Fiscal Investment and Loan Special Account at market value, the unrealized gains on the Gaikai’s balance sheet will become realized gains. This would eliminate the need to sell U.S. Treasuries in the financial markets. Since tens of trillions of yen are exchanged between the special accounts every year, this is not a tricky method at all.

In addition, the balance sheet of the special account for foreign exchange will show a decrease in unrealized gains, and U.S. Treasuries on a market value basis will be recorded, but since the U.S. Treasuries will be held until maturity, there will ultimately be no loss (there is a possibility of a valuation loss in the middle before maturity, but that is the case for other U.S. Treasuries as well).

Don’t miss this historic opportunity to “end deflation!

Some may argue that since it is only an unrealized gain, “it cannot be a permanent source of revenue. However, there is a strong possibility that the inflation adjustment does not need to be a permanent source of revenue. According to Toshihiro Nagahama of the Dai-ichi Life Institute, using the Cabinet Office’s “medium- to long-term economic and fiscal calculations,” in the “growth transition case” in which stable growth above 1% in real terms is secured, “¥7.6 trillion can be raised if the GDP deflator stays at +0.6-0.7%.

Growth exceeding 1% in real terms” and “GDP deflator +0.6-0.7%” are not major hurdles. In other words, there is a strong possibility that tax cuts can be continued as long as the government provides financial resources for the next two to three years. To begin with, the government’s estimate of a 7.6 trillion yen decrease in tax revenues does not take into account the increase in tax revenues that will result from economic growth through increased consumption and labor supply due to the tax cuts. The decrease in tax revenues should be much smaller.

It is often claimed that “most of the tax cut will go to savings,” but this is thought to be limited to temporary “disbursements” such as “special flat-rate benefits. The increase in disposable income resulting from the increase in income tax deductions is permanent, and most of it is likely to go to consumption.

According to the 2024 Labor Economy Analysis by the Ministry of Health, Reiwa, the average propensity to consume, which indicates the percentage of permanent disposable income that goes to consumption, is 86% (in 2011). In other words, nearly 90% goes to consumption. The increase in personal consumption is expected to boost GDP significantly.

The DPJ’s proposal also has its flaws, if one were to go into detail. Even if the income tax deduction is revised, there are still “barriers” in the social security system that prevent a drastic solution, and various other criticisms remain. However, it is simply a matter of first resolving the highest priority issues and then correcting any glitches as they arise.

As stated in the aforementioned Cabinet Office document, “Japan’s economy is now facing a once-in-a-lifetime historic opportunity to completely break free from deflation and realize a growth-oriented economy.” The unrealized gains in the foreign exchange market are one of the few by-products that the people of Japan have gained in exchange for deflation. If they do not use it now, when will they use it?

Interview and text by: Kenji Matsuoka

After working as a money writer, financial planner, and market analyst for a securities company, Matsuoka became independent in 1996. He writes articles on finance and asset management mainly for business and economic magazines. Author of "A Textbook for the First Year of Robo-Advisor Investing" and "Understanding with Rich Illustrations! Cashless Payments: The Book That Will Definitely Benefit You".

PHOTO: Afro