Unrealized profit” exceeds 30 trillion yen due to the weak yen…Reason to believe that the “special foreign exchange market” can cover the funding for the “1,030,000 yen barrier” of the National Democratic Party of Japan.

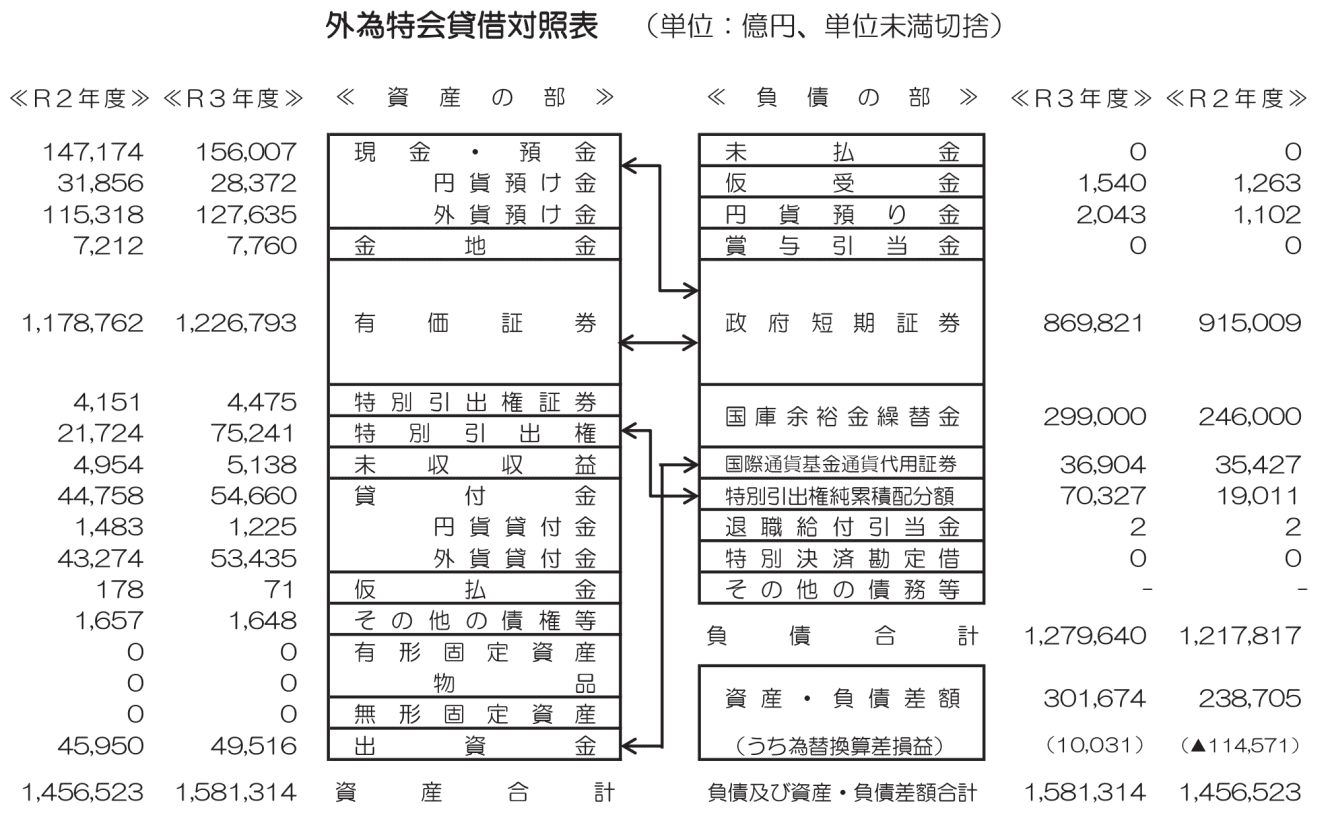

So, it is not as if there are no financial resources. The “Special Account for Foreign Exchange Funds” (hereinafter referred to as the “Foreign Exchange Special Account”) is the most promising source. The “Foreign Exchange Fund Special Account” (hereinafter referred to as the “Foreign Exchange Fund Special Account”) is like a “war chest” for intervening to stabilize the foreign exchange market in the event of a sudden change in the market, and a huge amount of money is being held in this account. As of the end of March 2010, the total amount was approximately 158 trillion yen.

In fact, the “non-tax revenue” that Representative Tamaki refers to is the “investment profit” of the Gaikai. The Foreign Exchange and Foreign Trade Special Account generates huge surpluses (i.e., investment gains) every year. According to the Ministry of Finance’s “Special Account Guidebook (Reiwa 2023 edition), the total amount for FY 2010 was approximately 3.5 trillion yen. However, about 2.8 trillion yen of this amount was transferred to the general account in FY 2011, 1.2 trillion yen was used for defense expenditures, and about 500 billion yen was transferred to the Special Account for the Government Debt Consolidation Fund. Even so, there is still a surplus, and every year the surplus is used as a source of revenue, but to be honest, one cannot deny the impression that this is “weak” in terms of gaining the public’s understanding.

Unrealized profits of the “Foreign Exchange Special Account” exceeding 30 trillion yen

What we would like to focus on here is “unrealized profit. As of the end of March 2010, approximately 30 trillion yen was recorded as the “difference between assets and liabilities” on the balance sheet of the Foreign Exchange Special Account. This is an increase of about 6 trillion yen in the year since the end of March 2009, and taking into account the current exchange rate, it is estimated to be at least 35 trillion yen. This is a whole lot of money that can be used as a financial resource.

There are objections to this. The main objection is that the U.S. will not allow it because it would effectively be a currency intervention to sell dollars and buy yen, and Finance Minister Suzuki has made a similar statement. Most of the assets of the Foreign Exchange Special Committee are U.S. Treasury bonds. Unrealized gains are generated when the yen depreciates against the U.S. dollar compared to when the U.S. Treasury bonds were purchased. The logic is that this is foreign exchange intervention itself. However, this raises several questions.

It is true that the Biden administration has spoken out against Japanese currency intervention. However, President-elect Trump has consistently expressed concern about the yen’s depreciation (in April ’24, he posted on a social networking site that it was “a disaster for the US” following the yen’s first depreciation in about 34 years). While he will not allow foreign exchange intervention to induce the yen to depreciate, he may be more receptive to a “yen conversion” to convert dollars into yen in the direction of yen appreciation.

Also, they will not convert 7 to 8 trillion yen at a time. If the US Treasuries are sold little by little, making a profit of 600 to 700 billion yen each month, there should be almost no impact on the exchange rate.

Furthermore, it is anticipated that some will argue that the sale of U.S. Treasuries itself will not be approved by the U.S. government. In that case, there is another way. If the Gaikai sells the U.S. Treasury bonds to the Fiscal Investment and Loan Special Account, a separate special account, at market value, and then buys them back from the Fiscal Investment and Loan Special Account at market value, the unrealized gains on the Gaikai’s balance sheet will become realized gains. This would eliminate the need to sell U.S. Treasuries in the financial markets. Since tens of trillions of yen are exchanged between the special accounts every year, this is not a tricky method at all.

In addition, the balance sheet of the special account for foreign exchange will show a decrease in unrealized gains, and U.S. Treasuries on a market value basis will be recorded, but since the U.S. Treasuries will be held until maturity, there will ultimately be no loss (there is a possibility of a valuation loss in the middle before maturity, but that is the case for other U.S. Treasuries as well).