NISA Credit Card Accumulation Points Drop: Time to Switch Brokerages?

New NISA has been in operation for less than a year, and now it’s getting worse!

From 2023 to 2024, companies competed to attract new NISA accounts with the credit card accumulation point rewards as a key feature. However, less than a year after the start of the new NISA, multiple downgrades have emerged. Wasn’t the foundation of NISA supposed to be long-term investment? Many may feel deceived. Therefore, this article will explain the rules and precautions for switching brokerage firms.

The deterioration of credit card accumulation is malicious.

As reported multiple times by FRIDAY Digital, 2024 saw a series of negative changes to credit card services. Among them, the reduction in the point return rate for credit card savings is likely to be categorized as malicious.

In March 2024, Sumitomo Mitsui Card announced a significant revision of the point return rate starting from purchases made in November. Points will no longer be granted unless annual usage exceeds 100,000 yen (for credit cards with no annual fee). The au Pay Card reduced its point return rate from 1% to 0.5% starting with December purchases.

Credit card savings refer to a service where investment trust savings are paid using a credit card. Points are returned based on the amount saved, and the service can be used not only with NISA’s investment savings account but also with the growth investment account. If you save tens of thousands of yen, a considerable amount of points can accumulate, leading to research showing that more than half of people using the investment savings account use credit card savings.

For online brokers, the lineup of investment trusts available for purchase through NISA is nearly the same. Therefore, the point return rate for credit card savings became a major selling point to encourage account openings, and from the second half of 2023, when the new NISA was introduced, online brokers competed to highlight their high return rates. However, as mentioned, within less than a year of its launch, there was a continuous stream of negative changes.

The point redemption service resulted in a loss!

“I initially thought it wouldn’t last long since it was a service running at a loss, but I didn’t expect changes to happen this quickly.”

The surprise is clear from Kenji Matsuoka, a financial writer well-versed in credit card matters.

“After emphasizing the importance of long-term investment through NISA, they suddenly start making negative changes to the service. I understand focusing on short-term profitability, but they might lose the most important thing—the trust of their customers.” (All quotes below are from Matsuoka.)

Indeed, profitability is tight. The profit securities companies earn from investment trusts is called the agency fee and is generally one-third of the “management fee” for the investment trust. The management fee is the fee that investors pay to financial institutions while holding the trust.

For example, the management fee for Japan’s most popular investment trust, the eMAXIS Slim U.S. Stocks (S&P 500), which is very popular in NISA, is 0.09372% per year (tax included). Since it is split between the three companies: the securities company, the management company, and the trust bank (with the sales company sometimes taking more than a third), the agency fee is 0.03124%. That’s about 1/35th of 1%.

Therefore, if they offer a 1% point return, considering management costs, it is estimated that it would take around 4 to 5 years for the securities company to break even. While some of the points granted may be shared by the card company, the basic structure remains the same since the management fee itself is minimal.

“Currently, we don’t know what will happen with the securities companies offering point returns, but as long as there are points, it’s better to use them,” Matsuoka stresses. The reason is that regular investments create a steady monthly expense.

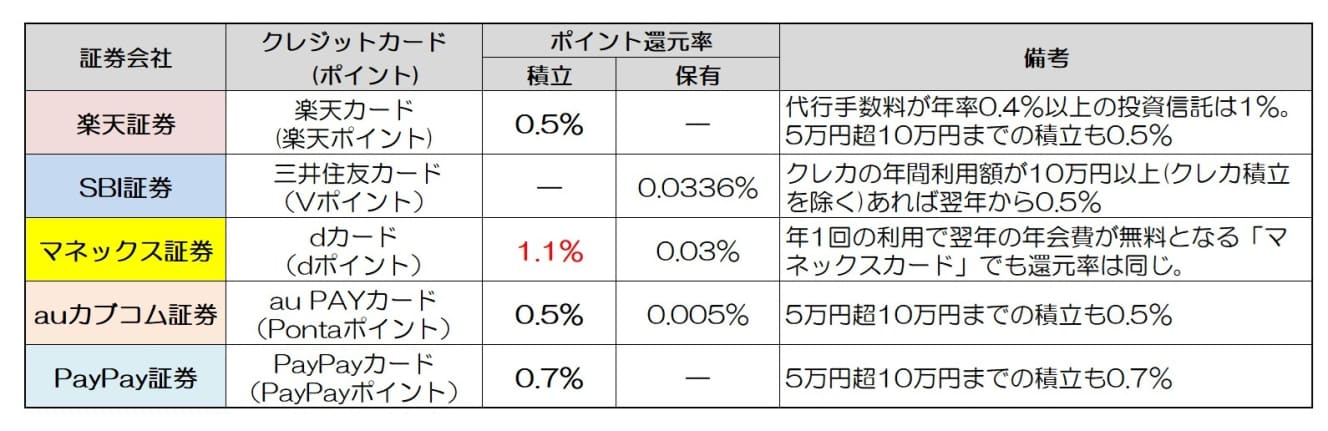

Here, I have summarized the point return rates for credit card savings at major online securities companies. Some companies grant points based on the balance of investment trust holdings, and these have been added as holding points. The return rates are based on credit cards with no annual fee, and to make comparison easier, I have set the monthly investment amount to 50,000 yen. Since the return rate for holding points varies depending on the investment trust’s brand, I have focused on the ‘eMAXIS Slim U.S. Stocks (S&P 500)’ for this comparison.

Looking at this table, it’s clear that Monex Securities is still maintaining a 1% point return rate. Moreover, their holding points are also high at 0.03%. For those living in the “Docomo economic zone,” this would likely be the top candidate. SBI Securities also has high holding points, returning nearly all of the agency fees. PayPay Securities is performing well as well, but it’s important to note that their lineup of investment trusts is limited.

Dormant account holders can switch brokerage firms!

Now, let’s confirm the rules for transferring NISA accounts for those considering switching securities companies.

There is a specific period during which NISA accounts can be changed. The period for changing is from October 1st of the previous year to September 30th of the year you wish to make the change. Therefore, at this point, it’s still possible to change your account for this year, but there is an important condition: you must not have used the NISA investment allowance yet. If you have already made investments, such as mutual fund savings or stock investments, in January within your NISA account, you cannot change your account this year.

If you proceed with the change, your current account will become inactive, and you will not be able to invest in NISA for the rest of this year (you will be able to restart investing in the new account next year). So, if you have already used your investment allowance, you will have to wait until October of this year and complete the transfer procedure for next year.

On the other hand, if you already have a NISA account but have not made any purchases this year, you can still transfer your account. In fact, many people fall into this category.

“According to the ‘NISA Account Utilization Survey’ published annually by the Financial Services Agency, as of the end of December 2023, there were approximately 21.25 million NISA accounts, and of those, around 9.07 million accounts had not made any purchases in 2023, so-called dormant accounts. This is about 43% of the total, and many of these accounts are likely still dormant after the introduction of the new NISA. For those with dormant accounts, transferring to a new account allows them to start trading again.”

NISA is not one account per person!

Additionally, as the new NISA enters its second year, there are new points to be aware of.

“It has always been said that a NISA account is one account per person, but technically, you can have one active account for investments and another NISA account that doesn’t have any investments.”

What does this mean? For example, if you already have a NISA account and have not made any purchases in that account this year, you could open a new NISA account at a different financial institution. In that case, you won’t be able to make purchases with the original NISA account, but you can still keep it open.

“To change financial institutions, you must obtain either a ‘Tax-exempt Account Termination Notice’ or a ‘Account Termination Notice’ from your original financial institution. If you submit the Tax-exempt Account Termination Notice, the NISA account will be terminated, and you will need to sell the investments or transfer them to a taxable account. However, with the Account Termination Notice, transactions in the original NISA account will be stopped, but you can leave the mutual funds and stocks there, tax-free. As a result, you will end up holding two NISA accounts: the one with the original financial institution and the new one.”

So, if someone opens a new account at a different financial institution every year, will the number of NISA accounts grow to three or four?

“Yes, it will. You can’t transfer tax-exempt assets between NISA accounts, but by making it easier to open accounts, the system becomes more flexible, and it increases convenience for users. In the future, it will be even easier to switch accounts. Already, Rakuten Securities has made the process much easier.”

Furthermore, if you terminate a NISA account and sell or transfer the financial products you held in that account to a taxable account, the corresponding lifetime investment allowance will be restored. The submission of the Tax-exempt Account Termination Notice and the sale of tax-exempt assets can be done at any time. Additionally, even if you hold multiple NISA accounts, the annual investment allowance and lifetime investment allowance will not change.

The effects of regular investment will continue as long as you don’t change your investment targets. As October approaches, account opening campaigns may be held, so those who have the time and ability to put in the effort should choose a more advantageous securities company.