FP’s estimate! “Floating-rate mortgages” to rise in October… Pitfalls of the “5-year rule” and the “125% rule

What will happen to the interest rate on the “variable rate mortgage” being repaid? ?

In October, many mortgages are expected to increase their “variable rate”. Will there be an impact on mortgages that are being repaid or not? If so, how much? Are you making the right assumptions?

If you answered, “I am going to wait and see because of the ‘5-year rule’ for variable rates. If you answered “yes,” you have a high level of mortgage literacy. When will your “5-year rule” end? One year? Or three years? Do you understand exactly how variable interest rates work, such as the “5-year rule” and the “125% rule,” which are unique to variable interest rate types?

Interest rates are now on an upward trend. If the upward trend remains unchanged, repayments will surely rise at the time the five-year rule expires. At that point, the 125% rule may be triggered and “accrued interest” may occur.

First, let’s review the “5-year rule” and the “125% rule.

These are not unified names. They are not mandated by FSA to be included in mortgage contracts, nor are they adopted by all financial institutions. In fact, Sony Bank, PayPay Bank, SBI Shinsei Bank, and others have not adopted them, hence the importance of what is in your own mortgage contract.

If you are repaying your mortgage at a variable rate, check it immediately.

Understand how variable interest rates work.

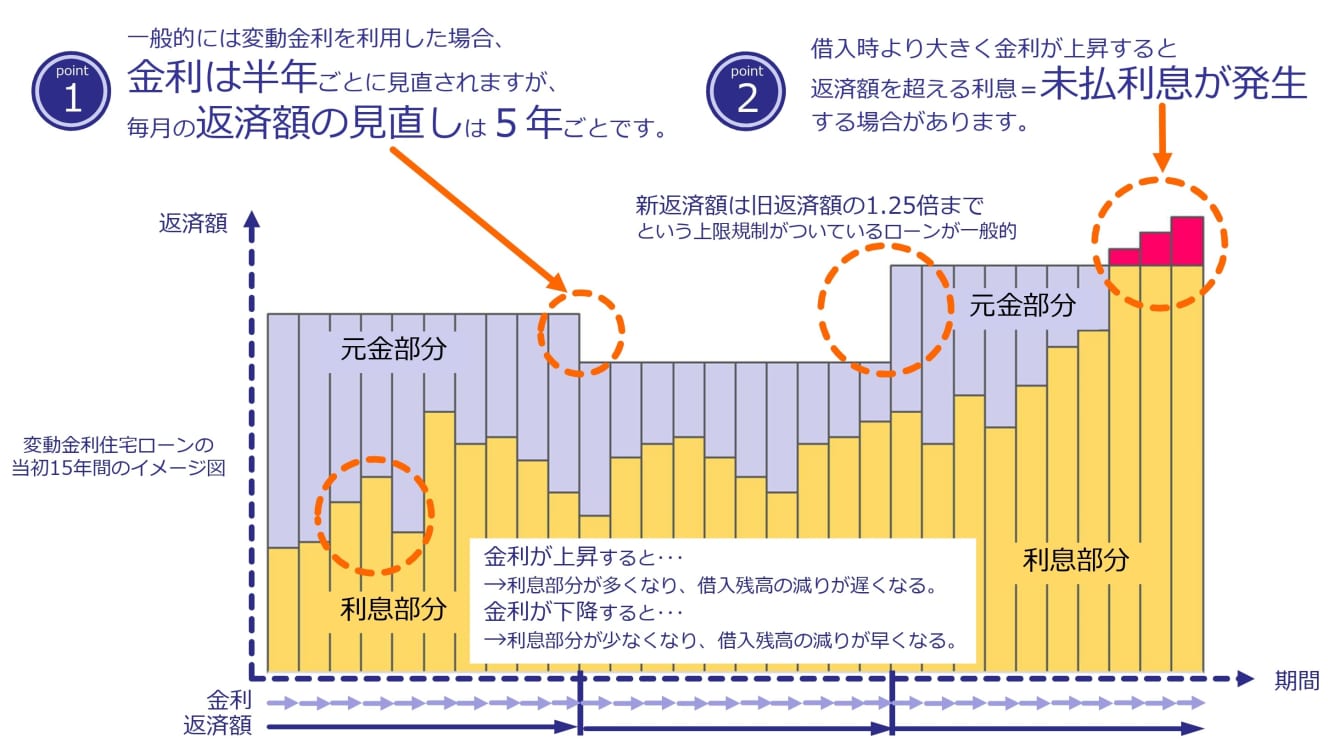

Five-year rule

The rule of reviewing the repayment amount every 5 years: The amount of repayment remains the same for 5 years regardless of interest rate fluctuations.

125% Rule

The 125% rule: When the repayment amount is reviewed in the sixth year, the new repayment amount is limited to a maximum of 1.25 times the previous amount, even if interest rates rise. However, when the repayment amount is reduced, accrued interest (accrued interest) accrues. The accrued interest is adjusted in subsequent repayment periods. The payment is not exempted.

Review” of borrowing interest rates and timing of “reflected” interest rates

At most financial institutions, mortgage rates are reviewed on April 1 and October 1 of each year based on each bank’s “Base Interest Rate”. If the review is conducted in April and October, the interest rate will be reflected in the repayment amount in July and January.

Who will be affected by the “5-year rule” this time?

The following are the cases that will be directly affected by the October interest rate hike.

- (1) New borrowers who take out a new mortgage loan and execute the loan in October.

- When the 5-year rule ends, such as when 5 or 10 years have passed since the start of repayment.

Even if you are not at a milestone of the 5-year rule, be on your guard. Even if interest rates rise, the repayment amount remains the same, but thanks to the 5-year rule, the percentage of interest payments in the repayment amount increases, and the amount allocated to principal repayment decreases.

This means that the principal amount is not decreasing, even though the monthly repayment of 100,000 yen is being made.

Many financial institutions, including major banks, use the short-term prime rate (Short-Price-Price-Plus) as an indicator for variable mortgage loans Many financial institutions raised the Short-Price-Plus in September after the Bank of Japan raised its policy rate by 0.25% at the end of July.

Mortgage rates will be affected in October. Some financial institutions have already announced their mortgage rates for October, but the major banks will announce their rates on September 30. If interest rates are revised in October, the repayment amount will be reflected in January.

Simulation】Case of a person who has passed 5 years since the start of repayment

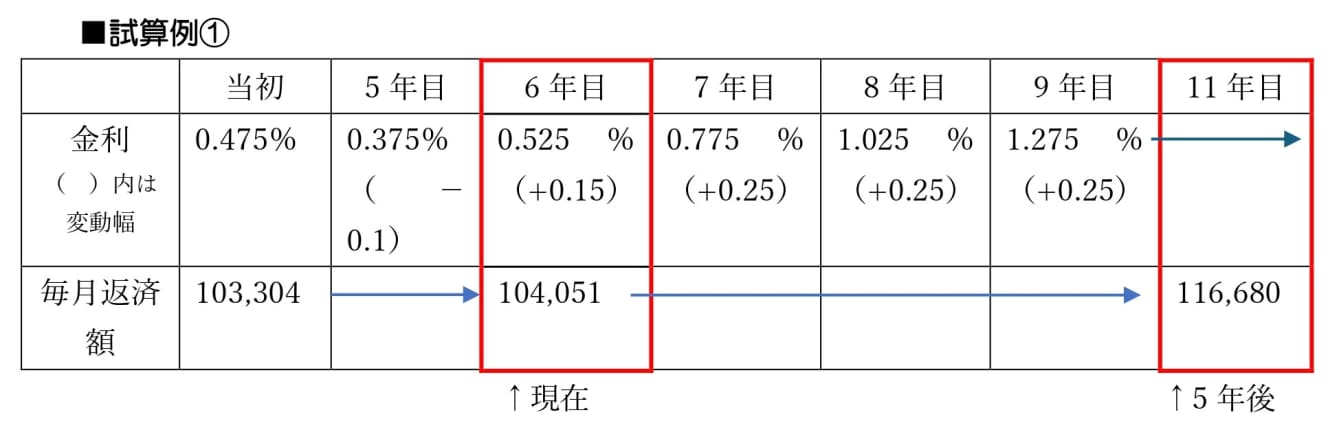

Now, let’s simulate the case where 5 years have passed since the start of repayment and the 6th payment is due on October 1.

In the case of [Sample Calculation (1)], the borrower borrowed 40 million yen five years ago at a variable interest rate of 0.475%, the interest rate was 0.375% in the middle of the loan, and the mortgage rate will be 0.525% from October, in line with the +0.15% increase in the Short-term Loan Program in September. Thereafter, +0.25% annually. The upward trend was assumed to continue for three years.

In the example of the estimation (1), the increase in the repayment amount is less than 1,000 yen. It can be said that this is an amount of money that can be handled with a little bit of daily effort. If interest rates continue to rise by 0.25% every year for three years, the repayment amount in the 11th year will be in the 110,000 yen range. This is an increase of more than 12% from the initial amount, but it amounts to a little more than ¥13,000. This is likely to be a defensive strategy to respond by reviewing household expenditures while expecting wage growth.

However, the other day, BOJ Council Member Tamura touched on the neutral interest rate in his speech at the Okayama Prefecture Finance and Economy Roundtable, saying, “Raising short-term interest rates to at least 1% in the second half of the outlook period through FY26 is necessary to contain upside risks to prices and achieve the price stability target in a sustainable and stable manner. The Bank believes that raising short-term interest rates to at least 1% in the second half of the outlook period through FY26 is necessary to contain upward price risks and achieve the price stability target in a sustainable and stable manner.

The second example is based on theassumption that the short-term interest rate will rise by 0.25% every six months for three years after the 0.15% rise in October.

In Trial Calculation Example (2), the 5-year rule is also in effect, and the repayment amount remains unchanged for 5 years. But even during that period, the ratio of the original repayment and the interest portion of the repayment amount will change according to interest rate trends.

Due to the rising trend of interest rates from the sixth year onward, the repayment amount remains the same, but the interest portion will certainly increase and the amount going to principal repayment will decrease. Then, the 11th year. The repayment amount increases by over 26,000 yen and enters the 130,000 yen level. The annual increase is estimated to be approximately 312,000 yen.

In addition, in the example (2), the 125% rule comes into effect in the 11th year, and the repayment amount is reduced to 125% of the previous repayment amount. At the same time, “accrued interest” accrues. Please pay attention to the 16th year in Trial Calculation Example (2). The upward trend in interest rates has already ended, but the repayment amount has increased. This is due to the adjustment of accrued interest.

If interest rates were to rise earlier, one might regret, “I should have switched to a fixed rate at that time. However, it is impossible to completely predict the movement of interest rates.

While the 5-year rule is in effect after the 6th year, we should examine every possible means, such as refinancing and early repayment. Interest rates are said to move fast. It is crucial not to miss the timing to take action.

If you have 10 more years left to repay your loan, please visit ……

Next, let’s consider the case where the remaining term is 10 years, the balance is 15 million yen, etc., and the 5-year rule milestone is reached as the repayment proceeds.

There seems to be no need to make a hasty move here.

It is the case where the remaining term is long and the balance is large that will be strongly affected by rising interest rates. The burden on household finances varies from person to person. Regardless of the amount of the remaining balance, we would like to make an estimate if you are using a variable type.

If the household balance is comfortable, an increase of ¥10,000 may be fine, but if the monthly income and expenses are toned and there is no margin, an increase of ¥10,000 will put the household in the red. The key point is to confirm whether the household can withstand a rise in interest rates.

If you cannot sleep at night worrying about what will happen if interest rates rise, switching to a fixed rate or reducing the remaining balance by early repayment may be an option. Refinancing to a fixed-rate mortgage is another option, but at a higher cost and with a lower priority. It is more realistic to focus on cost-oriented planning, such as changing the interest rate type at the same financial institution. Consult with the financial institution where you are currently repaying your loan.

If you are thinking of taking out a “new” loan, please visit ……

Finally, let’s consider the case of new borrowing.

In the case of a new borrower who purchases a new house and takes out a mortgage loan for the first time, there is no previous repayment amount to compare. The only thing to consider is whether or not the borrower can afford the repayment based on the household income and expenditure. In addition to variable interest rates, consider fixed interest rates and “mixed plans” that combine variable and fixed interest rates.

Also, pay attention to the time difference between the time of financial planning and the time of loan execution. The interest rate at which the actual repayment amount is calculated is the interest rate at the time the loan is executed. There must be cases where interest rates have risen since the time of financial planning. If there is a difference in interest rates, it is necessary to re-calculate as soon as possible. Let’s make sure that our finances will not suffer even if interest rates are on an upward trend. Do not underestimate the world with interest rates.

Up to 50,000 yen per month, my family will be fine.” ……Estimating the impact on household finances when interest rates rise

The BOJ’s “price stability target” is a 2% year-on-year rate of increase in consumer prices. If a 2% rate of price increase is assumed in addition to rising interest rates, the expectation of wage increases alone is not encouraging. Self-help efforts are essential.

It will be an all-out battle, including a review of household expenditures and asset management. In a world where prices will rise steadily by 2%, it is not so surprising that interest rates will be 2% plus. While one option is to forego early and switch to fixed interest rates, it is important to make a comprehensive decision based on one’s borrowing situation, household finances, and work style.

Even if interest rates rise, if the household can afford it, the increase can be absorbed by the household balance. For example, “If interest rates rise by 2%, the increase is expected to be 40,000 yen. If you can estimate the impact on your household budget when interest rates rise, you will not have to panic.

However, if interest rates rise and the household’s surplus funds are invested in mortgage repayments, the budget for retirement funds and other future needs may be reduced. Keep in mind that today’s spare funds are the funds needed in the future.

Interview and text: Izumi Oishi

Certified Senior Financial Planner CFP® by the Japan FP Association. Career consultant. After graduating from university, joined Recruit Co. Ltd. for about 15 years before establishing his own FP firm in 2001. He has been offering lectures and training courses on economic education, career design, and asset building to universities and companies, using familiar newspapers for men and women of all ages. For individuals, he provides objective financial planning and life and career planning. He was recognized by the Financial Services Agency and the Bank of Japan for his work in promoting financial literacy.