The current investment performance is greatly affected by the weak yen… “Is it safe to choose NISA and Orkan?

What should I invest in with my NISA?” — What is always mentioned in this theme is index funds such as [All Country] and [S&P500]. Internet articles and social networking sites are lined with words of praise, as if there is no other choice. However, experts point out that there is a “weak point” that has been obscured by all the high praise.

Unusual “Orcan popularity” revealed by the NISA relaunch

The renewed “NISA” started in January 2012. It has immediately had a major impact on the financial markets. The domestic investment trust market saw an excess inflow of 1,310.7 billion yen in January alone. With the addition of rising domestic and international stock markets, the total net asset value of publicly offered additional stock investment trusts in Japan (excluding ETFs) at the end of January reached a record high of 111.5956 trillion yen.

The sources of inflows were also eye-catching. The top fund inflow was “eMAXIS Slim Global Equity (All Country)” (“Orcan”) with 343.9 billion yen. This is an unusually large amount for a single month for an existing investment trust (fund), not a newly launched fund. Although it was expected to become popular, this is an unprecedented amount of money. In second place was the “eMAXIS Slim US Equity (S&P 500)” with ¥209.0 billion, which was also not far behind.

In addition to the “eMAXIS Slim” series, there are also “Global Equity” and “S&P 500” index funds sold by other companies, both of which have seen considerable inflows. In total, more than half of the approximately 1.3 trillion yen of new retail funds have flowed into these two types of index funds.

The overwhelming performance of Orcan and the S&P 500

An index fund is an investment trust that aims to invest in an index such as a stock price index. As its name suggests, the index used by Orcan is the MSCI All Country World Index, which covers the world’s stock markets, including emerging markets. And [S&P500] is the name of the index, which is composed of 500 stocks representative of the U.S. market.

What are the reasons why these two are overwhelmingly supported by individual investors among the many index funds? First of all, they have excellent past performance. Orcan’s three-year gain through the end of January 2012 was +68%, and its one-year gain was +32%. The S&P 500 has recorded a three-year increase of 91% and a one-year increase of a whopping 41%.

Given such high performance, since last year, financial experts and individual investors have been unanimously commenting in the media and on social networking services that “if you want to invest in NISA, it should be in Orcan or S&P500. This was a strong response from those who wanted to start a NISA but did not know what to invest in.

Are “weaknesses” being overlooked due to strong performance?

However, the high praise of index funds in the media and on social networking services has led some to overlook their “weak points” as index funds. Naoko Shinoda, deputy head of Rakuten Securities’ Asset Creation Research Institute and fund analyst, explains as follows.

There is no doubt that it is one of the best investment trusts for long-term accumulation investment, but it is not a panacea. However, it is not a panacea. It is important to understand the contents of the fund properly in order to overcome situations in the future when investment performance does not go as expected.

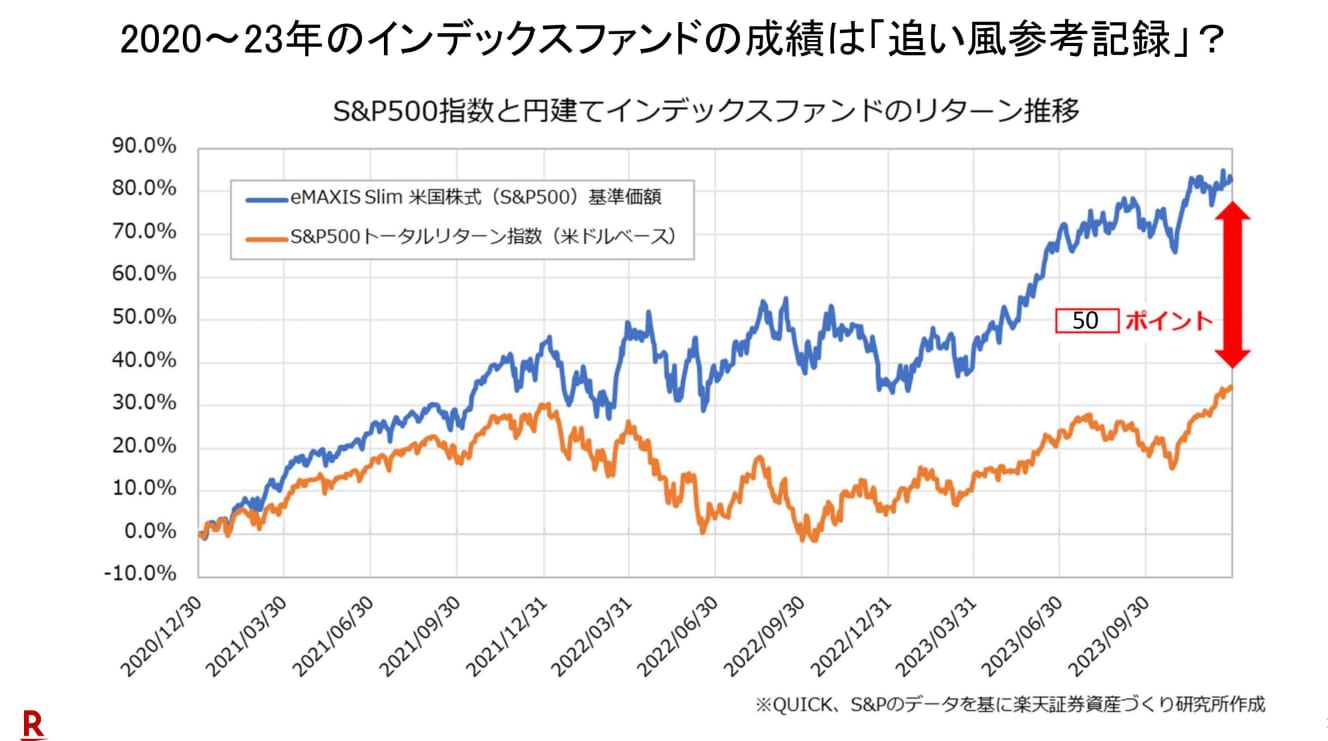

The current investment performance is a “tailwind reference record” due to the weak yen.

Therefore, the first thing to understand is “true ability. As mentioned above, the performance of [Orcan] and [S&P500] over the past few years has been overwhelming, but Mr. Shinoda points out that “it should be taken as a ‘tailwind reference record.

Major overseas equity indices such as [All Country], [S&P500], and even the New York Dow have returned 70 to 80% across the board over the past three years, and 50 to 60 points of that is actually due to the effect of the weak yen. About 3 years ago, in January ’21, the yen was in the 103-104 yen per dollar range, and it is currently around 148-150 yen per dollar.

In other words, the yen has weakened by more than 40% in three years, raising the returns of U.S. dollar-denominated index funds beyond their ability.

Surprisingly, returns for the most recent three years were higher for index funds linked to the Nikkei Stock Average and TOPIX (Tokyo Stock Exchange Stock Price Index) on a local currency basis.

He said, “I don’t deny that currency fluctuation is a source of return and one of the most appealing aspects of investing in foreign currencies, but the recent rapid depreciation of the yen has made it difficult to invest in foreign currency denominated funds. However, it is important to note that the rapid depreciation of the yen in recent years has led to an overestimation of the value of foreign currency-denominated investments.

If the exchange rate settles and the “tailwind” stops, it will be difficult to expect the same performance as before. Moreover, if the yen appreciates against the U.S. dollar when overseas stock markets decline, losses will be amplified.

Diversification Effect Declines as Market Capitalization of U.S. Large Cap High-Tech Stocks Increases

The next concern is the “decline in the diversification effect. As mentioned at the beginning of this paper, the [Orcan] is currently more popular than the [S&P500]. This is because the S&P 500 invests only in U.S. stocks, whereas the ORKAN is a “diversified investment” that targets global stock markets, including emerging markets. In textbook terms, diversification, which diversifies the financial products and regions in which investments are made, can reduce investment risk. However, Orcan is notorious for its bias in investment targets.

The main countries in which it invests are heavily weighted toward the U.S., with 63% in the U.S., 6% in Japan, 4% in the U.K., and about 3% in France. The reason for this is that the market capitalization of some large-cap stocks in the U.S. market has increased dramatically.

For example, Apple, Microsoft, Amazon, and Alphabet alone account for more than 10% of the total market capitalization of Orcan. It can be said that the effect of diversification is weakening.”

The market capitalization of a stock is calculated as “share price x number of shares outstanding” and is generally considered to indicate the size of a company. Most stock indices are then constructed based on market capitalization. Therefore, the composition ratio of stock markets and stocks with large market capitalization rises, creating a bias that increases the risk of the fund.

It should be noted that the degree of diversification has been declining in recent years, although index funds are a low-cost and efficient investment method that can provide diversification benefits. Could it be said that this shows the limitations of index management?”

Active funds” of domestic stocks are also an option.

So, with these weaknesses in mind, what is the best way to invest?

If you have a surplus fund that you do not plan to use for at least the next 10 years, I think there is no problem investing only in [All Country] or [S&P 500]. However, in that case, the ironclad rule is to control risk by accumulating funds, diversifying investment timing, and continuing to invest over the long term.

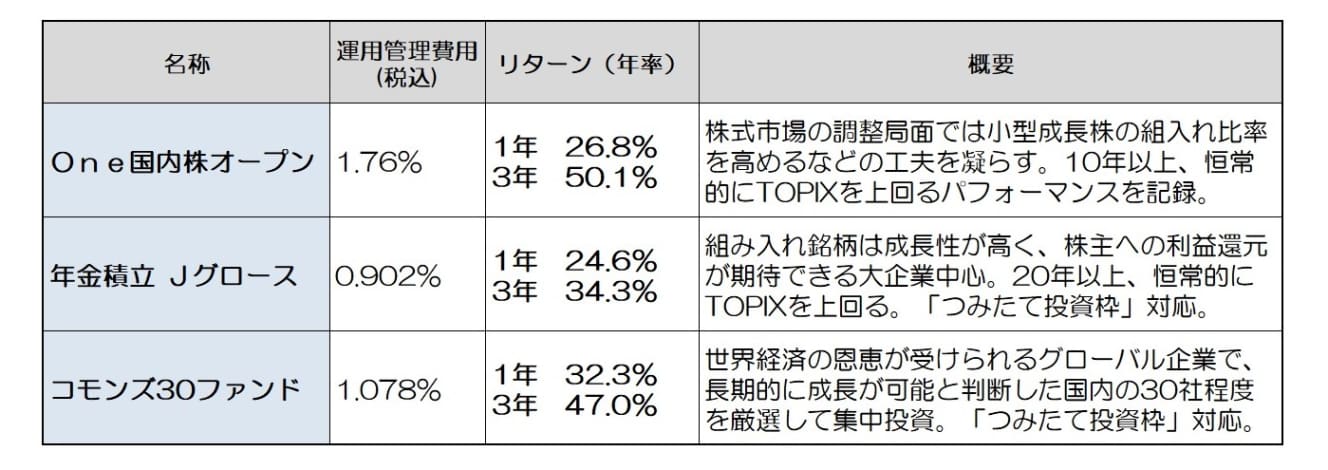

He also suggests combining an “active fund” of domestic stocks for those who are already accumulating investments in the [Orcan] and [S&P500] and want to invest more efficiently with a little less risk. There are various types of active funds, but basically they are investment trusts that aim to outperform an index.

Compared to the U.S., the Japanese stock market is a market where active funds tend to “beat” the index.

In addition, the companies in which the funds invest take on the currency risk without the individual investor having to bear the direct currency risk.

When hearing about active funds, many people exclude them from their choices because their management cost, the investment management fee, is higher than that of index funds.

However, there are a number of funds that have outperformed indexes even when costs are taken into account. It would be a waste to throw away the possibility of obtaining such excess returns.”

We asked Mr. Shinoda to pick out active funds of domestic stocks that are suitable for combination. He says that the standard investment amount when combining these funds is about half of the amount of the Orcan and S&P 500. We hope you will find this information useful.

Interview and text: Kenji Matsuoka

After working as a money writer, financial planner, and market analyst for a securities company, Matsuoka became independent in 1996. He writes articles on finance and asset management mainly for business and economic magazines. Author of "A Textbook for the First Year of Robo-Advisor Investing" and "Understanding with Rich Illustrations! Cashless Payments for the Absolute Benefit of Cashless Payments".