The current investment performance is greatly affected by the weak yen… “Is it safe to choose NISA and Orkan?

Are “weaknesses” being overlooked due to strong performance?

However, the high praise of index funds in the media and on social networking services has led some to overlook their “weak points” as index funds. Naoko Shinoda, deputy head of Rakuten Securities’ Asset Creation Research Institute and fund analyst, explains as follows.

There is no doubt that it is one of the best investment trusts for long-term accumulation investment, but it is not a panacea. However, it is not a panacea. It is important to understand the contents of the fund properly in order to overcome situations in the future when investment performance does not go as expected.

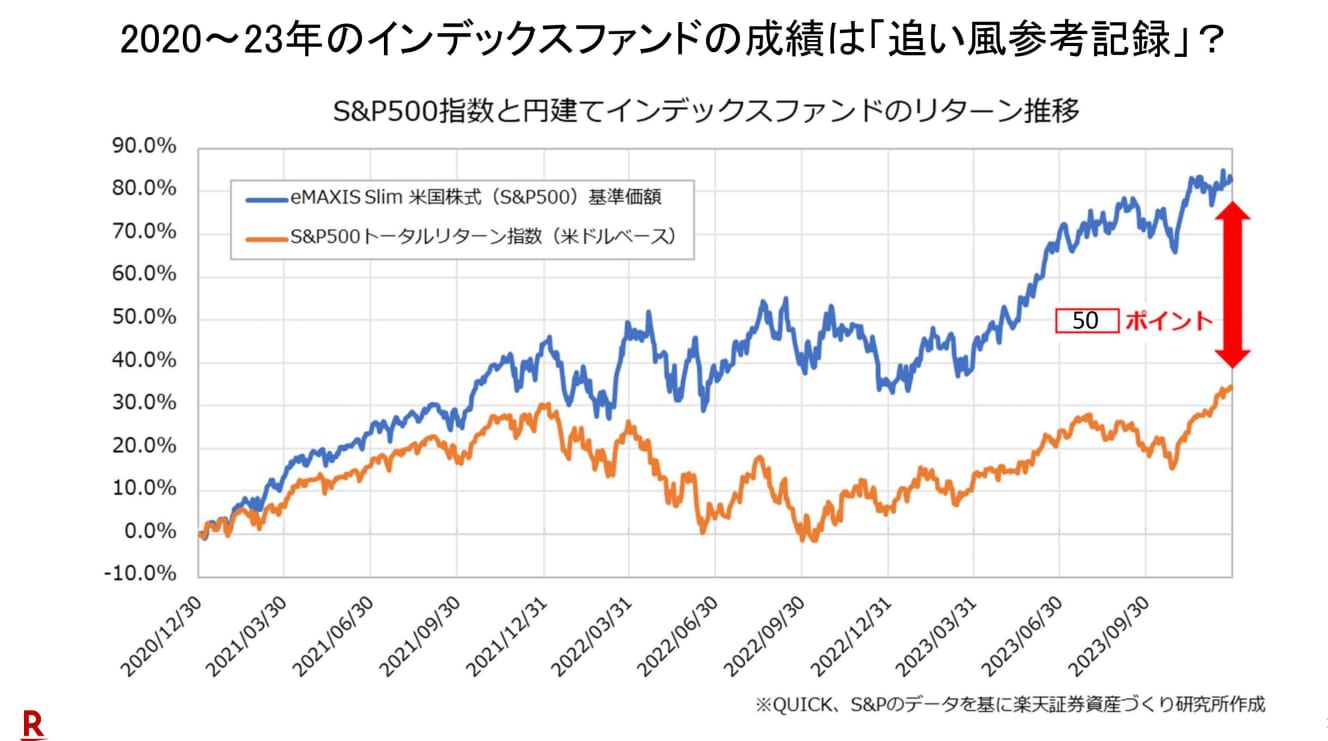

The current investment performance is a “tailwind reference record” due to the weak yen.

Therefore, the first thing to understand is “true ability. As mentioned above, the performance of [Orcan] and [S&P500] over the past few years has been overwhelming, but Mr. Shinoda points out that “it should be taken as a ‘tailwind reference record.

Major overseas equity indices such as [All Country], [S&P500], and even the New York Dow have returned 70 to 80% across the board over the past three years, and 50 to 60 points of that is actually due to the effect of the weak yen. About 3 years ago, in January ’21, the yen was in the 103-104 yen per dollar range, and it is currently around 148-150 yen per dollar.

In other words, the yen has weakened by more than 40% in three years, raising the returns of U.S. dollar-denominated index funds beyond their ability.

Surprisingly, returns for the most recent three years were higher for index funds linked to the Nikkei Stock Average and TOPIX (Tokyo Stock Exchange Stock Price Index) on a local currency basis.

He said, “I don’t deny that currency fluctuation is a source of return and one of the most appealing aspects of investing in foreign currencies, but the recent rapid depreciation of the yen has made it difficult to invest in foreign currency denominated funds. However, it is important to note that the rapid depreciation of the yen in recent years has led to an overestimation of the value of foreign currency-denominated investments.

If the exchange rate settles and the “tailwind” stops, it will be difficult to expect the same performance as before. Moreover, if the yen appreciates against the U.S. dollar when overseas stock markets decline, losses will be amplified.

Diversification Effect Declines as Market Capitalization of U.S. Large Cap High-Tech Stocks Increases

The next concern is the “decline in the diversification effect. As mentioned at the beginning of this paper, the [Orcan] is currently more popular than the [S&P500]. This is because the S&P 500 invests only in U.S. stocks, whereas the ORKAN is a “diversified investment” that targets global stock markets, including emerging markets. In textbook terms, diversification, which diversifies the financial products and regions in which investments are made, can reduce investment risk. However, Orcan is notorious for its bias in investment targets.

The main countries in which it invests are heavily weighted toward the U.S., with 63% in the U.S., 6% in Japan, 4% in the U.K., and about 3% in France. The reason for this is that the market capitalization of some large-cap stocks in the U.S. market has increased dramatically.

For example, Apple, Microsoft, Amazon, and Alphabet alone account for more than 10% of the total market capitalization of Orcan. It can be said that the effect of diversification is weakening.”