Not Just a Bad Thing! Rising long-term interest rates increase interest payments on the “national debt”… but is it a plus for families?

BOJ “accepts rising long-term interest rates”…sees easy transition to fiscal consolidation

Long-term interest rates are rising. Japan is saddled with a massive debt of over 1,000 trillion yen in government bonds, and rising interest rates are expected to increase the burden on the Japanese people through higher interest payments. On the other hand, experts have pointed out that a shift to fiscal rehabilitation can be made immediately if the government is so inclined. What will life be like in the future?

The yield on 10-year JGBs is a measure of long-term interest rates. The Bank of Japan’s ultra-low interest rate policy has kept the yield near zero. However, at the end of October this year, the yield rose to 0.955%, the highest level in about a decade and a half, as selling pressure on JGBs increased in the bond market.

The price and yield of JGBs and other bonds are inversely related: a fall in price causes the yield to rise, while a rise in price causes the yield to fall. The BOJ has been buying large amounts of government-issued bonds in the money market to suppress price declines and interest rate rises. While maintaining this policy, the BOJ has recently shifted its stance to allow long-term interest rates to rise to some extent.

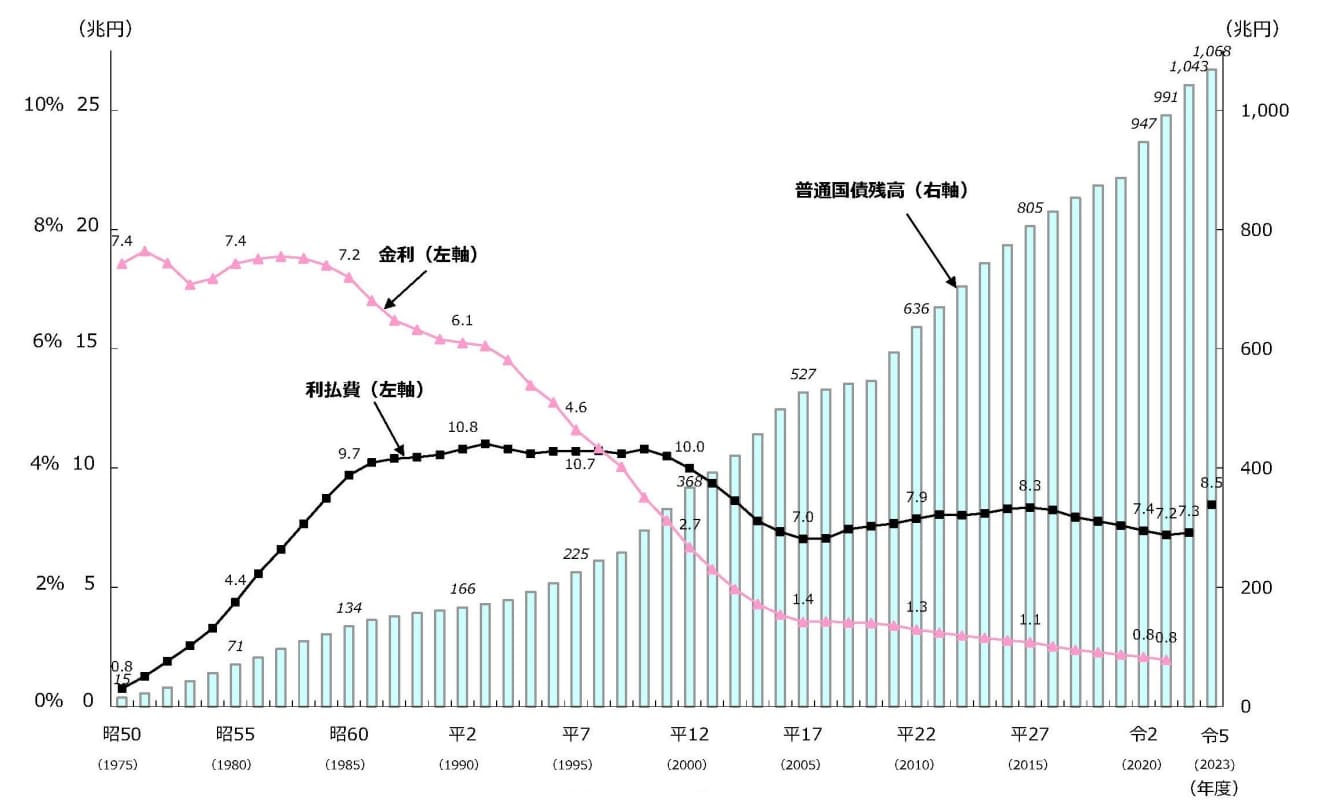

National Debt”….Interest payments increase by 10 trillion yen per year with a 1% rise in interest rates Interest payments increase by ¥10 trillion per year with a 1% rise in interest rates

When government bonds come due for redemption (repayment), the government often refinances them because it does not have enough funds to repay them. Although not all of the 1,000 trillion yen in debt will be refinanced at the same time, it is estimated that a 1% increase in interest rates will result in a 10 trillion yen increase in interest payments per year if all of the debt were refinanced at the same time. The government’s initial budget for the current fiscal year totals approximately 114 trillion yen, with tax revenues of just under 70 trillion yen. The shortfall is covered by government bonds and other debt. If interest payments increase due to higher interest rates, the impact on fiscal management will be significant.

The government has been issuing large amounts of JGBs and spreading money around as a measure against deflation. The BOJ has been purchasing these bonds in the money market and adopting a policy of ultra-low interest rates to prevent the government from incurring heavy interest payment costs. The BOJ’s method is called “yield curve control (YCC),” in which the BOJ purchases JGBs to keep the interest rate on 10-year JGBs at “around zero percent. This is the so-called “zero interest rate policy.

Meanwhile, prices have been rising around the world due to economic expansion and soaring oil prices, and countries have been raising interest rates in order to suppress these rises. Global inflation has also increased pressure on domestic financial markets to raise interest rates.

Using the YCC method, the BOJ successively revised the allowable range for long-term interest rates to rise above zero% to around 0.25%, 0.5%, and so on. At the end of July, the Bank of Japan had set the upper limit at 1%, but at the end of October, it changed the upper limit to “around 1%,” thereby shifting its stance to allow interest rates to rise by more than 1%. Interest rates in Japan are also set to rise.

Interest Expense” for the current fiscal year is 8.5 trillion yen was expected to be…

With interest rates rising, how much debt does Japan have? According to the Ministry of Finance, the “national debt” is the total of government bonds, borrowings, and FBs, which totaled 1,275.6116 trillion yen at the end of September. Of this amount, over 1,131 trillion yen was in JGBs, most of which are called “ordinary JGBs,” the main source of funds for interest payments and redemptions being taxes, and the outstanding balance of these was over 1,027 trillion yen.

For example, a graph showing the outstanding amount of JGBs and changes in interest payment expenses and interest rates published by the Ministry of Finance shows that while the outstanding amount of JGBs has expanded due to Abenomics, interest payment expenses have been kept at around 7 or 8 trillion yen annually for the last 20 years as interest rates have been guided to lower and lower levels. For the current fiscal year, the initial plan was expected to be approximately 8.5 trillion yen.

On the other hand, the Ministry of Finance has been raising the interest rate on JGBs it issues in response to trends in the financial markets: the 10-year JGBs had been at 0.1% for several years until March 2010. Since July of this year, the rate has been 0.4%, and in October, it was raised significantly to 0.8%.

JGBs come in fixed-rate and floating-rate types, with fixed-rate maturities varying from 2 to 40 years. When JGBs reach their maturity dates, they are often refinanced. The cost of interest payments on fixed-rate JGBs is determined by the level of interest rates at the time of issuance, and future refinancing will increase the cost of interest payments due to rising interest rates.

Is the household sector, which has more “deposits” than “debts,” on the contrary positive?

Some experts disagree with this pessimistic view of public finances, pointing out that there are ways to curb the issuance of government bonds. Taro Saito, Director of Economic Research at Nissay Research Institute, is one such expert. He believes that the BOJ’s decision to allow long-term interest rates to exceed 1% “came a bit too soon,” and that it “clearly shows that the YCC,” which has been guiding interest rates to ultra-low levels, has “become a mere skeleton. He then added, “The BOJ has been holding down interest rates.

I think the BOJ will continue to hold down interest rates. If left to nature, interest rates could rise to 2% or 3%, but the impact on the economy would be too great. I think the BOJ will continue to buy JGBs and keep interest rates at the 1% level for the next few years.”

Furthermore, Mr. Saito says that although interest rates will rise and interest expenses on JGBs will increase compared to the zero-interest-rate era, “we will just have to accept it. On the other hand, unlike the government and corporate sectors, which are heavily in debt, the household sector has more deposits than debts, and the rise in interest rates will be positive for the household sector as a whole, he said.

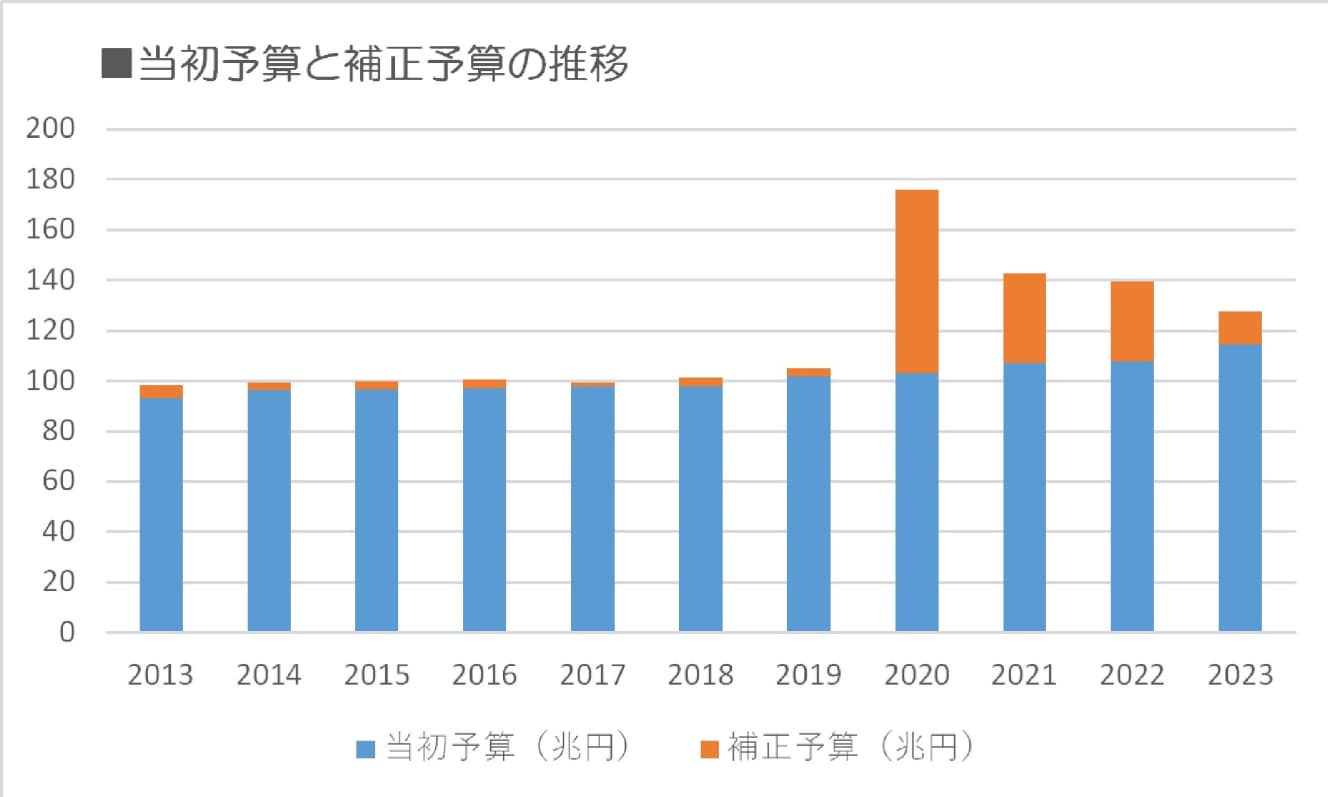

The source of the problem is “ Waste of taxpayers’ money” is the “supplementary budget,” which is full of “wasteful use of taxpayers’ money”?

To begin with, Saito points out that the Japanese economy has been in a contractionary equilibrium due to deflation, but the economy will grow and the size of fiscal revenue and expenditure will expand in the future. What will be important is to avoid spending money on wasteful things, so that there will be no excessive spending restraints, which is called “austerity”

Put another way, “No need to do a supplementary budget. The initial budget is too small,” Saito said. What does he mean?

For the past several years, supplementary budgets have been prepared every fall under the guise of economic stimulus measures. On the other hand, the initial budget at the beginning of each fiscal year has been at a record high every year. This is because it is compared to the initial budget of the previous year. In order to look at the actual situation, it is necessary to compare the total budget amount, which is the sum of the previous year’s initial budget and supplementary budget. Mr. Saito explains that each year’s initial budget is more austere than the previous year’s total budget.

In other words, we can stop compiling supplementary budgets and include all necessary items in the initial budget stage. Of course, additional measures may be necessary for unforeseen situations such as major disasters.

It is easy to include everything in a supplemental budget. It is easy for each ministry and agency to get what they want. On the other hand, the initial budget takes about six months to compile, and the screening process is very strict.

Therefore, ministries and agencies put what they want in the supplementary budget. Supplementary budgets are supposed to be compiled when unforeseen circumstances arise, but in reality, they contain useless things.

Mr. Saito thus sees a lot of waste in the supplementary budgets, which tend to be checked only briefly and laxly.

As a general rule, supplementary budgets that are called economic measures, as is customary every fall, should be stopped. This would “eliminate wasteful spending and curb the issuance of government bonds,” Saito says.

Interview and text by: Hideki Asai