Secret Techniques for Ordinary Company Employees to Easily Make “100 Million Yen

The Definitive Edition! From 60 yen to a "Millionaire"! There is an investment method that can turn your life around even if you failed once!

From a life with 60 yen in one’s pocket to the pioneer of “FIRE

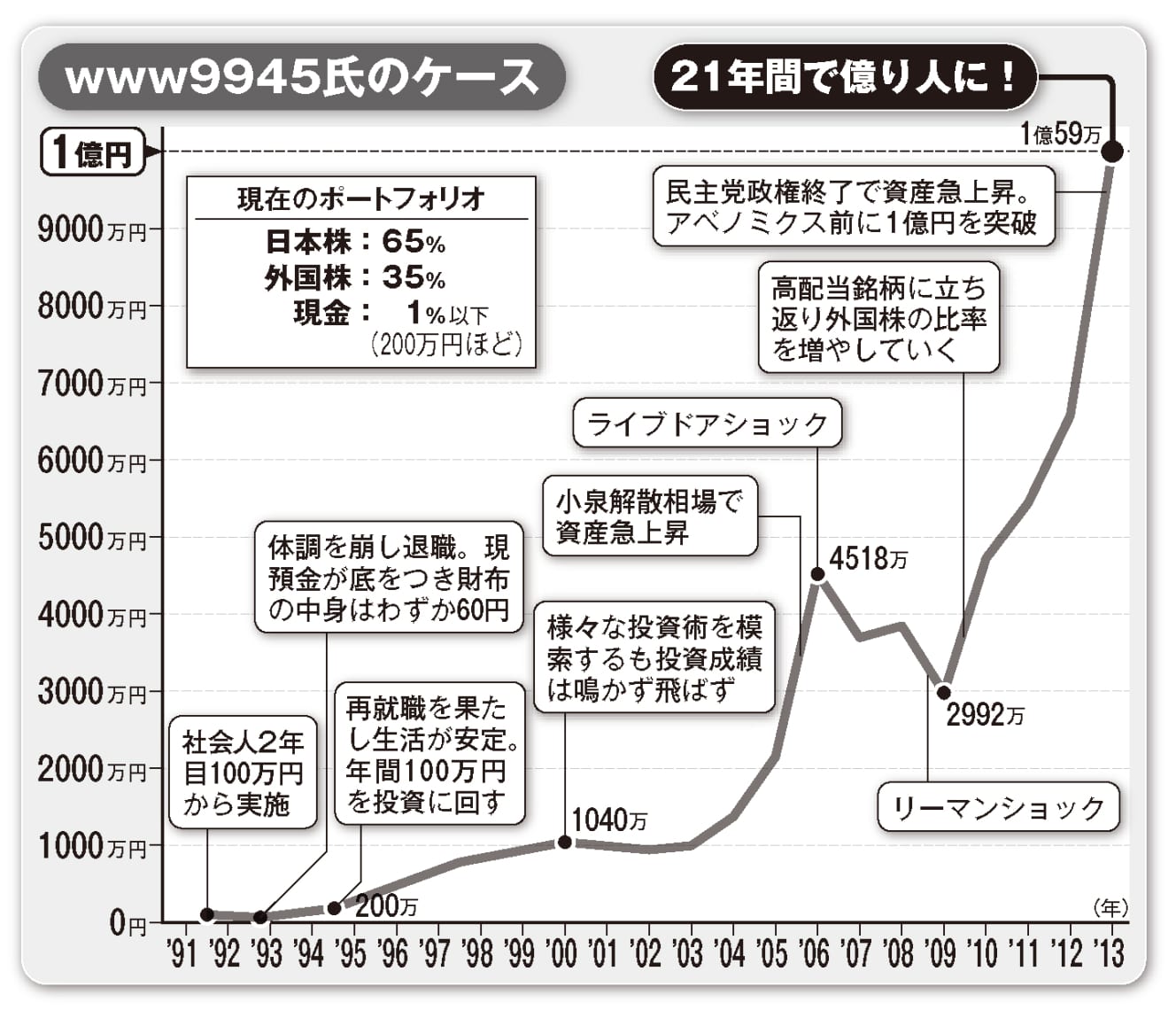

Not all “billionaires” who have amassed assets in the hundreds of millions through investment have been investment experts from the start. Some have gradually increased their assets from a situation where they could not even afford to eat tomorrow. Individual investor www.9945 now owns more than 500 million yen in assets. He was living on the edge when he started investing.

He says, “I had been investing in stocks since I was a newly graduated employee, but after I got sick and quit my job in ’92, I had been poking around for about nine months. My savings had run out, and at the worst time I had only 60 yen in my wallet. I managed to find a part-time job as a cleaner and resumed my investment lifestyle around 1994, when I became a full-time employee and had a stable income. At the time, I was putting 70,000 yen a month from my salary, or about 1 million yen a year, into stocks.

This is how Mr. WWW9945 resumed investing, but in 2000, the IT bubble burst. However, the IT bubble burst in 2000, and for a while he had no success.

The tide turned with the securitization boom that began around 2002, when the share price of Asset Managers (now Ichigo) nearly doubled. After that, however, the Livedoor Shock caused a 10% drop in assets in a single day, and the Lehman Shock caused a huge loss. During that time, I remained conscious of “Street Corner Watch. Seeing what is popular and where, and getting information by actually seeing it with my eyes, is a more reliable way to invest than reading “Shikiho”.

The tailwind blew once again as we turned our attention to U.S. and ASEAN stocks against the backdrop of the strong yen at that time. I bought high dividend stocks and small stocks that had become undervalued under the Democratic Party of Japan administration, and when the Noda administration was dissolved in ’12, stock prices jumped and I achieved assets of 100 million yen. This was more than 20 years after I first started investing. While some of my friends quit investing, I never gave up. I think that is the biggest reason why I became a ‘billionaire.

Later, his investments rode the Abenomics market and doubled to 200 million yen by the end of 2001. Currently, he has 14 million yen in stock dividends per year, half of which he uses for living expenses and half for investments. He is truly a pioneer of “FIRE,” but what method would you recommend to those who are just starting out in asset management?

He says, “If you are going to invest, I would recommend that you start by accumulating and buying mechanically. Even now, when my assets have increased, I am still using the “Tsumitate NISA” up to the maximum amount of 400,000 yen per year. Combining this with an iDeCo might leave you with your hands full, but if you can afford it, you can buy stocks that are special offers from stores you frequent. I don’t mind if the stock price drops a little, and I think you will be able to build enough assets to at least easily clear the ’20 million yen for retirement’ problem.”

He continues to maintain his enthusiasm for investing and also continues to make steady accumulations. Both of these are important attitudes for becoming a “billionaire.

How to Turn Around from a Failure to a Loss of 3 Million Yen in the Third Year of Investing

I was in my late 20s when I started working after completing my doctorate at graduate school. I started investing in stocks as a way to earn money outside of my salary because I was working shorter hours than others and had scholarship debt.

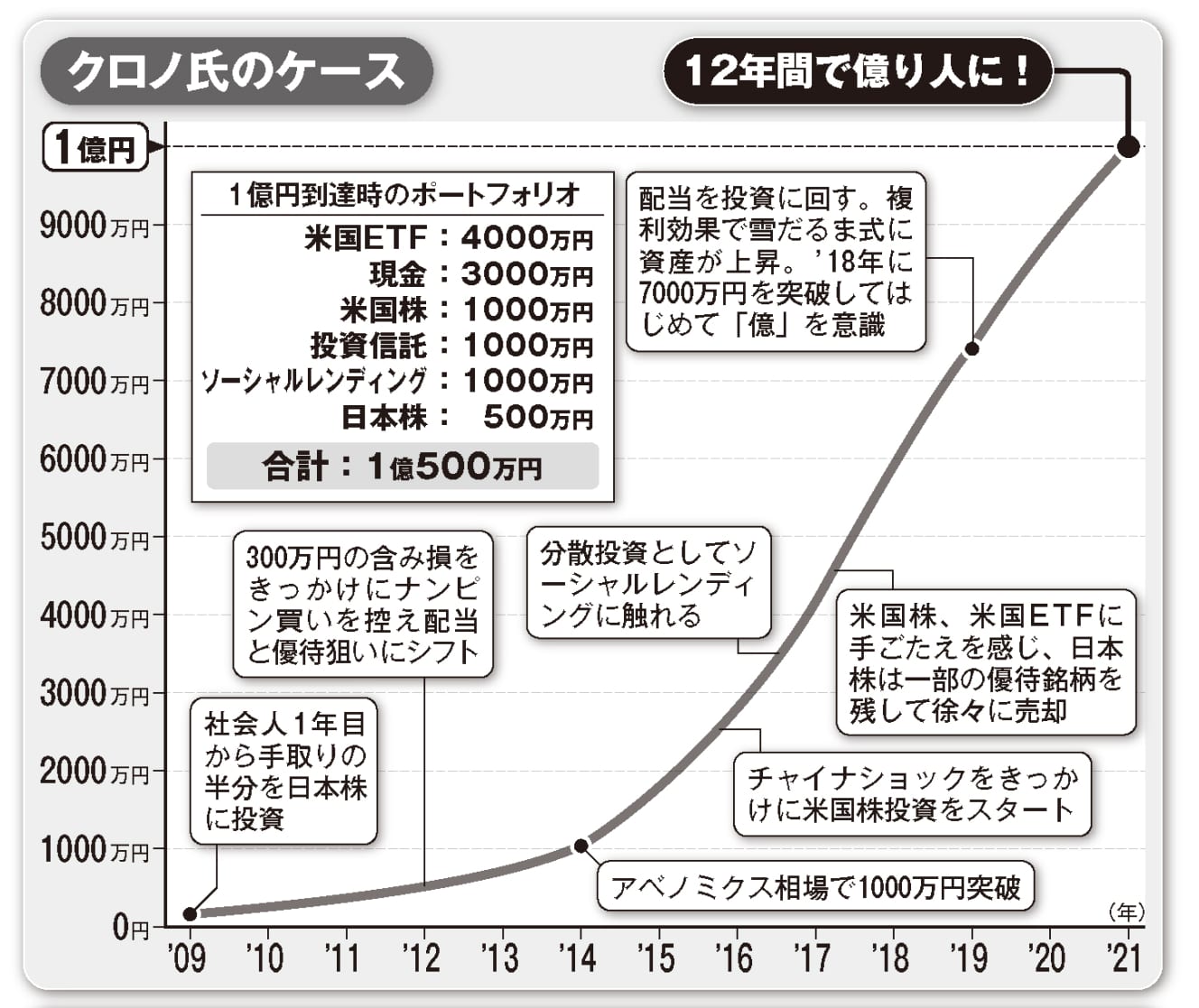

An individual investor, Mr. Crono began his investment life by allocating half of his monthly take-home pay to the purchase of Japanese stocks. After the Lehman Shock, many stocks were undervalued, and he was steadily making gains on sales, but one mistake led him to switch his investment approach.

When the price of a stock I was holding fell sharply, I thought it was a good time to buy, so I repeated what is called “nanpin buying,” and as a result, I incurred a loss of 3 million yen. Since then, I stopped buying stocks of companies whose numbers looked good at first glance but whose businesses I did not fully understand, and started buying stocks of well-known companies I wanted to support. Then I realized that the saving effect of shareholder benefits is not ridiculous. Aeon, which I still hold, is a typical example. Another advantage of investing in stocks with special benefits is that I can buy a variety of stocks in the smallest unit that gives me special benefits, so I don’t lose a lot of money,” he said.

Riding the Abenomics market, Chrono’s assets surpassed 10 million yen in five years, and it was dividends that supported him. At the time, he did not have the image of becoming a billionaire, but he felt that “single-decker” Japanese stocks were risky, so he looked for a new investment.

He says, “I started investing in U.S. stocks after the China shock of ’15. In retrospect, I should have bought growth stocks such as Tesla, but it was solid stocks such as P&G and Coca-Cola that caught my attention. I also bought more ETFs of U.S. stocks, and I was conscious of diversifying my investments. In addition, I also invested in “social lending. This is a system in which money is lent to individuals or companies via the Internet, and a pre-determined rate of return is received like interest. Since it does not fluctuate like stock prices, it felt a bit like a risky time deposit. I started to realize the strength of the snowball effect of reinvesting the dividends. I realized that I was going to make more than 100 million yen.

Chrono’s theory that he never touched the virtual currency that was becoming a hot topic at the time reveals a philosophy that prioritizes “peace of mind.

He said, “I invest in order to relieve anxiety about the future, so I prefer not to hold financial instruments that make me nervous. For those who are just starting out, I recommend buying mutual funds or inexpensive individual stocks to gauge how much price fluctuation you can mentally tolerate in a day.

Stretch widely, but not too widely. The best way to invest is to follow a theory.

Continuing to work is a hedge against investment risk

Many people who have achieved 100 million yen in assets from ordinary company employees have one thing in common: they never quit their jobs, even after accumulating a large amount of assets. The monthly paycheck is the quickest and most stable way to make money for investment.

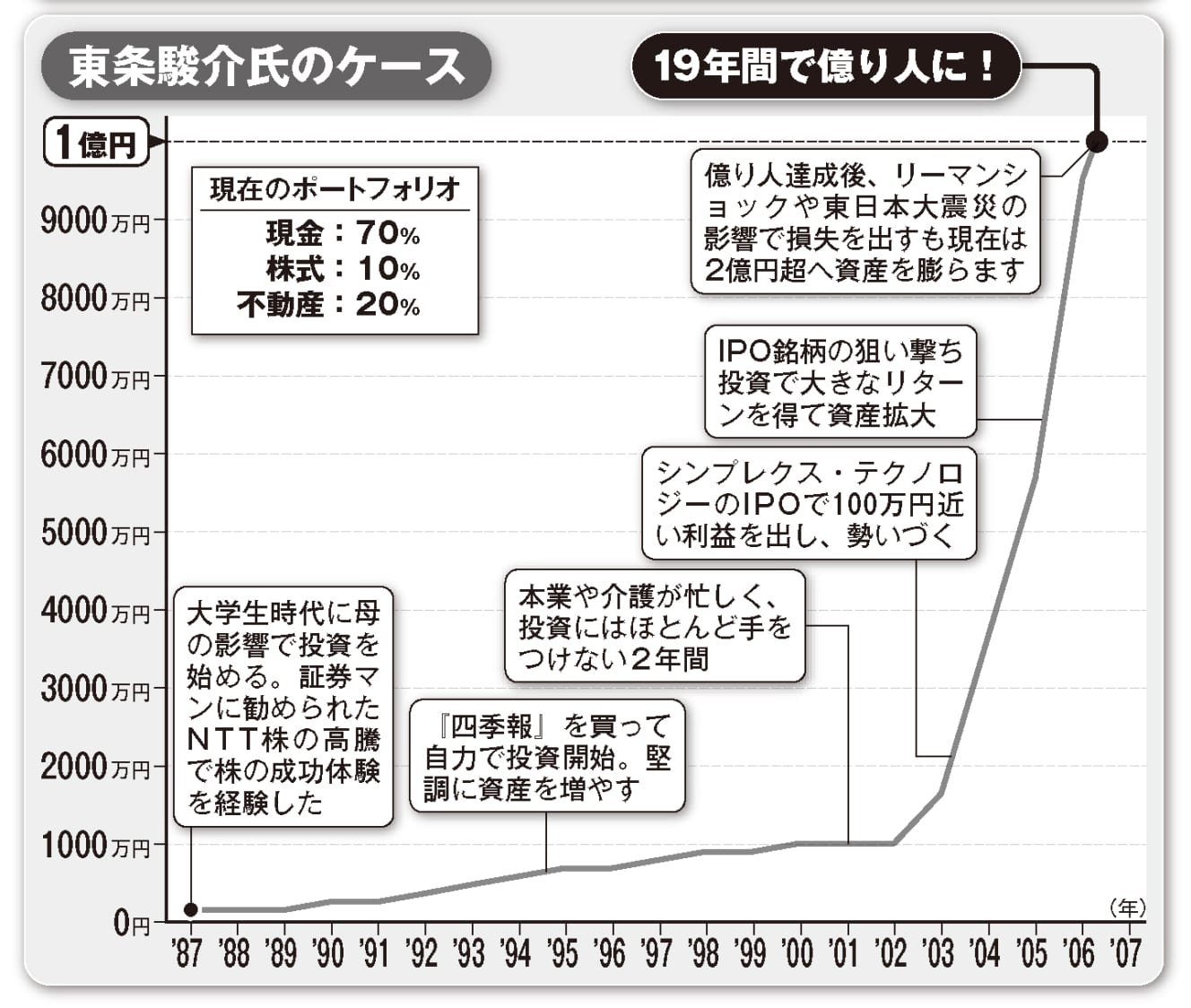

Tojo Tojo, author of “Making 100 Million Yen with Super Affordable Stocks and Real Estate! (Diamond Inc.), who has made ¥200 million from stock and real estate investments, is still working as an office worker.

What I consistently practice is to pick up coins whenever I find them on the floor,” he says. I always do coupons, credit card promotions, flea market apps, iDeCo, and other financial techniques. Even if it’s 100,000 yen a year, think of it as 3 million yen if your life as an office worker lasts 30 years, and keep earning pocket change.”

Mr. Tojo made his investment debut at the age of 18, when he purchased NTT stock, which was the talk of the town when it was listed on the Tokyo Stock Exchange. He also traded Toyota and Sony stocks while reading “Shikiho,” but it was after focusing on IPO (Initial Public Offering) investments that he quickly increased his assets.

I applied for the IPO of Simplex Technology (now Simplex), which had a public offering price of 200,000 yen, and the initial price went up to 990,000 yen. In recent years, there have been more cases where the initial offering price exceeded the offering price, and I believe this is a low-risk, high-return investment that ordinary investors can make as long as they pass the lottery.

Tojo’s portfolio has further expanded by focusing on real estate investments. This does not mean that he borrowed tens of millions of yen to buy a whole apartment building.

When the Lehman Shock hit and the stock market was totally ruined, I suddenly bought a one-room apartment in Higashimurayama for 2.9 million yen. I recommend used studio apartments because they are a relatively low-cost investment with a good yield. Especially with the Corona Disaster, many owners are in a hurry to sell, and you may be able to get it for much less than the original price. If you are investing in real estate for the first time, choosing an “owner-occupied” property that already has tenants will allow you to avoid the labor of finding tenants on your own and the risk of vacancy. The fact that the owner is a company employee also makes it easier to pass bank examinations and more popular with management companies, so there is another benefit to continuing to work.

Although Mr. Tojo suffered major losses when Lehman Brothers collapsed and the Great East Japan Earthquake hit, he was able to double his assets by continuing to invest in stocks and real estate without any major fluctuations.

With stocks, real estate, and his day job, he is able to remain calm and watch even if one of his investments is not doing well. What is important to become a billionaire is to become an investor who can wait. If you have an open mind, you will be able to invest appropriately when opportunities arise.

The “one-yen stop-loss rule” for investment without making mistakes

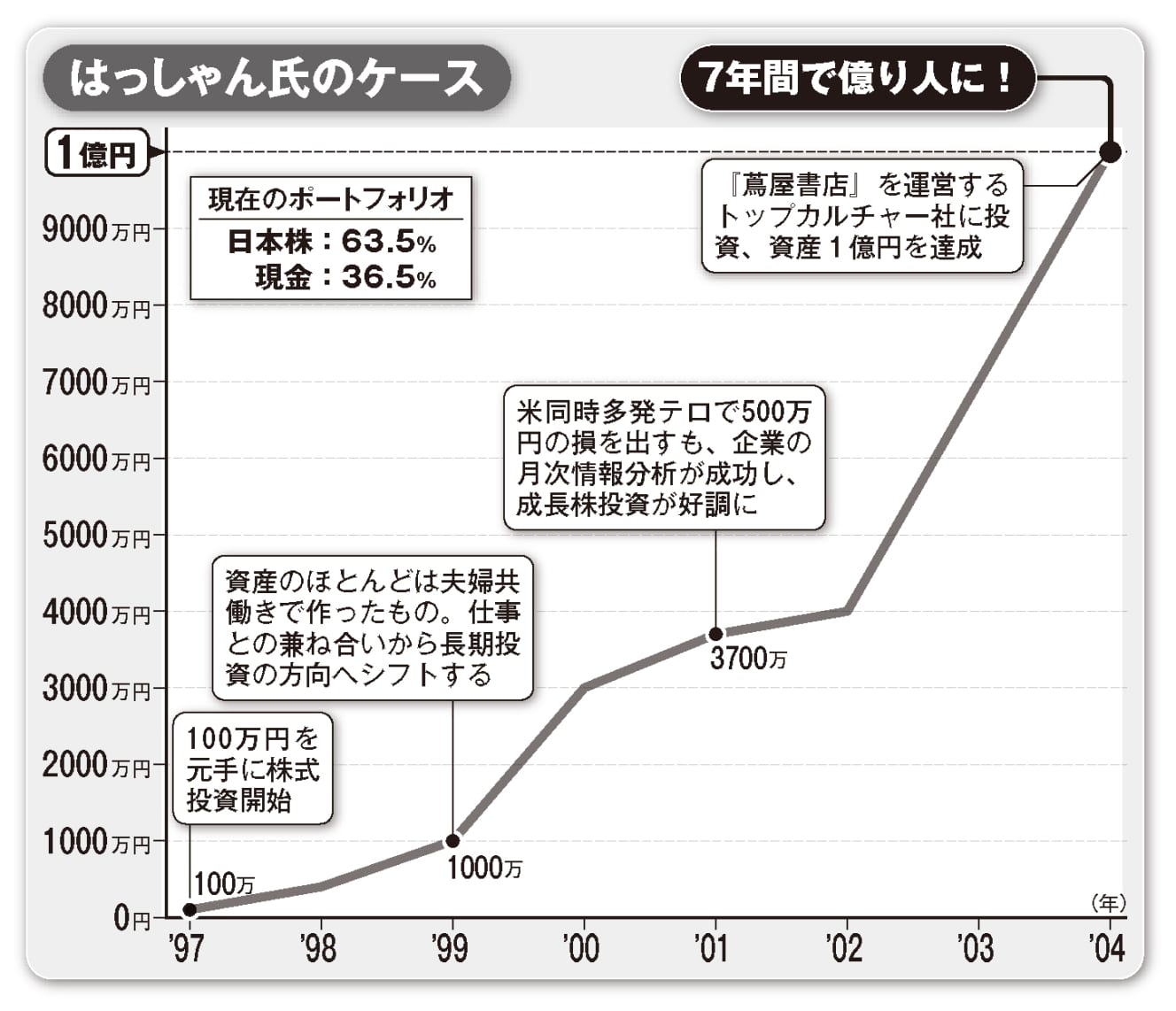

Some may think that looking back on the experiences of successful investors who have achieved 100 million yen in assets is not reproducible. Finally, we asked Mr. Hassan, an investor Vtuber who has succeeded based on long-term investment in growth stocks and currently holds over 250 million yen in assets, to share with us his investment techniques that can be used in any market. He currently has over 250 million yen in assets.

What I used to do was to read the “monthly information” of a company and see if it is growing or not,” he said. Especially in the retail and service industries, many companies update monthly information on their websites about existing store sales and store openings. We pick up companies whose figures are growing and compare them with those of their rivals. We can then see whether the industry as a whole is growing or whether the company is in a one-man race. Companies in the latter category have room for growth and can be judged to be suitable for long-term investment. Conversely, a company that is opening more stores but sales are down month over month can be considered risky. It allows us to make reasoned trades without being misled by stock prices.

By checking monthly information once a month, Mr. Hassan discovered the growth potential of Top Culture, which operates the Tsutaya bookstore, and through long-term investment, his assets surpassed 100 million yen.

He said, “The reason I did not lose a lot of money riding the IT bubble around ’00 was because I judged not to buy overvalued stocks based on monthly information and financial statements. I am glad that I was able to ensure that I bought companies that were growing but whose stock prices were stagnant, rather than companies whose profits and stock prices were diverging. Such growth stocks may not pay dividends, but my stance is that holding growth stocks for the long term provides a greater return than short-term dividends.

Of course, not everyone will suddenly encounter a market as big as the top culture or the IT bubble. In order to continue investing without losing precious capital, risk control is of the utmost importance.

Risk control means, specifically, cutting your losses. I used to practice the “one-yen stop-loss rule,” which means that I would sell the stock if the closing price on the day after the purchase date was even one yen lower than the purchase price. This minimizes the loss, and if the timing of the purchase was simply bad, you can re-purchase the stock when the time is right. However, it is also important to set a rule that you can only re-purchase stocks up to three times, as you may have made a mistake in the stock selection itself.

Do not buy or sell stocks based on fads or random thoughts. It seems that what all billionaires have in common is a mindset of trusting their own investment theories.

From the June 10, 2022 issue of FRIDAY

PHOTO: Afro