How to Easily Retire Early Using “F.I.R.E. ” Techniques for 40s and Above

Read this and achieve your "Dream Early Retirement!" How much money do I have? How do I make money? How many years can I do it? What should I never do? All your questions will be answered!

Early Retirement Techniques for Achieving Financial and Spiritual Freedom

The “100-year life era” is upon us, and people in their 70s and even 80s will have to continue working. Against this backdrop, the concept of “FIRE,” which was born in the United States, has been attracting attention. “Financial Independence FIRE” stands for “Financial Independence,” “Retire,” and “Early”. In Japanese, it means “financial independence and early retirement.” The point of FIRE is not simply to retire early, but to become financially independent by earning through asset management.

FIRE includes “Full FIRE,” in which people quit their jobs completely and make a living solely on passive income, and “Full Retirement,” in which people earn passive income through asset management. “Side FIRE”, which is to continue working in the way one likes to work while earning passive income. Let’s take a look at these two options in detail.

Side FIRE can be achieved in a few years even by people in their 40s and 50s.

Flexible Planning Based on Household Structure and Income!

It is generally believed that people in their 20s and 30s should start preparing for FIRE. However, it is not too late to start preparing for FIRE in your 40s or 50s. This is based on the so-called “4% rule,” a U.S. financial theory that states that if a person can keep his or her expenses under 4% while managing assets after retirement, there is a high probability that the person will be able to maintain his or her assets for 30 years or more.

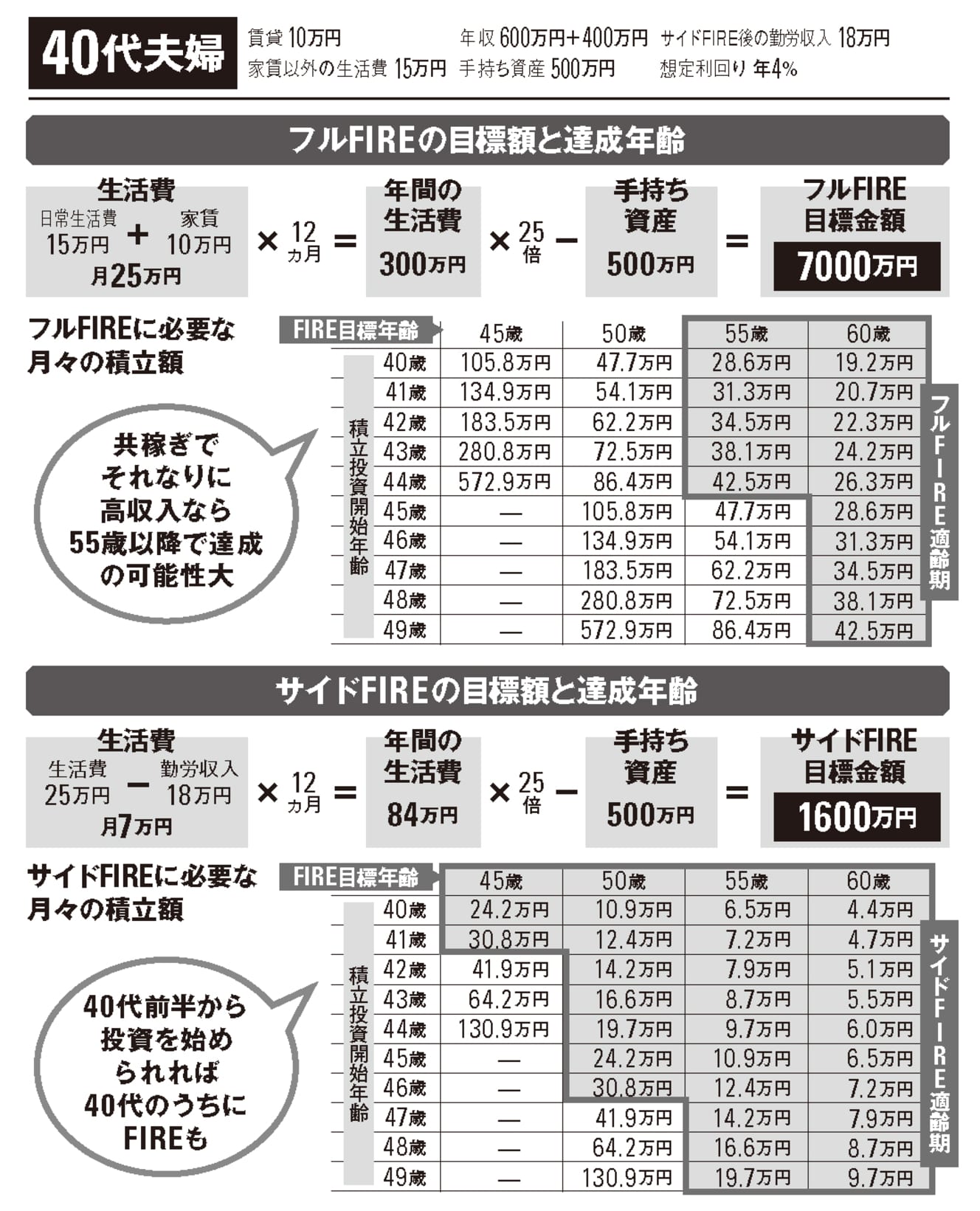

First, let us look at the case of a working couple in their 40s. Let us assume that their annual income is 10 million yen and they live on 250,000 yen per month for rent and living expenses combined. In this case, the amount needed for full FIRE would be “250,000-yen x 12 months x 25 years = 7.5 million yen. The amount needed for full FIRE is “250,000-yen x 12 months x 25 years = 7,500,000 yen. Even if you already have ¥5 million in assets on hand, you will need to prepare ¥7,500,000,000 from now on.

However, if expenses are properly controlled, full FIRE is not a dream. Subtracting annual living expenses of 3 million yen from the couple’s combined take-home pay of 7.7 million yen, a simple calculation leaves a little less than 400,000 yen per month. If all of this were invested, full FIRE would be attainable at the age of 55 to 60. Side FIRE, which assumes that the couple will continue to earn 180,000 yen per month after retirement, can be achieved in about 4 to 5 years.

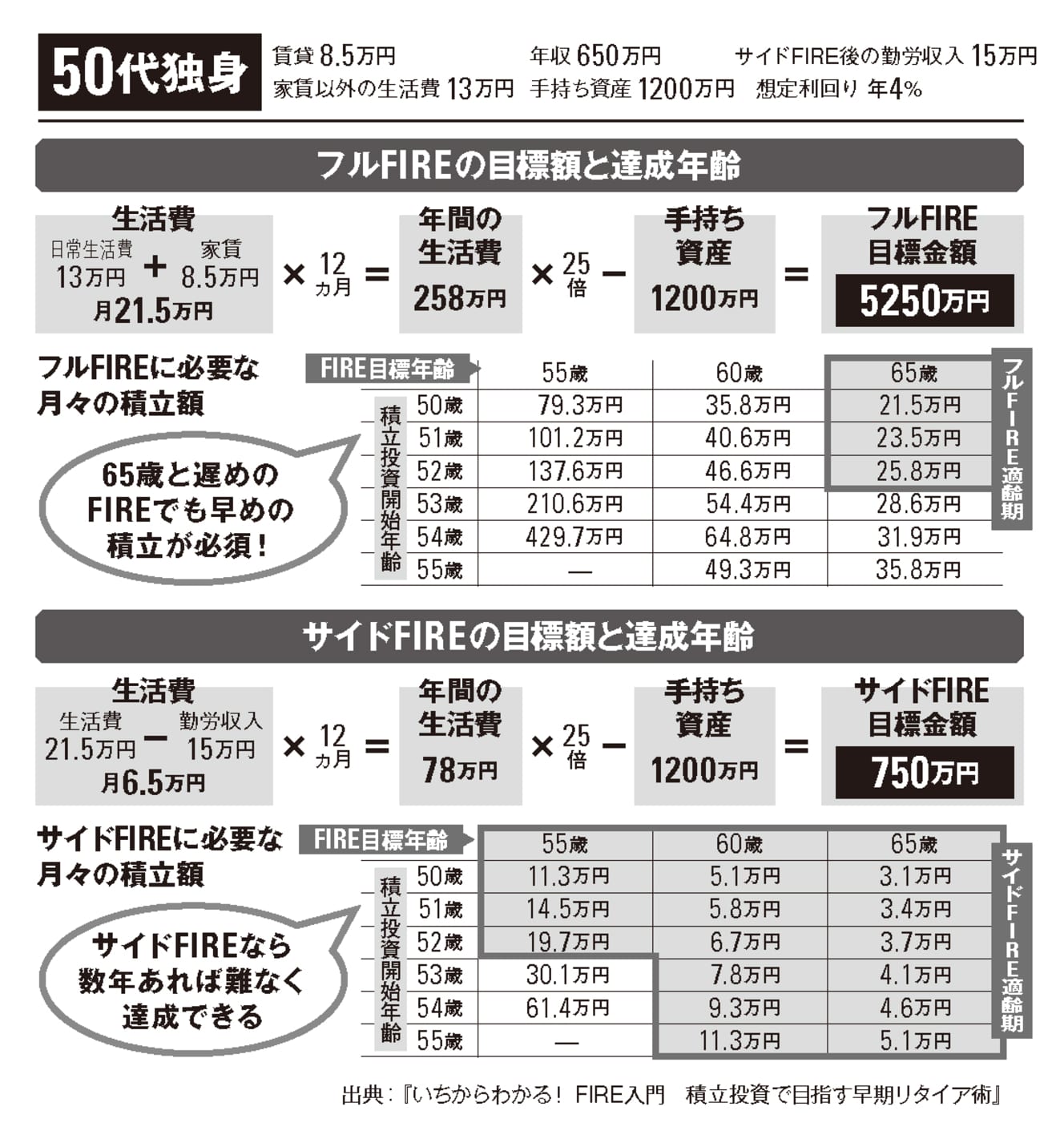

Next is the case of a single person in his/her 50s. If the monthly living expenses are 215,000 yen, the target amount is 64.5 million yen. If he has 12 million yen in assets on hand, he only needs to prepare the remaining 52.5 million yen. With a take-home income of 5-million-yen, one can invest about 200,000 yen per month after deducting living expenses. Full FIRE can be achieved at the age of 65 or so if you start investing in savings early. Side FIRE can be achieved in 3 to 5 years.

The hurdle for full FIRE is high even for households with high incomes. However, it is important to keep in mind that in this day and age, it is a blessing if you can retire as early as possible.

How have successful investors increased their income? “Global and U.S. stocks” are essential.

The main investment is in U.S. stocks with growth potential.

The 4% rule assumes that you invest at 4% or more per year. 4% is based on the historical U.S. S&P stock growth rate of 7% per year to 4% is the historical U.S. S&P stock growth rate of 7% per year minus the inflation rate (price inflation) of 3%. Japan’s inflation rate is less than 1%, making it a more FIRE-friendly environment. However, 4% per year is a figure that cannot be achieved without taking a certain amount of risk. Moreover, taking risk does not guarantee results, and the investment approach is very important in FIRE.

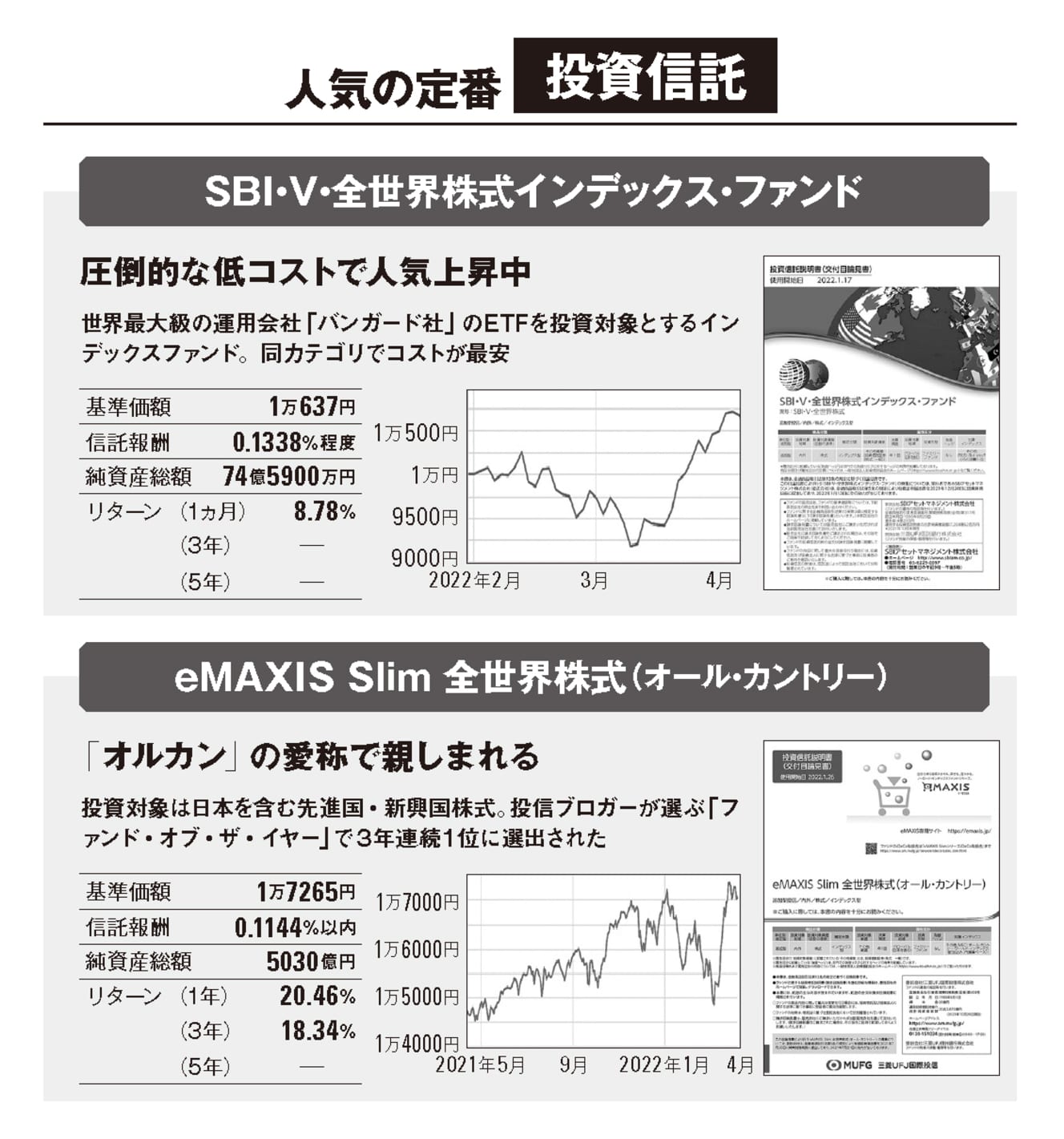

How did successful FIRE participants increase their assets? In our interviews, we found out that mutual funds, stocks, and ETFs were the key factors. All of these investments are purchased regularly for a fixed amount over a long period of time, which reduces risk and facilitates the generation of profits.

The main investment destination is U.S. stocks. The U.S. is home to giant IT companies such as Apple, Microsoft, and Amazon.com, as well as large, well-established companies such as Coca-Cola and P&G, which drive the global economy.

Investment trusts and ETFs that are linked to major U.S. stock indices (e.g., S&P 500 and NY Dow) can be used to directly invest in U.S. stocks. ETFs that track major U.S. stock indices (S&P 500, NY Dow, etc.) allow you to ride the wave of U.S. stock growth directly. Index-type investment trusts that track stocks in developed countries or global stocks are also a good choice. Although they are called “developed countries” or “global,” 60-70% of their investments are in U.S. stocks.

Although the risk is higher than mutual funds, investing in individual U.S. stocks for higher returns is also an option. Not only can you aim for gains in price, but U.S. stocks emphasize shareholder returns through dividends, and there are many stocks that can achieve a dividend yield of 4% alone.

Investing in the world’s largest economy is the shortest route to FIRE.

FIRE practitioners speak! Five Key Success Factors

Learn from short-term investment failures and shift to accumulation investment

Successful FIRE practitioners did not always succeed in managing their assets. Through twists and turns, they have established their own optimal investment methods. Let’s hear what these successful people have to say.

Two years ago, Mr. “Dream Father” applied for early retirement and achieved FIRE. He had incurred significant losses in his previous investments. When he started investing in 1998, he mainly invested in individual stocks and FX, and increased his assets to 20 million yen in about 10 years. He has been a major investor since then, but he has lost a lot of money in the past. However, the Lehman Shock of 2008 reduced his assets to one-quarter. For several years, he kept his distance from investments.

In the years that followed, I experienced the birth of my daughter and the death of my father. With my inheritance in hand, I decided to start studying investment seriously this time and read many investor blogs and books. That’s when I came across the savings-investment method,” said Mr. Yumemiru.

Although you cannot expect big returns in the short term with indexed investment, you can steadily increase your assets with low risk. By allocating assets to Japan, developed countries, and emerging countries, he has built a portfolio that can withstand changes in global conditions. In 12 years, he started investing in savings with a principal of 24 million yen, adding 3 to 4 million yen per year.” In 2008, when he was 50 years old, he applied for early retirement, and together with his retirement benefits, his assets exceeded 100 million yen and he achieved FIRE.

‘Now I’m re-employed and working lightly. But I am living the carefree life I always dreamed of when I was a company employee, enjoying time with my family as well as my hobby of watching movies,” (Mr. Dreamy Dad).

A couple with different values built a 100-million-yen fortune in just 10 years.

Mr. and Mrs. Gumi Pang achieved side FIRE in their 30s while raising a young child. The first thing they did was to improve their family budget. By keeping a household account book, they were able to visualize and review waste, and as a result, they succeeded in reducing their annual expenses to 3 million yen. By thoroughly adhering to the principle of “Income – Expenses = Investment” and putting 4.5 to 6 million yen per year into investments, they were able to surpass 100 million yen in assets in just 10 years from 2011, the year they started investing. This was the secret to their success in achieving FIRE.

The couple’s main investments are in individual U.S. stocks. Among them, Amazon.com and Apple, which they purchased in 2002, soared tenfold and fivefold, respectively, to a combined total of 45 million yen. They were the driving force behind the realization of FIRE.

They also said that the most important thing for a couple to achieve FIRE together is to reconcile their values.

My wife wants to cherish the present and trust her intuition, while I think theoretically and value the future. We had many conflicting opinions and fought a lot. But as we worked toward the common goal of achieving FIRE, we came to understand the differences in our values. I believe that if we continue to set a clear vision for ourselves and our family, putting our happiness first, we will be able to overcome some difficulties.

From the May 20-27, 2022 issue of FRIDAY

Interview and text: Fujiko Sakai (Kaiyusha), Shikiko Nagai Design: Maki Murakami