Why “Smartphone Bank, 1st Generation” Deposit Interest Rates 150 Times Higher than Megabanks Are Possible

The age of inflation has arrived! Review “deposits” as a means of asset defense.

The price increases of food, daily necessities, sundries, gasoline, and other items have not stopped. Slowly but surely, the wave of inflation is coming. On the other hand, there is not the slightest sign of an increase in income, and it is difficult to take the plunge into asset management in the face of an unstable stock market. In such a situation, why not review your savings as a means of increasing your money, even if only a little?

With interest rates at almost zero, bank accounts have long been mere money repositories, but recently, online banks and smartphone banks have appeared that are bringing interest rates back to life. Will this trend continue in this period of radical change in the banking industry? We look ahead to the future, introducing some forward-looking banks.

Smartphone banks with interest rates 150 times higher than megabanks.

In January 2022, Japan’s second bank specializing in smartphones was launched. It is UI Bank, a subsidiary of Tokyo Kiramboshi Financial Group. The term “smartphone specialized bank” may sound unfamiliar, but it refers to a bank where banking services, from account opening to deposits, withdrawals, and transfers, can be completed using only a smartphone application. The first such bank in Japan was Minna-no Bank, established in May 2009 under the umbrella of Fukuoka Financial Service, and is better known in the financial industry as a “digital bank” (hereinafter referred to as a “smartphone bank”).

The design and operation of the application was innovative and differentiated it from conventional banking applications. However, the key features, such as interest rates and various fees, remain on par with those of existing online banks.

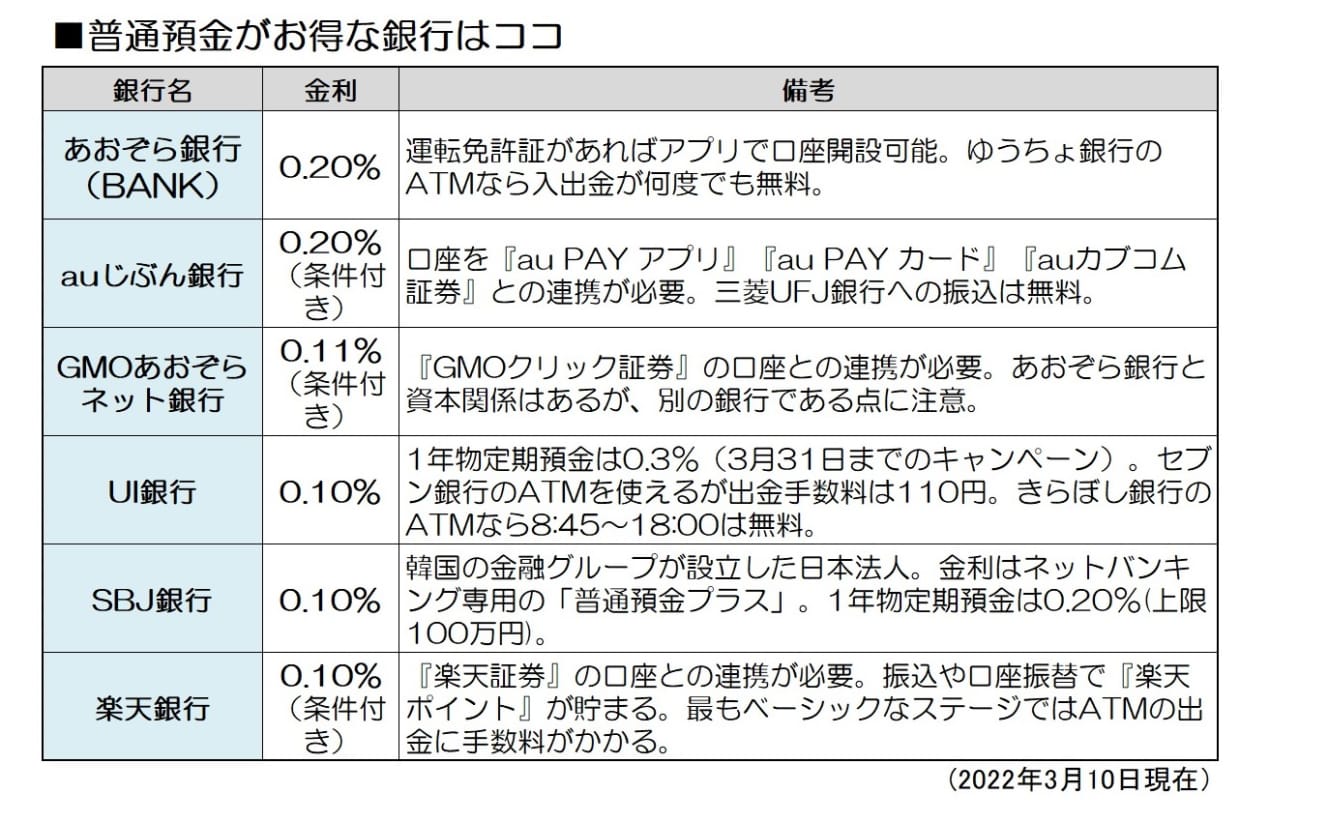

In this regard, UI Bank offers a transfer fee of 86 yen (including tax, regardless of the amount) for transfers to other banks. The same applies below). Moreover, the interest rate on savings deposits is 0.1% (before tax. The interest rate on savings deposits is 0.1% (before tax; same below), while the interest rate on one-year time deposits is set at 0.3% as part of a campaign. Megabanks’ savings accounts offer 0.001%, which is simply 100 times higher, and one-year time deposits offer 0.002%, which is 150 times higher. Almost no major online bank offers this level without conditions.

Many foreign digital banks differentiate themselves from existing banks in terms of interest rates and fees, in addition to the ease of application operation. In this sense, it can be said that a smartphone bank that is typical of digital banks has appeared in Japan.

Savings account interest rate of an astounding 0.2%.

On the other hand, some existing banks also offer attractive interest rates. The first of these is Aozora Bank. In its “BANK” account for individuals, the interest rate on savings deposits is a whopping 0.2%. Moreover, this is not a campaign, nor is it a preferential interest rate that is applied when conditions set by the bank are met. The interest rate on one-year fixed term deposits is also as high as 0.2%, but savings accounts are probably more convenient. The interest rate has been set at this rate since 2019, when it was lower than the current rate, so it is unlikely to be lowered in the foreseeable future.

Aozora Bank, originally the bankrupt Nippon Credit Bank, has been promoting digitalization since 2015, when it paid off its public funds; in 2019, it will relaunch its traditional services for individuals as “BANK,” and in 2021, it will stop handling cash and accepting new accounts from individuals at its real branches. In 2021, the bank will cease handling cash and accepting new accounts from individuals at its real branches, transforming itself into an “almost online bank. The interest rate reflects the cut in various expenses.

There is more! Savings accounts with a little more savings

Other banks that are doing well, based on savings accounts, include au Jibun Bank,GMO Aozora Net Bank,SBJ Bank, andRakuten Bank. For example, au Jibun Bank offers an interest rate of 0.2% with the “au PAY App,” “au PAY Card,” and “au Kabu.com Securities” all working in tandem.

Every bank is a smartphone bank.

It has been more than 20 years since the birth of online-only banks with no real branches; since the late 2000s, banks have been setting up online branches in rapid succession, the number of accounts has expanded dramatically, and online banking has become fully established. The Minna-no Bank and UI Bank mentioned above are not only the “first generation” of smartphone banks, but also the “third generation” of online banks. In the future, it is expected that all banks, including existing banks, will be converted to smartphone banking.

Over the past few years, banks have accelerated the consolidation of branches and the reduction of ATMs. Many banks have been streamlining their operations, using smartphone applications to compensate for the decline in customer service. With no signs of a turnaround in the profit environment, these cost-cutting measures will not be reversed and, therefore, the enhancement of services through smartphone applications will not stop.

Banking agency business” that allows ordinary companies to become banks

In fact, other industries are also entering the smartphone banking market. These include “JAL NEOBANK” by Japan Airlines, “T NEOBANK” by Culture Convenience Club (T Point), and “Yamada NEOBANK” by Yamada Denki. These banks do not have original banking licenses, but are licensed as bank agents to provide banking services. In addition to deposits and transfers, JAL NEOBANK and Yamada NEOBANK also offer card loans and mortgage loans. They offer almost all the services available at a bank.

Such banks without banking licenses are called “NeoBanks ” overseas. NeoBanks began appearing in the United States around 2010, and have now spread to Europe, Asia, Africa, and Latin America. In Japan, the environment has been improved by the revised Banking Law enacted in 2018, and JAL NEOBANK finally started as the first one in 2020. In a broader sense, the three NEOBANK banks may be considered part of the first generation of smartphone banks.

Minna no Bank and UI Bank have a banking license, but Neobank’s is only a banking agency. However, there is no difference in the services available as a smartphone bank, and Neobank currently has a larger lineup. For users, the presence or absence of a license would not make much difference. It is more important to have services that are profitable and easy to use (note that deposits in the banking agency business are also covered by the deposit insurance system).

Connect to existing platforms and transform into a bank

But why would JAL or Yamada Denki be able to conduct banking business, albeit by proxy? In very simplified terms, we are borrowing the online banking platform of our partner bank. JAL NEOBANK, T NEOBANK, and Yamada NEOBANK use SBI Sumishin Net Bank’s “NEOBANK” platform.

SBI Sumishin Net Bank is not the only bank providing the platform. For example, GMO Aozora Net Bank has already announced a business alliance with [HIS]. SBJ Bank, which was picked up in the savings account interest rate table, has actually partnered with UI Bank. Furthermore, Minna-no Bank and au Jibun Bank have also indicated their intention to become providers.

The provision of a financial services platform to companies, as explained so far, is called “BaaS (BaaS). It is an acronym for “Banking as a Service. In fact, the battle for leadership over BaaS is now in full swing as we enter an era in which bank tellers and ATMs are being consolidated into smartphones. This is because the benefits, such as the accumulation of user data, will be immeasurable if more financial institutions and general companies adopt their own platforms.

Incidentally, the UI Bank mentioned at the beginning of this article has been able to offer high interest rates from the beginning because it uses SBJ Bank’s platform. Minna-no Bank has built its own platform, and the upfront investment is a burden, so it is not currently able to demonstrate its superiority in terms of interest rates.

Will increased competition benefit the campaign?

The more competition in the financial industry increases, the more opportunities there are for individual users to benefit from campaigns. In the near future, SBI Sumishin Net Bank plans to list on the First Section of the Tokyo Stock Exchange. The three neo-banks are still running individual campaigns, but we expect that SBI Sumishin Net Bank itself will also launch a campaign upon its listing.

Although some may say, “Even if the interest rate is a little high, the interest is not worth a tear of a sparrow,” we would like to increase our antennae to find out more about the special services available.

Interview and text: Kenji Matsuoka

After working as a money writer and financial planner/market analyst for a securities firm, he became independent in 1996. He writes articles on finance and asset management mainly for business and economic magazines. Author of "Textbook for the First Year of Robo-Advisor Investing" and "Understanding with Rich Illustrations! Cashless Payments for the Absolute Benefit of Cashless Payments". He is also a credit card guide for the information website "All About".