Fear of “5% Overseas Fees” for Credit Cards! Next Generation Credit Cards: The True Identity of Next Generation Credit Cards to Prevent the “Unwary” from Losing Too Much Money without Knowing It

A big loss overseas? Fear of 5% commission fee

A situation has arisen that will hit the wallets of those who love to travel abroad. The “overseas handling fee” that is charged each time a credit card is used overseas has not stopped rising.

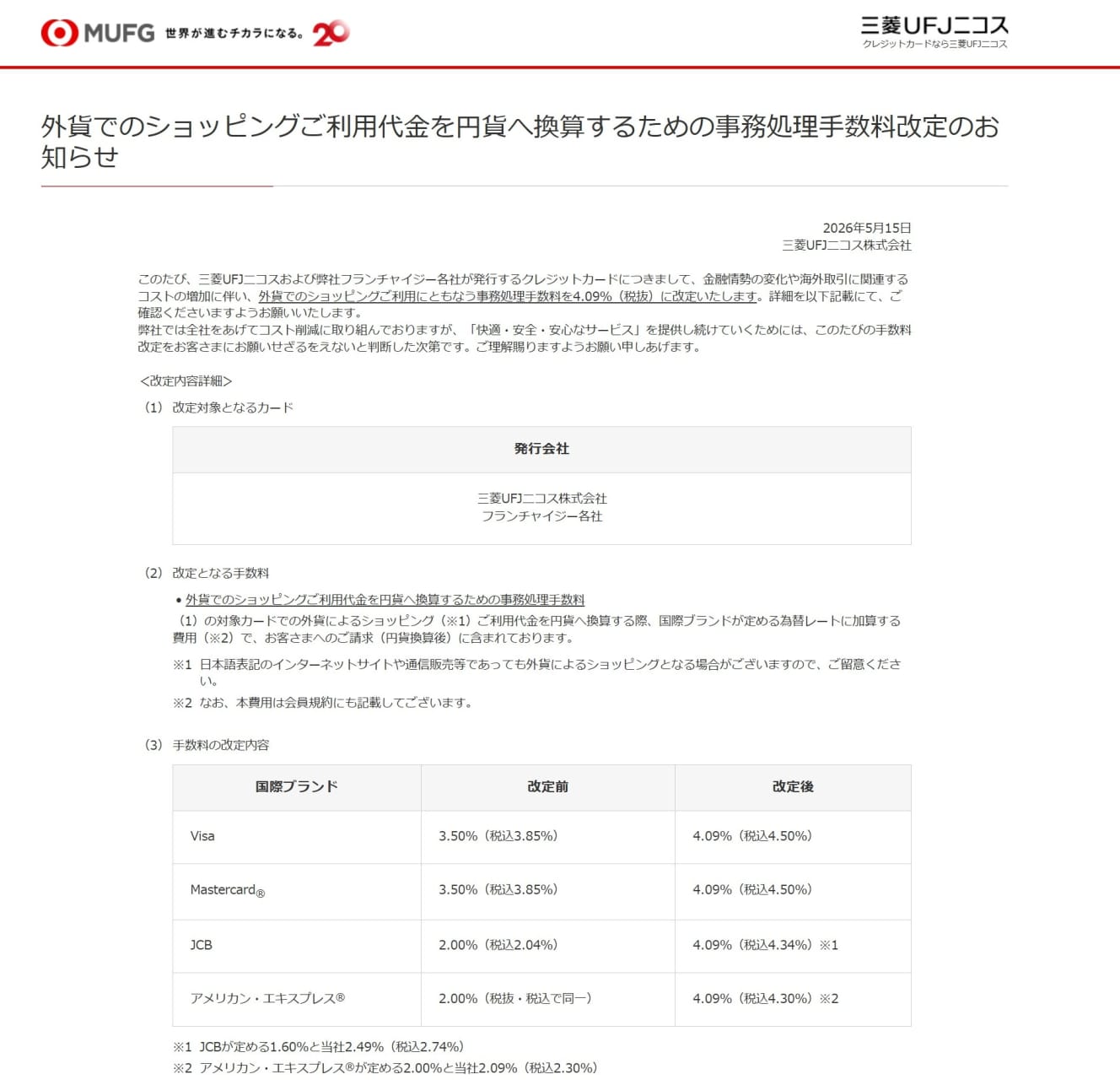

Until a few years ago, it was common for all credit card companies to charge 1-2%, but now 3.85% is the norm. In May of this year, Mitsubishi UFJ NICOS announced that it would raise its fee to 4.09% for all brands, effective November 16. Including consumption tax, this means that approximately 4.5% of the total amount spent will disappear as fees. There is a strong possibility that other companies will follow suit in the future.

If you spend 1,000,000 yen overseas, you will be charged 45,000 yen as a fee; even 100,000 yen will cost 4,500 yen. This is not a small amount for anyone. It is no exaggeration to say that if you use a conventional credit card to pay for travel and other foreign currency transactions locally or even in Japan, you will “lose a lot of money just in fees” if you settle the transaction as it is.

The Circumstances Behind the Continued Rise in Fees

Why have credit card fees continued to rise one after another? We asked Kenji Matsuoka, a money journalist and expert on credit cards, why.

The direct cause is the rise in short-term interest rates due to the Bank of Japan’s (BOJ) policy rate hike. In the case of credit card companies, when short-term interest rates rise, funding costs also rise, putting pressure on profits.

In addition, the high cost of hedging foreign exchange is also having an impact. These are like “insurance premiums” that companies that engage in foreign exchange transactions pay to limit foreign exchange losses. Although they have declined from their peak about two years ago, they have remained high due to the recent rise in US interest rates. This hedging cost is also a factor that puts pressure on the earnings of credit card companies.

As long as the yen continues to depreciate in Japan, hedging costs are unlikely to fall. Therefore, they will have no choice but to raise their overseas transaction fees involving foreign exchange transactions.

After Mitsubishi UFJ NICOS announced an increase to 4.09% for all brands, other companies have so far not followed suit. However, Mr. Matsuoka said, “Some card companies are trying their best, but they will probably follow suit.

June is the peak month? Further Price Hikes Coming

What everyone is worried about is the possibility that other companies will follow suit and raise other fees as well. Mr. Matsuoka says that June will be the biggest point of the year.

The BOJ will hold its Monetary Policy Committee meeting in June. There is a high possibility that the BOJ will raise interest rates at this meeting, and the market is expecting another rate hike within this year (2014). If the BOJ does so, short-term interest rates will rise further, which will increase the burden on credit card companies.

If the BOJ raises interest rates and the yen shows signs of appreciation, hedging costs will decline. However, the impact of higher funding costs will be far greater, he said. It will likely lead to increases in various fees, including overseas handling fees.

Pitfalls of the “Wise” topic

One of the reasons why credit card companies have no choice but to raise overseas transaction fees is because of the “weak” yen, which is making the Japanese yen less valuable as a currency. Travelers and business travelers want to choose other means of payment that are “as economical as possible.

The next-generation financial services such as “Wise,” “Revolut,” and “Sony Bank WALLET” are suddenly emerging. Wise,” for example, is an overseas remittance and multi-currency service from the UK that allows overseas remittances and foreign currency management with minimal fees and exchange rates close to those prevailing in the market, and “Revolut” is almost the same.

Mr. Matsuoka said of Wise, “If you look at the fees alone, they are very favorable (compared to credit card companies). The fees are a full digit different,” he said. On the other hand, there are a few things to keep in mind when using Wise and other services for overseas travel.

First of all, there is no “compensation” that is usually included with credit cards. For example, if you have a problem with unauthorized use or overpayment, you will not have the same support as Japanese credit card companies.

Wise only charges a 0.5% to 0.7% overseas administration fee when a debit card is issued and used for payment at local stores. As Mr. Matsuoka mentioned earlier, it is exactly “one digit different. And when Japanese yen is deposited, it is converted to US dollars, euros, or other foreign currencies in real time and at the lowest possible rate. In addition, the debit card can be used only for the amount charged, not a credit card, making it easy to prevent unauthorized use of large sums of money.

On the other hand, the card does not earn points as credit cards do, and a card creation fee (1,200 yen for Wise) is required. It takes one week to 10 days from the time of application to obtain the card. If you are planning to travel abroad, you will want to obtain the card well in advance.

A Series of Changes…The Predicament of Card Companies

In addition to this fee, other so-called “credit card-related” changes have become common in recent years. For example, it is still fresh in the minds of travelers that Priority Pass, which came with the Rakuten Premium Card, was downgraded from unlimited use to five free flights per year. In addition, some Rakuten cards have seen a reduction in the number of Rakuten Points that can be earned based on the amount of purchases made in recent years.

In addition, some credit card companies have increased the annual fee or raised the “quota” for annual payments. In addition, an increasing number of credit cards are “shortening” their payment cycles. This is also due to the increase in funding costs caused by rising short-term interest rates.

Since credit card companies are paying for the use of cards on behalf of users, they are trying to reduce the interest burden by shortening payment cycles. These “changes” are not always announced by the credit card companies, but they are sometimes subtly included in their announcements.

The credit card companies are in a tight financial situation. Japan is sensitive to “price hikes” to begin with, and there is a tendency to make it difficult to raise prices immediately even if overseas conditions are affected. In recent years, credit card companies have already entered an era in which they cannot “compete” on their own, and the mainstream is to “surround” their customers with comprehensive services such as “Rakuten Economic Bloc” and “Docomo Economic Bloc. The presence of credit card companies is declining, and they are no longer “part of the economic sphere.

New Payment Methods to Avoid Losses when Traveling Abroad

Incidentally, it is preferable to make payments in Japan for hotels and other accommodations you plan to stay at during your overseas trip if possible. For example, if you make a reservation through an online travel agency (OTA) such as an official hotel website, Trip.com, or Agoda, and settle the payment after you arrive in Japan, you will be charged an overseas administration fee. However, if you make a reservation in Japan and pay the amount indicated in Japanese, no additional fees are added. However, due to exchange rates, there are cases where the amounts are reversed between the time of reservation and the time of stay, so it is difficult to say for certain, but it is worth keeping in mind.

Using credit cards overseas was once said to be “safer than cash” and “cheaper than exchanging money,” and it is still widely used today. However, with the era of the “5%” service charge looming on the horizon, credit cards are no longer the “most powerful payment route” in the past. In order to avoid losing money on fees and to save as much money as possible on travel expenses, please consider the new generation of payment tools.

▼ Kenji Matsuoka After working as a money writer and financial planner/market analyst for a securities company, he became independent in 1996. Writes articles on finance and asset management mainly for business and economic magazines. Author of “A Textbook for the First Year of Robo-Advisor Investing” and “Understanding with Rich Illustrations! Cashless Payments: The Book You Can Definitely Benefit from”.

Interview and text by: Shikama Aki

Journalist and photographer. Born in Osaka. After graduating from university, joined the Yomiuri Shimbun. After working in the Matsuyama bureau and Osaka head office, he became a freelance photographer. Currently, his main genre of work is travel, especially airplanes and airports. He has extensive experience in both domestic and overseas coverage. She is a lecturer at Nikon College. Co-author of "The Best Travel Guide for Women Traveling Abroad Alone [Latest Edition]" etc. X/ Instagram : @akishikama

PHOTO: Afro