Rent-Level Home Purchase Trap in the 20s Leads to Overpriced Housing Risks and Double Burden of Mortgages and Education Costs

Amid continued rises in housing prices, a government household survey by the Ministry of Internal Affairs and Communications shows that the homeownership rate among people in their 20s (two-or-more-person households) has reached a record high.

Behind this trend are factors such as growing anxiety that “if I don’t buy now, I may never be able to afford a home,” the spread of dual-income pair loans, and the increasing use of ultra-long-term mortgages exceeding 35 years.

However, there is an inherent risk that if household income declines due to events such as childbirth, repayment can quickly become difficult. The idea that a home can be purchased for less than rent, or that it can simply be sold to repay the loan, does not always work out in reality.

The risks of overextending to buy a home are not limited to people in their 20s. Scenarios such as divorce after buying a home with a pair loan, household finances collapsing when peak education costs overlap with mortgage repayments, and post-retirement financial ruin due to continuing mortgage payments are all possible. Beyond the dream of homeownership, a scenario of despair may be waiting.

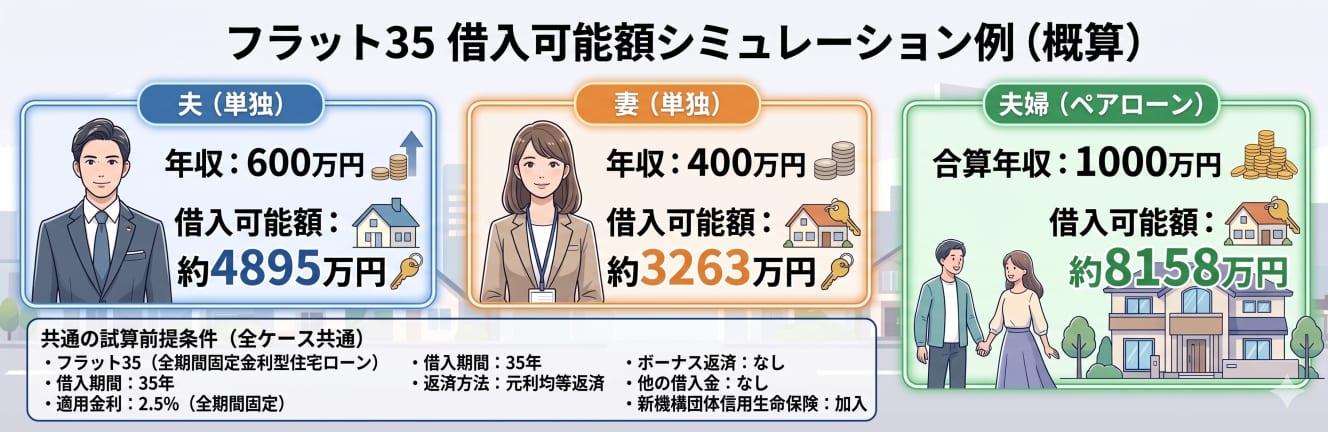

Reasons why young people are rushing to buy at high prices

You have managed to acquire a home of your own. However, a harsh reality may lie ahead.

How childbirth and career breaks disrupt pair loans

In cases where a home is purchased using pair loans or joint and several liability loans based on the combined income of a married couple, there are frequent situations in which repayment becomes difficult due to a reduction in household income caused by retirement, leave of absence, or job changes by either partner.

This risk is especially significant for couples in their 20s and 30s. After childbirth, it is common for wives to take extended leave or resign from work for childcare. Even if they plan to return to work soon after giving birth, various factors—such as the inability to secure a nursery place, slow physical recovery, or the need to care for a child with illness or disability—can prolong their absence. In some cases, this leads to permanent resignation.

Once a long-term career break occurs, even if the person returns to work, their income often decreases, and the original repayment plan can be significantly disrupted.

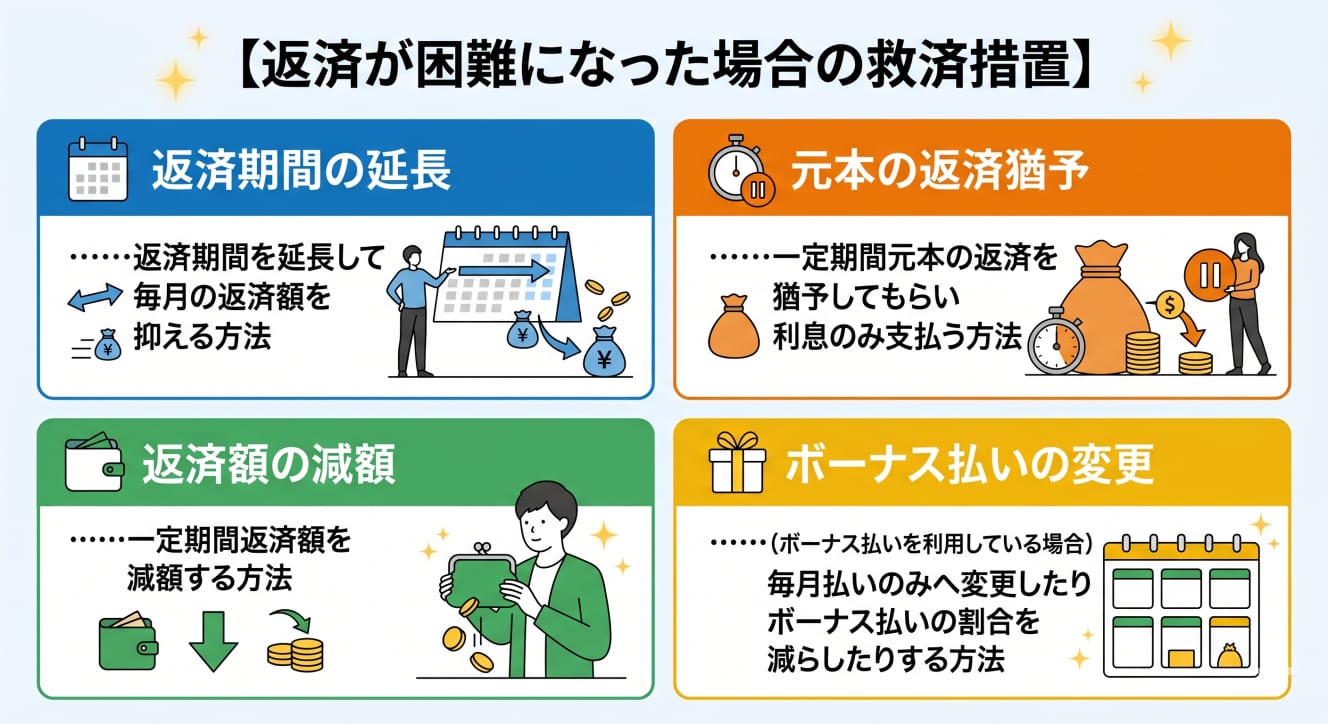

If repayment becomes difficult due to a decline in income, borrowers may be able to receive relief measures such as repayment deferrals or reductions, after undergoing screening by the financial institution that provided the loan.

However, these are only ways to temporarily reduce the burden by postponing repayment. Repayment is not forgiven, and the final burden will increase. If the relief measures are not granted and repayment falls into arrears, the financial institution will demand a lump-sum repayment, and in some cases, if the repayment cannot be made, the couple may be forced to give up the house.

The tragic end of pair-mortgage divorce

It is said that in an era where one in three couples divorces, various problems arise when a home has been purchased before divorce. In particular, cases involving pair loans or joint and several liability loans tend to become especially complicated.

In general, mortgage contracts cannot be changed mid-repayment, meaning that even after divorce, repayment obligations continue until the loan is fully paid off. The simplest solution is to sell the home and repay the loan in full. However, if the loan balance exceeds the home’s appraised value (i.e., a situation known as negative equity), selling the property will not be enough to fully repay the debt. The longer the repayment period, the slower the principal is reduced, increasing the risk of negative equity.

If selling the home is difficult, or if there is a desire to avoid changing a child’s living environment, one option is for one party to remain in the home while continuing to repay the loan. In this case, the party who moves out may still be required to continue paying their share of the mortgage. Combined with paying rent for their own residence, this creates a “double burden” that can be extremely financially difficult.

Pair loans also require caution because each borrower acts as a joint guarantor for the other. If one party falls behind on payments, the other becomes responsible for the full repayment. While it is sometimes possible to dissolve a pair loan through refinancing or consolidating loans, in many cases the remaining borrower’s income alone is not sufficient to pass the screening process, especially when the outstanding loan balance is large.

Education expenses and loans double burden of hell

50-year loan leads to retirement bankruptcy

The trap of you can buy a home for the same amount as rent

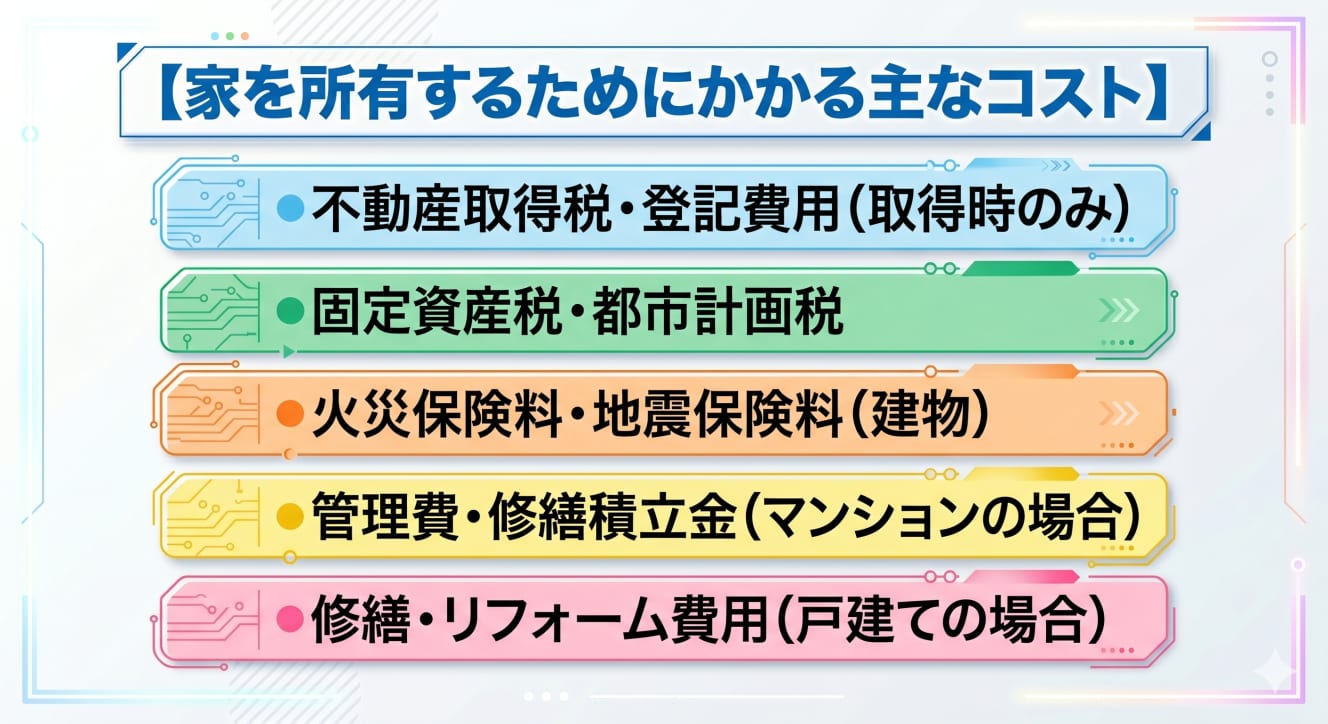

Depending on the property price, in many cases, the cost will increase by several hundred thousand yen to one million yen per year compared to renting. If a variable-rate mortgage is used, there is also the risk that loan repayments will increase due to rising interest rates.

If a home is purchased without taking these costs into account, the possibility increases that income and expenditures will be worse than anticipated and repayment will come to a standstill. It is important to make a financial plan with a margin of safety in anticipation of future increases in fire insurance premiums and reserve funds for repairs.

The end of the real estate bubble. Fear of not being able to sell

“Just sell the house if things go wrong and repay the loan.”

“If it gets too small, you can always upgrade later.”

Buying a home based on the assumption that you can sell it is a strategy that can work well in periods of rising housing prices. Over the past decade, this has often been a successful approach. In fact, in central urban areas, there are not rare cases where the appraisal value of a condominium has more than doubled in 10 years compared to the original purchase price. However, if that assumption breaks down, it can lead to a situation where the property cannot be sold at all.

Due to rising construction material and labor costs, as well as investment demand, new housing prices are likely to remain high for the time being. On the other hand, in the used housing market, the gap between listing prices and actual transaction prices is widening, and in some areas, price declines have already begun.

Going forward, the working-age population—the main group of homebuyers—is expected to decline, while inherited properties from the baby boomer generation will increase the supply of used homes and land. If buyers decrease while supply increases, housing prices may fall, especially for used homes and detached houses that are less attractive as investment assets.

In such an environment, taking on large, long-term mortgages based on expectations of price appreciation or easy resale carries significant risk. When purchasing a home in the future, it will become increasingly important to choose a property that fits one’s income and long-term life plan, with the assumption that one will continue living there.

Buying a home itself is not a bad decision. However, rushing into a purchase simply because others are doing so should be avoided.

A home that is meant to improve one’s life can instead become a financial burden, forcing people to live under constant stress. It is essential to carefully consider the balance between current living expenses, future education costs, and retirement savings, as well as the costs and risks of home ownership. Decisions about whether to buy, and how much to borrow, should be made carefully after proper financial simulations. If in doubt, it is important to pause and reconsider.

Interview and text: Hiroki Takekuni

Financial planner and representative of Rapport Consulting Office. After graduating from Nagoya University's Faculty of Engineering, he worked for a securities company and an insurance agency before setting up his own business. He is a first-class financial planning technician, CFP®, certified real estate transaction specialist, and sauna and spa professional.