Avoid big losses—check this unexpected tax checklist for your return

“Don’t worry, the company takes care of everything” — salaried workers who think this way may be losing out without even realizing it.

There are cases where it’s better for salaried workers to file a tax return to reclaim taxes, such as when deductions cannot be processed through year-end adjustments or when losses occur from investments. What are those cases? Let’s check with the tax return and tax-saving checklist for salaried workers.

Even company employees can get tens of thousands of yen back? Tax-saving list

Year-end adjustments are a convenient system where the company handles tax procedures on your behalf, but you can’t leave everything to them. To receive the following deductions, you need to file a tax return yourself.

Before looking at the checklist, it’s important to note that deductions fall into two groups: “[A] Income Deductions” and “[B] Tax Credits.”

The names are similar, but their impact is completely different. In short, the [B] group that appears later has overwhelmingly greater tax-saving effects (cash back).

The mechanism becomes clear if you look at the tax formula:

Income Tax = (Income – [A] Income Deductions) × Tax Rate – [B] Tax Credits

[A] Income Deductions (medical expense deduction, hometown tax donation, etc.) these reduce the amount subject to taxation. Subtract [A] from your annual income, then multiply the remaining amount by the tax rate (5%–45%) to calculate the tax. In other words, it reduces income before applying the tax rate.

[B] Tax Credits (mortgage deduction, dividend credit, etc.) these are directly subtracted from the tax amount itself. Even if the calculated tax is 100,000 yen, if [B] is 100,000 yen, the tax owed becomes zero. In other words, 100,000 yen in [B] is equivalent in value to cash 100,000 yen.

So, which cards (deductions) do you have at hand? Let’s start by checking the [A] group.

The trick to turning pharmacy receipts into cash

[A] – <Income deductions> requiring a tax return

◇ [A-1] Medical Expense Deduction

You can claim the medical expense deduction if the total amount of medical expenses paid that year for yourself or your spouse/relatives living with you, minus any insurance reimbursements, exceeds 100,000 yen (or 5% of total income if your total income is less than 2 million yen). The deduction amount is calculated as follows (up to 2 million yen).

“Medical expenses” can be combined for all family members living together. If income is below 2 million yen, it only needs to be 5% of income, so for those earning around 3 million yen, the threshold is lower.

“Medical expenses” can be combined for all family members living together. If income is below 2 million yen, it only needs to be 5% of income, so for those earning around 3 million yen, the threshold is lower.Expenses eligible for medical deduction include treatment costs, commuting costs to the hospital, and the purchase of medical devices directly needed for treatment. However, expenses for disease prevention or cosmetic purposes, as well as gratuities, are not eligible.

Commuting costs by train or bus are also eligible. Often forgotten are children’s orthodontics and therapeutic massages. Cosmetic or preventive treatments are not eligible, but if it’s for treatment, a wide range is accepted.

Commuting costs by train or bus are also eligible. Often forgotten are children’s orthodontics and therapeutic massages. Cosmetic or preventive treatments are not eligible, but if it’s for treatment, a wide range is accepted.To claim the medical expense deduction, you must attach a medical expense deduction certificate summarizing eligible medical expenses to your income tax return. Originals are not required, but receipts must be kept for five years.

◇ [A-2] Self-Medication Tax System

Those who engage in certain activities to maintain and promote health or prevent disease, such as health checkups, medical screenings, and vaccinations, and who purchase more than 12,000 yen of eligible medicines in that year for themselves or their spouse/relatives living with them, can apply the self-medication tax system instead of the medical expense deduction.

You cannot combine this with the medical expense deduction. Calculate which is more beneficial. Eligible medicines are indicated on receipts with a “★” mark or similar. For 12,000 yen, many people can reach this amount just by stocking over-the-counter medicines.

You cannot combine this with the medical expense deduction. Calculate which is more beneficial. Eligible medicines are indicated on receipts with a “★” mark or similar. For 12,000 yen, many people can reach this amount just by stocking over-the-counter medicines.A list of medicines eligible for the self-medication tax system is posted on the Ministry of Health, Labour and Welfare website, and receipts at the time of purchase indicate eligibility.

To apply the self-medication tax system, you must attach a self-medication tax system certificate summarizing eligible medicine purchases to your income tax return. Originals are not required, but receipts and documents proving the health-promoting activities must be kept for five years.

Common traits of people who lose out with hometown tax payments

◇ [A-3] Donation Deduction (“Hometown Tax Payment,” etc.)

Those who made hometown tax payments without using the one-stop exception, or who donated to the national or local governments, or to specified public interest promotion corporations (organizations designated by the government for significant contribution to education, science, culture, social welfare, etc.), can apply for a donation deduction (officially called contribution deduction) by filing a tax return. If the donation qualifies as a specified donation eligible for deduction, the receipt usually indicates that it is eligible for donation deduction.

If you file a tax return for medical expense deductions or other deductions, the one-stop exception for hometown tax payments becomes invalid. In that case, you must also enter the hometown tax payment on your tax return again, or it will count as just a donation, so be careful!

If you file a tax return for medical expense deductions or other deductions, the one-stop exception for hometown tax payments becomes invalid. In that case, you must also enter the hometown tax payment on your tax return again, or it will count as just a donation, so be careful!To claim the donation deduction, you must record relevant information about the donation deduction on your tax return and attach or present the receipt of the donation issued by the organization, along with any documents required depending on the range (recipient) of the donation.

■ Hometown Tax Payment One-Stop Exception

The one-stop exception is an exception measure for donation deductions under the hometown tax system. If all the following requirements are met, you can receive the donation deduction without filing a tax return.

[Requirements to use the one-stop exception for hometown tax payments]

□ You are a salaried employee

□ You do not receive salary or other payments from more than one source

□ Your annual income (total annual salary) is 20 million yen or less

□ You have no income other than salary income

□ The number of municipalities you donated to this year is five or fewer (if you donate multiple times to the same municipality, it counts as one)

□ You do not plan to file a tax return

If these requirements are met, you can apply for the hometown tax one-stop exception to each municipality you donated to, and filing a tax return becomes unnecessary. Application methods include applying online using your My Number card or submitting the required documents by mail.

Even if you apply for the one-stop exception, filing a tax return or donating to six or more municipalities will invalidate all applications. In that case, you must file a tax return for all donations to receive deductions, so be careful.

Suit costs as expenses? Deductions for salaried workers

◇ [A-4] Casualty Loss Deduction

If a disaster, theft, or embezzlement damages assets necessary for daily life owned by yourself or your spouse/relatives living with you, whose income for that year (total income) is 480,000 yen or less, you can claim the casualty loss deduction by filing a tax return.

Not only disasters but also theft and embezzlement are eligible; fraud is not. In addition to the damage amount, costs for restoration or demolition can also be counted as disaster-related expenses.

Not only disasters but also theft and embezzlement are eligible; fraud is not. In addition to the damage amount, costs for restoration or demolition can also be counted as disaster-related expenses.To apply the casualty loss deduction, you must record relevant items on your tax return and attach or present receipts for unavoidable expenses related to the disaster, etc.

If your income for that year is 10 million yen or less, instead of the casualty loss deduction, you may apply the income tax reduction/exemption under the Disaster Relief Act (explained later).

◇ [A-5] Specific Expenditure Deduction

If a salaried worker (salary income earner) incurs specific expenditures for work in the following items ①–⑦, and the amount exceeds half of the salary income deduction, you can receive an income deduction for the excess amount by filing a tax return.

[Expenditures qualifying as specific expenditures]

① 《Commuting expenses》Expenditures deemed normally necessary for commuting as a regular commuter

② 《Business travel expenses》Expenditures normally necessary for travel directly required to perform duties away from the workplace

③ 《Relocation expenses》Expenditures normally necessary for relocation due to a job transfer

④ 《Training expenses》Expenditures for training directly required to gain skills or knowledge necessary for duties

⑤ 《Qualification acquisition expenses》Expenditures to acquire qualifications directly required for duties

⑥ 《Home travel expenses》Expenditures normally necessary for travel between home and workplace or residence in the case of living away from home

⑦ 《Necessary work expenses》Expenditures required for work, such as books, clothing, entertainment, etc. (up to 650,000 yen)

To qualify as specific expenditures, proof from the payer of the salary that the expense is directly necessary for performing duties is required (for ④ or ⑤ related to education/training, certification by a career consultant is also acceptable).

Additionally, parts of these expenses that are reimbursed tax-free by the salary payer, or covered by education training benefits or child-support (single-parent) self-reliance education training benefits, are not included as specific expenditures.

To claim the specific expenditure deduction, you must attach a certificate to your tax return showing that the expenditures were directly necessary for your duties, and attach or present documents proving the fact and amount of the expenditures.

Recovering Taxes with Mortgage Loans and Stocks

[B] _Tax Credits Requiring a Tax Return

◇ [B-1] Mortgage Loan Deduction (First-Year)

If you use a mortgage loan to build, acquire, or renovate a home and meet certain requirements, you are eligible for the mortgage loan deduction (special deduction for housing loans) and can receive a deduction from income tax (if the deduction exceeds your income tax, it can also be applied to next year’s residential tax). In the first year you receive this mortgage loan deduction, a tax return is required.

The deduction amount is 0.7% of the remaining balance of the mortgage loan used to acquire the house and its land. The limit on the eligible mortgage loan balance (maximum amount) varies depending on the environmental performance of the house; for those moving in during ’25 or ’26, the maximum is 45 million yen (50 million yen for households with children under 19 or young couples with either spouse under 40). The deduction period is up to 13 years (up to 10 years for used homes).

To apply for the first-year mortgage loan deduction, you must attach documents corresponding to the type of house on your tax return. Specific required documents are listed on the National Tax Agency’s website.

From the second year onward, submitting the “Mortgage Loan Deduction Certificate” issued by the tax office to your employer allows you to receive the deduction via year-end adjustment.

◇ [B-2] Dividend Deduction

Dividends from stocks or distributions from investment trusts are taxed at the source as dividend income, so in principle, no tax return is required.

However, there are cases where filing a tax return is advantageous:

① If you incurred losses (capital losses) from stock or investment trust transactions and offset them against dividend income (tax loss offset), you can get a tax refund (explained later).

② If combining dividends with other income lowers your income tax rate.

In case ②, filing a tax return and selecting comprehensive taxation for dividend income allows you to receive the dividend deduction.

Considering also the burden of resident tax, choosing comprehensive taxation is advantageous if taxable income including dividends is under 6.95 million yen.

Taxable income is the amount after subtracting income deductions such as salary deduction, spouse deduction, and basic deduction from total income including dividends, and differs from nominal annual income. For those with only salary income, taxable income of 6.95 million yen corresponds roughly to an annual salary of 10 million yen (varies with deduction amounts).

Depending on the dividend amount, salaried workers with an annual income (salary) of 10 million yen or less may benefit from filing a tax return and choosing comprehensive taxation for dividends.

If taxable income is 6.95 million yen or less (annual income ~10 million yen), selecting comprehensive taxation and applying the dividend deduction is advantageous in most cases. However, be aware that national health insurance premiums and other costs may increase.

If taxable income is 6.95 million yen or less (annual income ~10 million yen), selecting comprehensive taxation and applying the dividend deduction is advantageous in most cases. However, be aware that national health insurance premiums and other costs may increase.◇ [B-3] Foreign Tax Credit

If a resident of Japan earns income overseas (including foreign stock dividends, etc.) that is taxed locally and also taxed in Japan, filing a tax return allows the local taxes paid to be deducted from your income tax (including special reconstruction income tax) for that year. This is the foreign tax credit.

To claim the foreign tax credit, you must attach a statement regarding foreign tax credit and documents proving foreign income taxes were imposed to your tax return.

Note: Capital gains from foreign stocks are generally taxed only in Japan under tax treaties with many countries, so they are not eligible for the foreign tax credit. However, foreign stock dividends are taxed locally and again in Japan after tax, making them eligible for the foreign tax credit.

◇ [B-4] Special Deduction for Donations

For certain donations eligible for income deduction as contribution deductions, you can instead apply for a tax credit called the special donation deduction (*includes special deduction for political party donations, special deduction for certified NPO donations, and special deduction for public interest incorporated associations donations).

For donations eligible for the special donation deduction, the receipt usually indicates that it qualifies.

To apply for the special donation deduction, you must record the amount to be deducted on your tax return and attach a calculation statement and supporting documents according to the donation recipient.

If a donation meets the requirements for both contribution deduction (income deduction) and special donation deduction (tax credit), creating the tax return using the National Tax Agency’s tax return preparation portal will automatically select the deduction that results in the lowest income tax based on the on-screen instructions.

◇ [B-5] Reduction/Exemption of Income Tax under the Disaster Relief Law

If the damage to your home or household goods caused by a disaster exceeds half of their current value after subtracting any insurance compensation, and your total income for the disaster year is 10 million yen or less, you can apply for a reduction or exemption of income tax under the Disaster Relief Law if you do not claim the casualty loss deduction (“zasson kōjo”).

You can choose whichever is more advantageous between the casualty loss deduction and the Disaster Relief Law. High-income earners cannot use this (income exceeding 10 million yen). Depending on income, this is a powerful system that can fully exempt income tax.

To apply for the income tax reduction/exemption under the Disaster Relief Law, you must indicate on your tax return that you are applying, along with details of the damage and the amount of loss. Filing a tax return is required.

Even deductions forgotten in year-end adjustments can be claimed through a tax return

With a tax return, you can claim all deductions, including those that can be applied in the year-end adjustment. If you forgot to declare deductions such as life insurance premiums or small enterprise retirement plan contributions (iDeCo contributions) during year-end adjustment, you can claim them yourself through a tax return.

■ Investment losses can be offset or carried forward through a tax return

Even if you made a profit from stock transactions, if you are using a specified account with withholding, a tax return is generally not required. However, if you incurred a loss, filing a tax return allows you to offset losses against profits from other brokerage accounts (loss carryforward) or carry forward the loss to future years.

By offsetting gains, your taxable profits decrease, which saves taxes (withheld taxes may be refunded). Carried-forward losses can be offset against future profits, providing similar tax-saving effects. Note that tax savings occur only when there is a net profit requiring tax payment; if there is no profit, there is no effect.

■ If income from side jobs exceeds 200,000 yen, you must file a tax return

If your side job generates income over 200,000 yen, you are required to file a tax return. This is not an optional action for tax savings but a legal obligation to pay taxes.

Also, note that the threshold is based on income, not revenue—income being revenue minus necessary expenses to earn that revenue.

Smartphone-friendly! Quick refunds at home!

The tax return procedure can be completed at home using a smartphone or computer and a My Number Card.

The biggest advantage is speed of deposit. Refunds are deposited in about three weeks—faster than paper submissions—and there’s no need to stand in line at the tax office or pay transportation costs (according to the National Tax Agency).

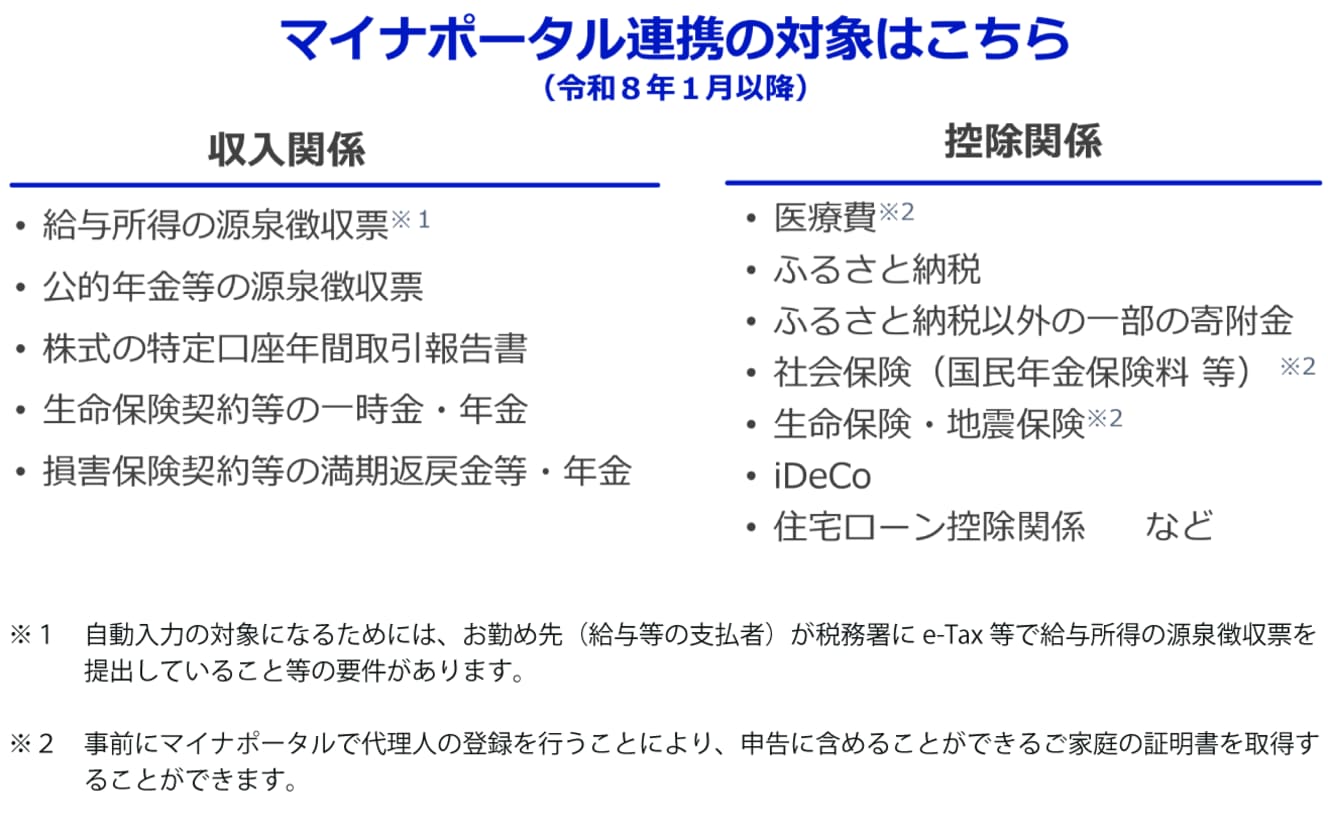

Creating your tax return is as simple as accessing the National Tax Agency’s “Tax Return Preparation Portal,” entering required information according to on-screen instructions. By linking to the My Number Portal, data such as withholding slips, medical expenses, and hometown tax donations can be imported and filled in automatically.

Medical expenses, hometown tax, insurance premiums, and other data are automatically entered. Tedious manual entry and calculation errors are eliminated. This makes filing a tax return so convenient that the impression of it being difficult is completely overturned, so make sure to enable linkage (according to the National Tax Agency).

Once necessary information is entered, income, deduction amounts, and tax amounts are automatically calculated, so you don’t have to calculate them manually. The completed return can be submitted (transmitted) directly to the tax office as data.

The period during which a tax return can be filed for a refund (refund return) is five years from January 1 of the year following the taxable year. Tax returns for offsetting or carrying forward investment losses, and tax returns for side job income (taxable income) must generally be filed between February 16 and March 15 of the year following the taxable year (if the first or last day falls on a Saturday or Sunday, the deadline is the following Monday) (for the 2025 tax year, the period is February 16, 2026, to March 16, 2026).

Although the refund return period is generous, it’s best not to postpone and complete the procedure early.

*The contents of this article are based on tax laws and regulations as of February 2026.

Interview and text by: Hiroki Takekuni

Financial planner and representative of Rapport Consulting Office. After graduating from Nagoya University's Faculty of Engineering, he worked for a securities company and an insurance agency before setting up his own business. He is a first-class financial planning technician, CFP®, certified real estate transaction specialist, and sauna and spa professional.