Flat 35 Is Not the Same Everywhere Choosing the Wrong Bank Can Cost Millions

You lose out if you don’t know this. It wasn’t true that it’s the same no matter where you borrow!

On December 19, the Bank of Japan decided on an additional interest rate hike. As this sent shockwaves through the housing loan market, the number of people turning to the fixed-rate Flat 35 mortgage to avoid interest rate hike risk has been rapidly increasing. However, there’s no need to rush. Aren’t you assuming that with Flat 35, it’s the same no matter where you borrow? In reality, simply choosing a different financial institution can lead to major differences in repayment amounts, screening criteria, and even coverage in the event of an emergency.

It’s also important to note that the applicable interest rate for Flat 35 is not the rate at the time of application, but the rate at the time the loan is actually disbursed (the month of loan execution—generally the property handover date).

Why you can pass screening even right after changing jobs

Flat 35 is a fully fixed-rate home loan with a maximum term of 35 years, jointly offered by the Japan Housing Finance Agency and private financial institutions. Let’s first review the basic features of Flat 35.

◇ Interest rate and repayment amount are fixed from the time of borrowing until full repayment

Because the interest rate and repayment amount are fixed at the time of borrowing through the end of repayment, Flat 35 makes it easier to plan repayments.

◇ Interest rates are higher than variable-rate home loans

Since Flat 35 eliminates interest rate fluctuation risk, its interest rates at the time of borrowing are generally higher than those of variable-rate home loans.

On the other hand, because the Japan Housing Finance Agency bears the lending risk (the risk that the loan cannot be recovered), interest rates are kept lower than those of long-term fixed-rate home loans offered solely by private financial institutions.

◇ Unique screening criteria

Flat 35 is a home loan designed to support the acquisition of high-quality housing, and its screening places heavy emphasis on the property itself (housing performance). To use Flat 35, the property must meet technical standards set by the Japan Housing Finance Agency, and a property inspection must be conducted to obtain a certificate of conformity.

Meanwhile, screening criteria related to the borrower—such as income, occupation, and health—tend to be more lenient than those of private financial institutions’ home loans. For example, the following types of people may be eligible to apply for and use Flat 35:

・People who changed jobs less than one year ago: Application is possible with just one month’s pay slip

・People on maternity or childcare leave: Application is possible even while on leave, regardless of whether they have returned to work; applicants may use either the previous year’s income or the annualized amount of post-return (or pre-leave) monthly salary, whichever is higher

・People assigned to overseas posts: Application is possible while working overseas or immediately after returning to domestic work

・People whose only income is a pension: Application is possible if the income is continuous; not only public pensions but also private pension insurance benefits can be included as income

・People unable to enroll in group credit life insurance due to health reasons: Since enrollment is not mandatory, people with pre-existing conditions or medical histories may still use Flat 35 (note that some guarantee-type Flat 35 products require enrollment)

◇ Interest rate reductions when conditions are met

Flat 35 offers a system under which interest rates can be reduced by up to 1% per year for a certain period after borrowing if conditions related to family composition (such as households raising children or young married couples) or housing performance are met.

How interest rates differ even with the same Flat 35

Flat 35 comes in two types: the “Purchase-type” and the “Guarantee-type.”

With the Purchase-type, although borrowing interest rates and loan handling fees differ depending on the financial institution, all other product features are the same regardless of where you borrow.

By contrast, the Guarantee-type has certain restrictions, but because financial institutions are allowed to design their own products, differences between lenders tend to be more pronounced. It should be noted that only a limited number of financial institutions handle the Guarantee-type Flat 35. As of December 2025, the only eight institutions accepting new applications are the following:

Financial institutions offering Flat 35 (Guarantee-type):

・SBI Aruhi

・Docomo Finance

・Family Life Service

・Zaikei Housing Finance

・Sumishin SBI Net Bank

・Japan Mortgage Service

・Japan Housing Loan

・Credit Saison

The weight of “¥800,000” created by a 0.1% interest rate difference

Depending on which financial institution you choose for a Flat 35 loan, differences may arise in four areas: borrowing interest rate, loan handling fees, group credit life insurance, and total debt-to-income ratio (repayment ratio).

1. Borrowing interest rate

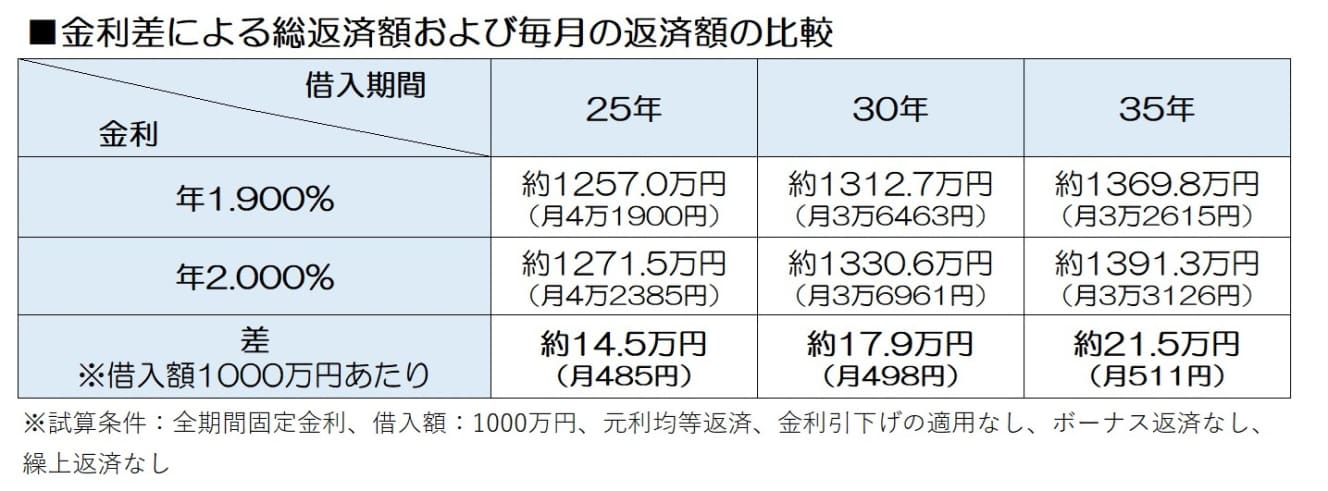

The borrowing interest rate directly affects the repayment amount. Even a 0.1% difference in interest can result in a difference of several hundred thousand yen in total repayment, depending on the loan amount and loan term.

For example, if you borrow ¥10 million and repay it over 35 years, a borrowing interest rate that is 0.1% higher will increase the total repayment amount by approximately ¥215,000. If the loan amount is ¥40 million, the difference grows to about ¥860,000.

Even with a 0.1% difference in interest rates, the total repayment amount can differ by several hundred thousand yen depending on the loan amount and loan term.

Don’t compare loans based only on the fee rate

2. Loan handling fees

Loan handling fees are fees paid to the financial institution that handles a Flat 35 loan. Because each financial institution sets its own loan handling fees, even if all other conditions are the same, the difference can amount to several hundred thousand yen depending on which institution you choose.

There are two ways to pay loan handling fees: a percentage-based type, in which a fixed percentage of the loan amount is paid, and a flat-fee type, in which a fixed amount is paid regardless of the loan amount.

With the flat-fee type, it is common for the borrowing interest rate to be increased in addition to the lump-sum payment (the fixed fee) paid at the time of borrowing. Therefore, when comparing flat-fee loan handling fees, it is necessary to include the increase in repayment amount caused by the higher interest rate. This increase is affected not only by the loan amount but also by the loan term—the larger the loan amount and the longer the loan term, the greater the increase in total repayments.

When comparing flat-fee (fixed-amount) loans, you must include the increase in total repayments caused by any interest rate surcharge in the comparison.

For percentage-based fees, if the loan amount is the same at ¥40 million, there is a ¥440,000 difference in upfront fees between institutions charging 1.1% (tax included) and those charging 2.2% (tax included).

For flat-fee loans, comparisons must factor in the additional repayment burden resulting from the interest rate increase applied on top of the flat fee.

For example, let us compare two products:

Product A: flat fee of ¥550,000 with an annual interest rate increase of 0.1%

Product B: flat fee of ¥550,000 with an annual interest rate increase of 0.2%

Assuming a loan amount of ¥40 million and a loan term of 35 years, the total loan handling cost is approximately ¥921,000 for Product A and ¥1,787,000 for Product B.

Although the flat fee itself is the same, the total cost including the interest surcharge is about ¥866,000 higher for Product B.

3. Group Credit Life Insurance (Danshin)

With guarantee-type Flat 35, group credit life insurance (danshin) is provided by the lending financial institution, so coverage varies by institution. Depending on the coverage, an interest rate surcharge may apply, or a separate insurance premium rider may be required, both of which can affect the total repayment amount.

Some institutions and product plans require enrollment in group credit life insurance. If a borrower is unable to enroll due to health or other reasons, they may not be eligible for that loan.

In contrast, with purchase-type Flat 35, enrollment in group credit life insurance is optional, and the insurance products offered are the “New Group Credit” or “New Group Credit with Coverage for Three Major Diseases” provided by the Japan Housing Finance Agency. As a result, there is no difference among financial institutions.

4. Total Repayment Burden Ratio (Repayment Ratio)

The total repayment burden ratio is the percentage of annual income used to repay Flat 35 and other loans combined. If this ratio exceeds the standard, Flat 35 cannot be used.

For purchase-type Flat 35, the standards are uniform across all financial institutions:

Annual income under ¥4 million: repayment ratio must be under 30%

Annual income of ¥4 million or more: repayment ratio must be under 35%

For guarantee-type Flat 35, some financial institutions impose stricter requirements. If the loan-to-value ratio (the Flat 35 loan amount divided by the construction or purchase price) exceeds 80%—meaning the borrower provides less than 20% in personal funds—the required repayment ratio may be capped at 20% or less.

For example, a borrower with an annual income of ¥5 million and no other debts could borrow up to approximately ¥45.4 million at an annual interest rate of 1.8% over 35 years if the repayment ratio limit is 35%. However, if the repayment ratio limit is 20%, the maximum borrowing amount drops to approximately ¥26 million.

[Real-Name Comparison] Docomo, SBI, ARUHI, and More — A Complete Comparison of Interest Rates and Group Credit Insurance Among the 8 Institutions Offering Guarantee-Type Flat 35

Depending on which financial institution you choose for a Flat 35 mortgage, what kinds of differences arise?

Here, we compare all guarantee-type Flat 35 products offered by the eight financial institutions that currently handle them, along with purchase-type Flat 35 products offered by major lenders, to examine the differences.

Comparing Guarantee-Type Flat 35

As of December 2025, the borrowing interest rates, loan handling fees, group credit life insurance (danshin), total repayment burden ratios (repayment ratios), and key features of the guarantee-type Flat 35 products offered by these eight financial institutions are summarized in the table below.

Among guarantee-type Flat 35 loans, the lowest borrowing interest rate is offered by Docomo Finance. As of December 2025, the applicable interest rate is 1.720% per year when the loan-to-value ratio exceeds 70% and is up to 90%, and drops to as low as 1.670% per year when the loan-to-value ratio is 50% or less.

Why do some banks have interest rates exceeding 4.5%? Understanding the market for purchase-type loans and differences in financial institutions’ strategies

[Comparing Purchase-Type Flat 35]

Although the product features of purchase-type Flat 35 are the same across all financial institutions, borrowing interest rates and loan handling fees differ by lender. If all other conditions are the same, choosing a financial institution with a lower interest rate and lower loan handling fees will help reduce the overall repayment burden.

As of December 2025, borrowing interest rates for purchase-type Flat 35 range from 1.970% per year to 4.510% per year, depending on the financial institution (for loan terms of 21 years or more and up to 35 years, and a loan-to-value ratio of 90% or less).

The most common interest rate is 1.970% per year, which corresponds to the lower end of this range. At financial institutions that adopt a fixed-amount loan handling fee, it is common for an additional 0.1% to 0.2% per year to be added on top of this rate.

The highest interest rate is offered by Sumitomo Mitsui Banking Corporation, at 4.510% per year. The bank’s ultra-long-term fixed-rate mortgage loans (loan terms of more than 20 years and up to 35 years) carry interest rates of 3.33% to 4.23% per year, indicating an intention to steer customers toward its own mortgage products. Among the megabanks, MUFG Bank and Mizuho Bank have suspended new Flat 35 offerings, and Sumitomo Mitsui Banking Corporation may also discontinue handling Flat 35 loans in the future.

Loan handling fees typically range from about 1% to 2% of the loan amount under the percentage-based fee structure, or several tens of thousands of yen under the fixed-amount fee structure. With the fixed-amount fee structure, it is also common for the borrowing interest rate to be increased by an additional 0.1% to 0.2% per year. Some financial institutions offer preferential loan handling fees if certain conditions are met, such as designating the lender’s own account as the repayment account. It is also important to check whether any such fee discounts are available.

A Difference of About 10 Million Yen in Total Repayment FP’s Final Conclusion on Variable vs. Fixed in a Rising-Interest Scenario

With Flat 35, the borrowing interest rate and repayment amount are fixed at the time of borrowing until the loan is fully repaid. The fact that there is no worry about repayment amounts increasing unexpectedly due to rising interest rates during the repayment period provides peace of mind. However, the trade-off is that the borrowing interest rate at the time of borrowing is higher than that of variable-rate mortgages. It’s important to understand that to avoid the risk of future interest rate increases, you will definitely bear a certain difference in interest rates (the difference between variable and fixed rates).

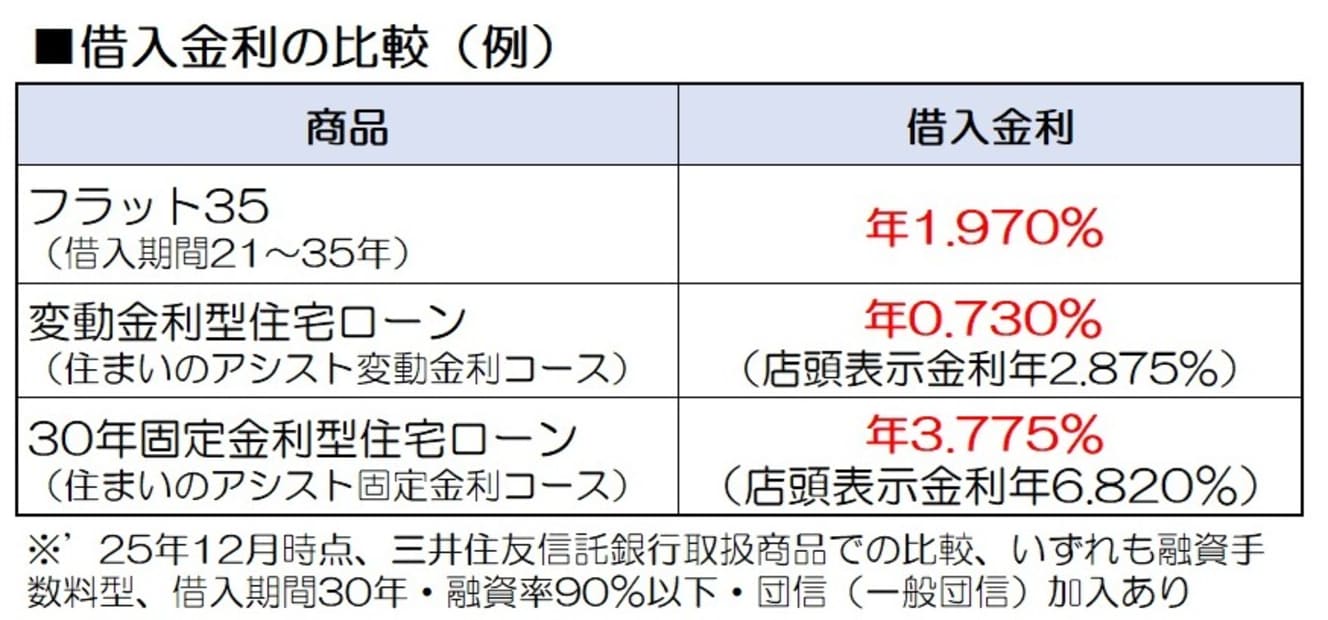

As an example, let’s compare the total repayment for a 35-year loan of 40 million yen. Assuming interest rates remain constant during the repayment period, the total repayment would be approximately 45.34 million yen for a variable-rate mortgage (0.730% per year), and approximately 55.39 million yen for Flat 35 (1.970% per year, no interest rate discount), resulting in a difference of about 10 million yen.

This assumes that interest rates do not change, and if interest rates rise during the repayment period, the difference would narrow, and there is a possibility that the total repayment could even reverse. On the other hand, with Flat 35, you bear higher interest rates during the early repayment period when the outstanding principal is largest, which slows down the pace of principal repayment.

One way to prepare for interest rate increases is to fix the interest rate, but it is also effective to borrow at as low a rate as possible and repay the principal (outstanding balance) quickly. Even if interest rates rise, the impact on repayment is smaller if the principal is reduced. If financially feasible, making extra repayments to reduce the principal can also help mitigate the increase in repayment due to rising interest rates.

Flat 35 is suitable for those who find it difficult to respond if repayment amounts increase mid-loan, or for those who feel stressed by changes in interest rates or repayment amounts. On the other hand, for those who are financially flexible and able to control their repayment schedule, a variable-rate mortgage may be more suitable.

It is important not to assume Flat 35 is the only option, but to compare it with variable-rate mortgages as well, and choose the housing loan that best suits your circumstances.

Note: The content of this article is based on information as of December 2025. When considering using Flat 35, please check the latest information on the websites of the handling financial institutions.

Interview and text: Hiroki Takekuni

Financial planner and representative of Rapport Consulting Office. After graduating from Nagoya University's Faculty of Engineering, he worked for a securities company and an insurance agency before setting up his own business. He is a first-class financial planning technician, CFP®, certified real estate transaction specialist, and sauna and spa professional.

PHOTO: Afro