Explainer: 1.03 Million Yen Income Threshold Updates and What to Check Before Year-End Tax Filing

Could you lose out if you leave your year-end tax adjustment entirely to your company!?

The so-called “¥1.03 million wall” has been making headlines day after day. While attention is focused on how the debate will unfold, are you aware that the 2025 (Reiwa 7) year-end tax adjustment, which directly affects our wallets, is becoming more complex than ever?

This time, there are numerous and complicated revisions, including an increase in the basic income tax deduction and relaxed requirements for dependent deductions.

If you’re thinking, “The company will probably take care of it,” beware. A lighter tax burden is certainly welcome, but the key point to watch out for is that some deductions cannot be applied unless you file a declaration yourself. To avoid losing out, use the ultimate checklist to confirm right now which situations require you to file.

Will the revision to the “¥1.03 million wall” increase your take-home pay?

A comprehensive look at the four major tax changes starting in Reiwa 7

The main points of the Reiwa 7 (2025) tax reform that directly affect year-end tax adjustments are the following four changes:

1_An increase in the basic income tax deduction

2_An increase in the minimum guaranteed amount of the employment income deduction

3_The introduction of the Special Deduction for Specified Relatives

4_Relaxation of income requirements for dependent deductions and related items

◇ 1_Increase in the basic income tax deduction

The basic deduction is an income deduction that subtracts a fixed amount from taxable income when calculating income tax and resident tax, based on the principle that income necessary for basic living expenses should not be taxed.

Under this revision, for taxpayers whose total income is ¥23.5 million or less (or ¥25.45 million or less if their income consists solely of salary), the basic deduction for income tax has been increased. (The basic deduction for resident tax remains unchanged.)

In the Reiwa 7 (2025) year-end tax adjustment, the annual tax amount is recalculated based on the revised basic deduction, and then reconciled with the amount of tax that has been withheld from salaries under the pre-revision withholding tax tables. If too much income tax has been withheld, the excess will be refunded when salaries are paid in December or in January of the following year.

◇ 2_Increase in the minimum guaranteed amount of the employment income deduction

The employment income deduction is a deduction that subtracts a fixed amount—based on income—from salary income as deemed expenses for wage earners, such as company employees, public servants, and part-time or temporary workers.

Under this revision, the minimum guaranteed amount has been increased from ¥550,000 to ¥650,000.

This increase relaxes the income requirements for relatives or spouses with salary income to qualify for dependent deductions and other related tax benefits.

For example, until the 2024 tax year, a relative eligible for the dependent deduction (a dependent relative) had to have a total income of ¥480,000 or less. If their income was solely from salary, this meant an annual income of ¥1.03 million or less (¥480,000 + employment income deduction of ¥550,000 = ¥1,030,000). This threshold is what has traditionally been called the “¥1.03 million wall.”

Under the new revision, the total income limit for a dependent relative has been raised from ¥480,000 to ¥580,000. Consequently, if a relative earns only salary, they can now have an annual income of ¥1.23 million or less (¥580,000 + employment income deduction of ¥650,000 = ¥1,230,000) and still qualify as a dependent, making them eligible for the deduction.

For instance, if a relative living in the same household (whose living expenses are shared) earns ¥1.2 million from salary, they would not have qualified for the dependent deduction under 2024 rules because their income exceeded ¥1.03 million. Starting in 2025, however, they meet the new threshold of ¥1.23 million and will become eligible for the dependent deduction.

◇ 3_Introduction of the Special Deduction for Specified Relatives

The Special Deduction for Specified Relatives is a new system introduced in this revision, primarily aimed at encouraging university students to work without losing tax benefits for their parents.

Under this system, even if a relative aged 19 to under 23 (such as a university student child) earns income that exceeds the limit for the regular dependent deduction, the deduction for the parent does not immediately drop to zero. Instead, the parent can continue to claim a partial deduction up to a certain amount.

A specified relative is a family member aged 19 to under 23 (as of December 31 of that year) who shares the same household and financial support as the taxpayer, and whose annual total income is over ¥580,000 and up to ¥1.23 million (or, if their income is only from salary, over ¥1.23 million and up to ¥1.88 million). (This includes foster children, but excludes spouses and persons receiving wages as a blue return business employee or white return business employee.)

The deduction amount is the same as the dependent deduction for a specified dependent for total income of ¥850,000 or less (or ¥1.5 million or less if salary only), and is gradually reduced for income above that up to ¥1.23 million (or ¥1.88 million if salary only).

For taxpayers with relatives (such as university student children) who work beyond the income requirements for the dependent deduction, if the relative’s total income is ¥1.23 million or less (or ¥1.88 million or less if salary only), they will be newly eligible for the deduction starting in 2025.

To apply the Special Deduction for Specified Relatives, it is necessary to submit a “Special Deduction for Specified Relatives Declaration Form” to your employer, including the name, date of birth, My Number, estimated income for the year, and the amount of the special deduction for the specified relative.

Since the deduction amount varies depending on the income of the specified relative, parents with children in the university-age range must track their children’s income more accurately than before.

◇ 4_Relaxation of income requirements for dependent deductions and related items

Along with the revision of the basic deduction, the income requirements for relatives or spouses eligible for dependent deductions and similar tax benefits have been relaxed.

Under this revision, the income requirements to qualify for deductions are each raised by ¥100,000. For those with salary income, combining this with the increase in the minimum guaranteed amount of the employment income deduction, the total increase in the income threshold is ¥200,000.

To Claim Deductions, You Must Declare Them Yourself. Key Points to Avoid Missing Out, Including the Newly Introduced Special Deduction for Specified Relatives

To receive deductions through the year-end tax adjustment, you must submit the necessary information to your employer yourself. Because the 2025 tax reform introduces new cases eligible for deductions, be sure to carefully check the changes to avoid forgetting to declare anything.

◇Documents Required for Year-End Tax Adjustment

The following two (A and B) or three (A, B, and C *if there were any changes in dependents during the year) must be submitted by all taxpayers for the year-end adjustment for the year Reiwa 2025.

(A) “Application for Basic Deduction for Salaried Workers, Application for Spousal Deduction for Salaried Workers, Application for Special Deduction for Specified Relatives of Salaried Workers, and Application for Deduction for Adjustment of Income” for the year 2025

(B) “Application for (Change in) Exemption for Dependents for employment income earner” for the year 2026

(C) “Application for (Change in) Exemption for Dependents for employment income earner” for Reiwa 2025 ( *Already submitted; revise and resubmit as necessary )

Under this revision, the income requirements for dependent deductions and related items have been relaxed. As a result, if the number of dependents increases or new relatives become eligible for deductions, you must update and resubmit the Reiwa 7 (2025) “Declaration of Dependent Deduction, etc. for Salary Earners (Changes)” (hereinafter, “Dependent Deduction Declaration”).

The “Declaration of Special Deduction for Specified Relatives for Salary Earners” (hereinafter, “Special Deduction Declaration”) is a newly introduced form added to this year’s year-end tax adjustment due to the creation of the Special Deduction for Specified Relatives.

Additionally, due to the increase in the basic deduction, the “Declaration of Basic Deduction for Salary Earners”(hereinafter, “Basic Deduction Declaration”) has also been partially revised.

【Checklist ①】 Dependents Now Eligible Up to ¥1.23 Million! Quickly Confirm Who Has Become Eligible for Deductions Under This Revision

Thanks to the relaxation of income requirements and the introduction of new deductions, the scope of eligible dependents has expanded. Use this checklist to verify if anyone in your household has newly become eligible and ensure that all applicable deductions are properly declared.

Key Points When Preparing Declaration Forms

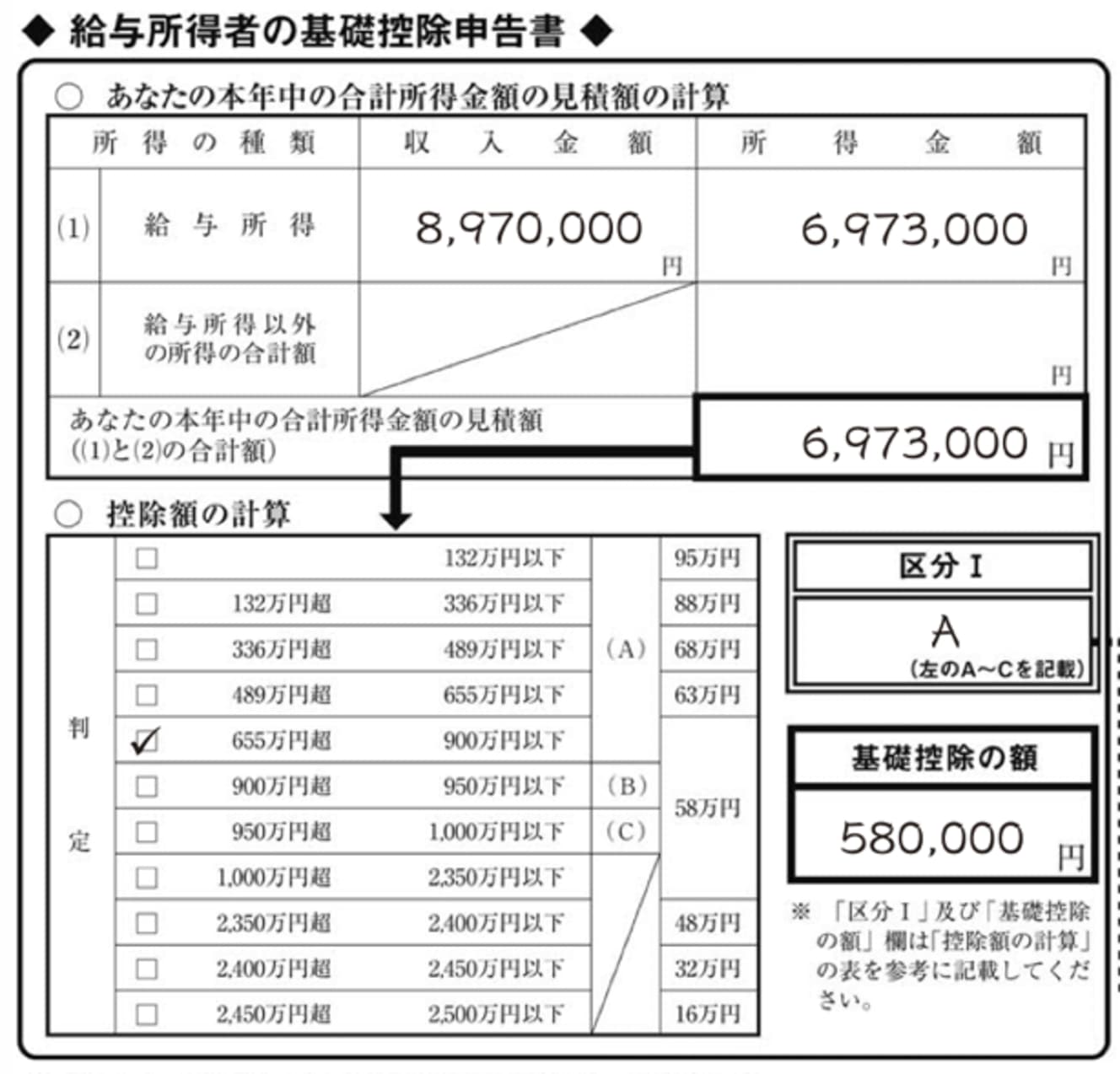

◇Estimating Income

The documents for the year-end tax adjustment must be submitted before receiving the December salary. Therefore, the income amount to be entered (total estimated income) is not the final confirmed amount, but a projection (estimate). Many people find it confusing how to fill in this section, so it’s important to understand it correctly.

To estimate salary income, first calculate the total gross pay received from January up to the time of submission, then add the projected salary and bonuses expected to be received for the remainder of the year. This gives the total income from salary. For the projected portion, you can reference last year’s withholding statement or your most recent pay slips, taking into account this year’s circumstances to arrive at an approximate figure.

The total gross pay is the amount before deductions for taxes and social insurance premiums, listed on pay slips or withholding statements as the payment amount. It includes overtime pay, family allowances, dependent allowances, housing allowances, and qualification allowances, but excludes non-taxable commuting allowances (transportation costs). If you receive income from multiple employers, sum all sources to determine your total salary income.

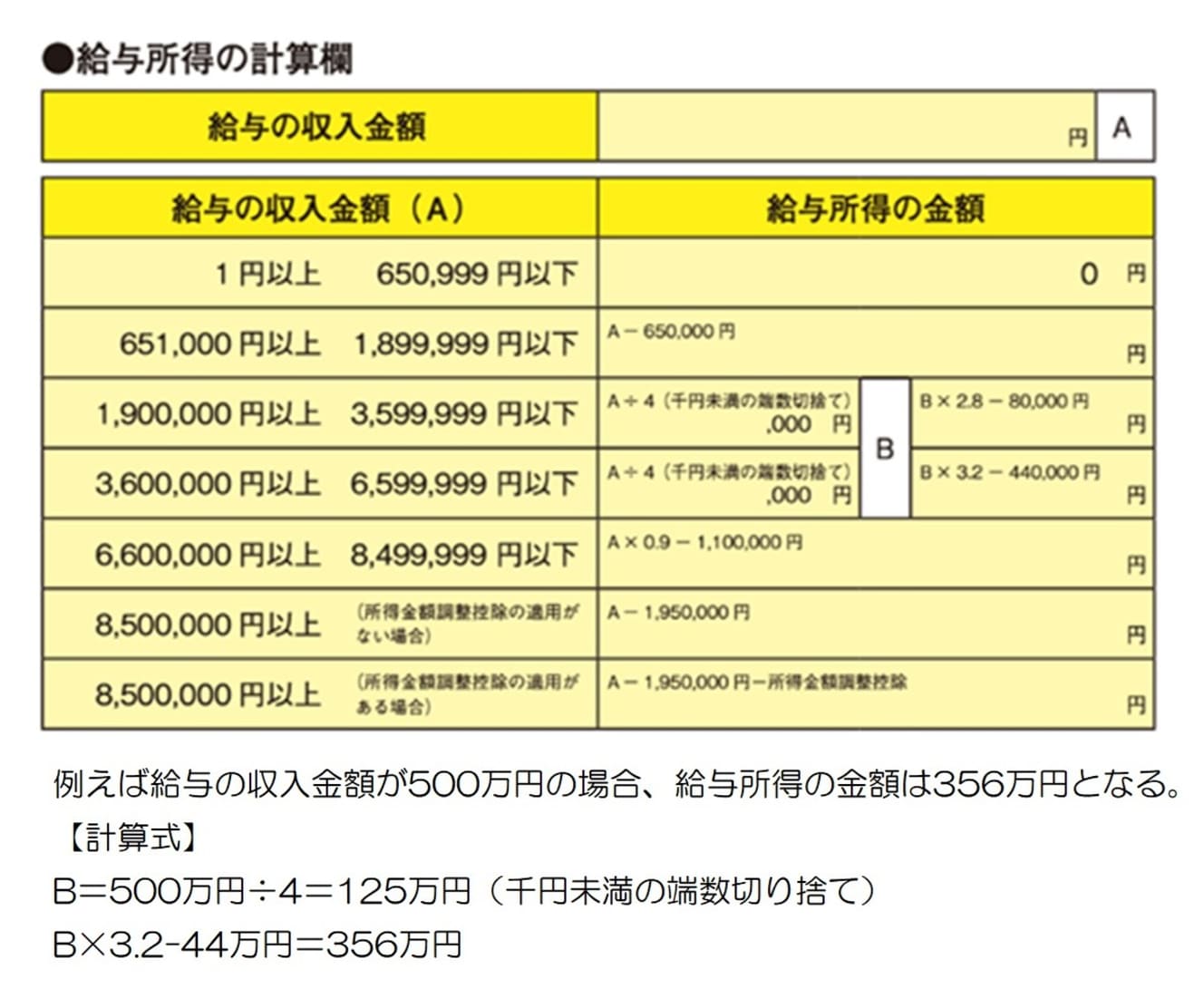

Once you have calculated the total salary income, apply it to the salary income calculation table to determine the amount of employment income.

If you have income other than salary, add the total amount of that income (income minus expenses) to the employment income. The resulting sum is your estimated total income, which should be entered on the form.

【Checklist ②】 No More Tedious Writing!? Conditions for Using the Simplified Declaration Starting in This Year’s Year-End Adjustment

For the Reiwa 7 (2025) year-end tax adjustment, employees must submit the Reiwa 8 (2026) Declaration of Dependent Deduction, etc., which is required for next year’s withholding.

For declarations submitted from January 1, 2025, if there are no changes from the information provided in the dependent deduction declaration submitted to the same employer last year, it is possible to submit a simplified declaration.

When submitting a simplified declaration, you only need to enter the taxpayer’s name, My Number, and address/residence, and note in the blank space that there are no changes (e.g., no changes from last year). If the declaration form is compatible with the simplified process, simply check the box indicating no changes from last year’s declaration in the relevant section.

If none of the following conditions apply, submission of a simplified declaration is permitted under the instructions of your employer.

In principle, the simplified declaration can only be used when there are no changes at all in the information provided. However, changes in the estimated income are allowed as long as they remain within the range where the dependent status does not change.

For example, if a child’s estimated income is ¥400,000 in 2025 and ¥500,000 in 2026, both amounts fall within the income requirement for a dependent (¥580,000 or less), so the simplified declaration can be used if there are no other changes.

Year-end tax adjustments may seem troublesome, but they are less cumbersome than filing your own tax return. To ensure you receive all applicable deductions, be sure to understand which deductions apply to you and their requirements.

Interview and text by: Hiroki Takekuni

Financial planner and representative of Rapport Consulting Office. After graduating from Nagoya University's Faculty of Engineering, he worked for a securities company and an insurance agency before setting up his own business. He is a first-class financial planning technician, CFP®, certified real estate transaction specialist, and sauna and spa professional.