Politician Arrested for Tax Evasion and Kickbacks Reveals Unthinkable Practices

A Balance Sheet Full of Unknowns an Incident “Where Everyone Should Be Arrested”

In the midst of the tax filing period, while #TaxReturnBoycott trends on social media, the catchphrase “Tax evasion is a crime” prominently displayed on posters by the National Tax Agency is stirring up taxpayer resentment.

“It’s ridiculous to file tax returns. I think they should pay their taxes properly before telling us to ‘pay up,'” expressed Koizumi Kyoko, echoing the sentiments of many.

The backdoor money scandal surrounding political fundraising parties organized by the LDP faction has triggered outrage. During the news23 program (TBS), where the House of Representatives Ethics Committee (Seirinshin) met, tax accountant Hiroaki Urauno, well-versed in political funds, made this damning statement:

“It’s unimaginable if we think about it from the perspective of a regular company. It’s the kind of event where everyone should be arrested.”

Last month, the National Federation of Chamber of Commerce and Industry requested the National Tax Agency to conduct a tax investigation into a total of 85 Diet members and branch managers of the Abe and Nikai factions, who were found to have failed to include their names on their political fund balance sheets. We asked Mr. Urano, a licensed tax accountant, if this case of back taxes constitutes tax evasion.

“This is egregious tax evasion. Of course, everyone is subject to arrest.

So, specifically, what kind of tax evasion is this? One aspect is corporate tax evasion.

Political funding parties are typically organized by political entities. Among these, political parties are classified as public-interest corporations, while factions and various political organizations are categorized as non-legal personality corporations, etc. Corporations engaged in revenue-generating activities are subject to corporate tax.”

In principle, political funds of political organizations are exempt from taxation, provided that they are used for political activities.

“Although they are advertised as political fundraising parties, the reality is that they are events with profit margins of 80% or even 90%. In other words, they conduct business under the guise of political activities, falling under the category of entertainment business among revenue-generating activities as defined by the Corporate Tax Law.

For corporate income, three taxes are imposed: national corporate tax, local corporate inhabitant tax, and corporate enterprise tax. Additionally, in cases of tax evasion like this one, additional taxes for underreporting are imposed. This functions as a penalty for concealing facts or intentionally misrepresenting reported information.”

Furthermore, late payment penalties are imposed for failing to pay taxes by the designated deadline.

“In cases of tax evasion, taxation is retroactive for up to seven years.

While corporate taxes are calculated annually for each business year, the combined total of the three taxes imposed on income is roughly 30%. This constitutes the original tax amount, with the additional tax for underreporting being 40% of this base tax. Late payment penalties, which were previously around 14.5% starting from the day after the payment deadline until two months later, are now about 10%. When considering the retroactive period of seven years, the late payment penalty alone can result in a significant amount.

This means that approximately 50% to 60% of the funds allocated by the political organization for the party will be subject to additional tax.”

For violations of the Political Funds Control Law (false entries), the accounting officers of both the Abe faction and the Nikai faction have already been indicted for failure to report some of the party’s income in the political funds income and expenditure reports.

“All the former secretaries-general who attended the Political Ethics Examination Committee (Political Ethics Committee) meetings claimed they were not involved in the accounting, stating that it was the responsibility of the accounting officers. However, the accounting officers are merely nominal figures in terms of their official duties. The actual organizers of the political organizations are the ones to whom the revenue belongs. Ideally, it would be the faction leaders, so if it’s the Nikai faction, it would be Chairman Toshihiro Nikai, and in the case of the Abe faction, it would be the secretary-general who should take responsibility.”

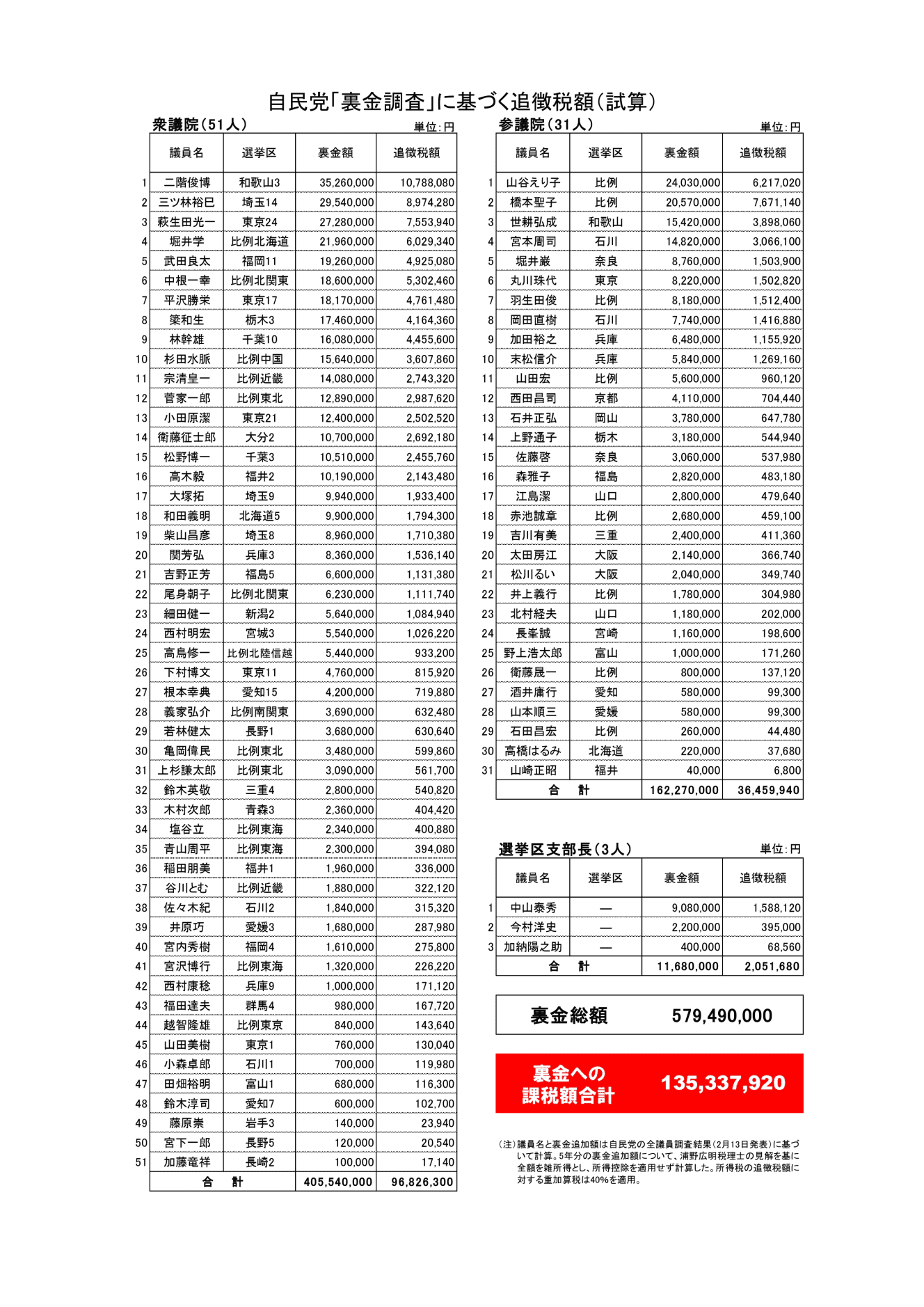

The taxable amount on the slush fund for the 85 lawmakers whose names were not listed is approximately ¥135 million.

It is not only corporate tax that constitutes tax evasion. Naturally, income tax is also a target.

“Any illicit funds are fully taxable as miscellaneous income. Miscellaneous income is calculated by subtracting necessary expenses from the income amount. For example, let’s say a salaryman receives a manuscript fee. If they buy reference books to write that manuscript, those expenses count as necessary expenses. However, politicians receive their salaries, and in this case, they pocketed kickbacks completely, so there are no necessary expenses. Income tax and resident tax are imposed on the full amount received as kickbacks.

In this scenario, the tax amount would be approximately 30% of the income when combining income tax and resident tax. Additionally, just like corporate tax, surtax and delinquency taxes are imposed, so the additional tax would amount to at least 50 to 60% of the kickback amount.

The National Confederation of Chambers of Commerce and Industry of Japan has estimated the tax amount if 85 individuals who were not reported in the political funds income and expenditure reports from 2018 to 2022 were subject to additional taxation, based on the analysis by Tax Accountant Urayoshi. According to the estimation, the total amount of hidden funds is approximately 579.49 million yen, and the taxable amount for the illicit funds amounts to about 135 million yen. Among them, the largest amount of additional tax is for former Secretary-General Nikai, exceeding 10 million yen. Hagiuda Koichi, former chairman of the Abe faction who was the only one of the five members of the Abe faction not to attend the House of Representatives Political Ethics Committee, has an additional tax of over 7.5 million yen.”

“This time, it hasn’t been scrutinized much, but consumption tax is also imposed. Since they’re essentially profiting from an entertainment business, they become taxpayers for consumption tax.”

For small-scale business owners and individual proprietors forced to pay consumption tax through the invoice system, filing tax returns may seem ridiculous.

Over the past five years, Mr. Hagita received a total of 27.28 million yen in kickbacks, yet even after amending his financial statements, he still listed entries such as “purpose of expenditure” and “amount” as “unknown.” What happens when an individual business owner submits a profit and loss statement or an income and expenditure breakdown full of unknown entries?

“The tax office is unlikely to approve it. If we submit with ‘unknown’ entries, we’ll be subject to additional taxes.”

If there are discrepancies in the tax return forms, citizens are investigated. Politicians, on the other hand, receive substantial kickbacks, make dubious entries in their financial reports, and still manage to avoid paying taxes.

Tax evasion by deception is punishable by imprisonment for not more than 10 years or a fine of not more than 10 million yen.

“It has long been said that the tax administration discourages the weak and helps the strong, and this is true. Even if the tax return of a small business is different by 10,000 yen, the tax office will strictly pursue the business.

For example, a freelance sole proprietor may receive a call from the tax office saying, ‘Please come to the tax office to learn about the details of your tax return. Most probably, most people will comply seriously. But such a request has no basis in law and should be left alone.

The tax office is essentially required to collect taxes based on the law. And citizens are supposed to pay taxes based on the law. So if you are investigated by the tax office and asked to pay additional taxes, it is important to ascertain the basis on which you have to pay additional taxes based on which law. The tax office often gives up when asked about the basis for the tax. The tax office employees are the least knowledgeable about tax law. They are not accustomed to using the Constitution as a tool.”

On the other hand, there is a reason why the tax administration “helps the strong,” in other words, it is lenient with politicians.

“The reason why they leave politicians alone is because the business world and the Ministry of Finance make the tax laws. Most of the tax laws are favorable to large corporations.

Once a Japanese tax law is submitted to the Diet, it takes about three weeks to pass the House of Representatives. The tax administration’s stance is that since it is the members of the ruling Liberal Democratic Party who will vote in favor of the law in the Diet, they should be left alone without pursuing the issue of taxation.”

The public is angry that lawmakers who have obtained slush funds are evading paying taxes. If this constitutes tax evasion, they should be charged with a crime.

“If the tax evasion was done by deception, it is a violation of the Income Tax Law, the Corporation Tax Law, and the Consumption Tax Law, and is punishable by up to 10 years in prison or a fine of up to 10 million yen. In addition, you must pay the additional tax amount. He should serve the imprisonment and also resign from the Diet.

If it is tax evasion, the National Tax Agency is obligated to file a complaint with the public prosecutor. Upon receiving the accusation, the public prosecutor will conduct an investigation and make a case. However, since tax evasion is a crime, the prosecutors can conduct their own investigation without waiting for the IRS to file charges if it is true.

It is strange to think that the legislators who are raking in the money in this slush fund case are not being charged with any crime. How to change this is certainly the challenge we have been given.”

“I won’t vote in the next election.” Now, such voices are being raised on social networking sites. Perhaps that is a good place to start.

Hiroaki Urano, a tax accountant and special researcher at Rissho University Institute of Legal Studies. Born in Hokkaido in 1940. From 2002 to 2011, he was a professor at the Faculty of Law and the Graduate School of Law at Rissho University. From 2011 to 2021, he was a visiting professor at the Faculty of Law at the same university. His books include “Facing Tax Audits with Dignity” (Nihon Hyoronsha), “Inequality and Poverty Expanded by Taxes” (Akebi Shobo), and “Challenges of Democratic Taxation” (Gakushu no Tomosha), among others.

Interview and text by Sayuri Saito: Sayuri Saito