Insights from Aggressive Investment Strategies on New NISA Savings Surpassing 60,000 Yen Monthly

The most common answer was “90,000-100,000 yen” at 36.5%!

The new NISA, launched in January after a review of the tax incentive system, has been touted by some as a boost to asset building, but is interest in investing growing?

400F, which operates the household financial diagnosis and consultation service “Okaneko,” conducted a survey of 1,594 users nationwide from January 4 to 7, the first day of the new year, on their intention to use the new NISA. The results showed that 86.6% were aware of the new NISA and 37.8% used it.

So, for what purpose do Okaneko users use the New NISA? When asked in multiple answers, 69.9% said “to increase surplus funds,” followed by “to save for retirement” at 63.5%, and “to save for education and childcare” at 13.3%.

Izumi Oishi, a financial planner, analyzed the results as follows.

The most common answer is to increase surplus funds, but it may be that they have a surplus in their monthly balance and it would be a waste to leave it in a savings account for life, so they accumulate and invest it in the NISA.

For example, if you are both working, it is unlikely that your household income will immediately drop to zero if something happens to one of you. If you have an emergency reserve fund of 1 to 1.8 million yen, equivalent to three to six months of living expenses, and you think that you can manage your immediate living expenses in case of emergency, it makes sense to put the monthly surplus into the NISA’s savings account.

Under the new NISA, the maximum amount of investment is limited to 1.2 million yen per year for the “savings investment limit” and 2.4 million yen per year for the “growth investment limit,” for a total of 3.6 million yen that can be invested in financial products tax-free.

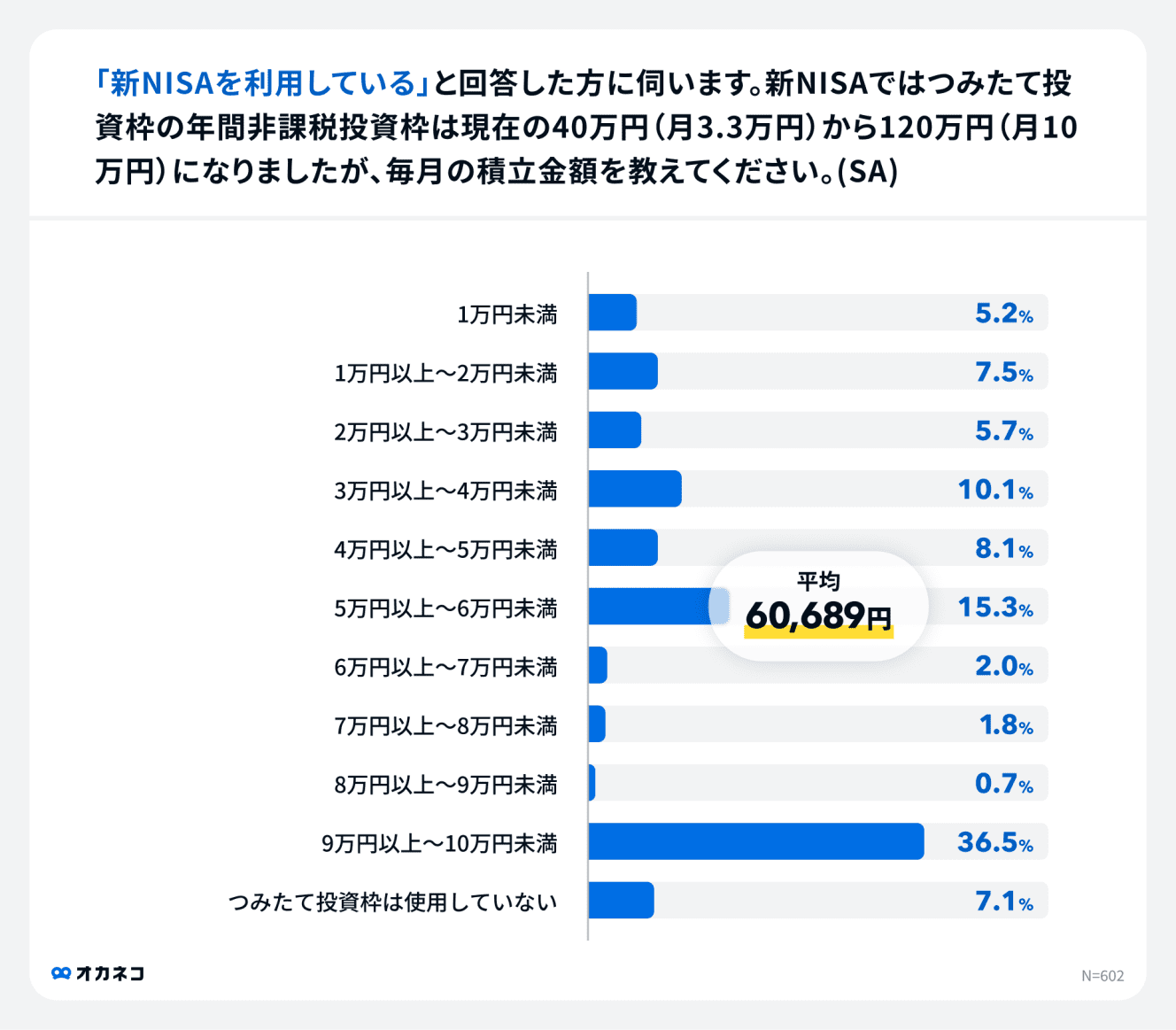

The monthly savings amount of 36.5% of Okaneko users is “90,000-100,000 yen or less. The average monthly savings amount was 60,689 yen, followed by “50,000-60,000 yen” at 15.3% and “30,000-40,000 yen” at 10.1%.

The average monthly savings amount was 60,689 yen. “If you accumulate 60,000 yen every month, for example, your monthly take-home pay is 300,000 yen, and your expenses are kept at 240,000 yen, so your income and expenses would be 60,000 yen.

If you can always maintain a surplus of 60,000 yen or more, even if prices are on the rise or you have extraordinary expenses, it may be possible to accumulate 60,000 yen every month.

Incidentally, 28.2% of respondents had household incomes of “less than 4 million yen,” the highest percentage. 19.1% of the respondents had an annual income of “4 to 6 million yen,” 16.6% had an annual income of “6 to 8 million yen,” 10.5% had an annual income of “8 to 10 million yen,” and 15.6% had an annual income of “10 million yen or more. So there are people with annual incomes of less than 4 million yen who deposit a monthly surplus of 50,000 to 60,000 yen into their NISA accounts.

Well, I wonder if there are people who cut down their living expenses and put their money into NISA. I think it is OK to invest surplus funds in NISA. If you have never accumulated funds before, you might try to live by investing them to the fullest, and then reduce the amount to determine the appropriate price. The ironclad rule is to invest with surplus funds, so don’t overdo it. It is important to understand your income and expenditure.

20 million yen is not enough” for retirement funds…

In 1919, based on a report by the Market Working Group of the Financial System Council of the Financial Services Agency, the mass media reported that “20 million yen will be insufficient for retirement,” and this became a hot topic. However, after 2010, amid rising prices, some people are saying that “20 million yen is not enough for retirement”. The fact that many respondents answered “to save for retirement” as the purpose of using the new NISA may be an indication of their distrust of the public pension system.

He continued, ” Currently, due to macroeconomic indexing adjustments, even if wages and prices rise, the pension amount will not rise as much as the rise in prices. I think that inflation has continued to rise for the past year or two, and people are becoming anxious about doing nothing for their retirement.

According to the aforementioned FSA report, the monthly deficit for an elderly couple in an unemployed household is approximately 50,000 yen. Assuming that retirement is 30 years from the age of 65, the estimate is that the amount needed to prepare on one’s own is 18 million yen. People who are conscious about money say, ‘If prices continue to rise as they are now, 50,000 yen will not be enough. I don ‘t think it is surprising that people who are money-conscious would think, ‘If prices continue to rise as they are now, 50,000 yen will not be enough, and 20 million yen will not be enough for the retirement funds I will need when I am old enough.

Looking at household financial assets in the “Japan-U.S.-Europe Comparison of Flow of Funds (as of March 31, 2011)” released by the Bank of Japan in August ’23, cash and deposits account for 54.2% in Japan, while stocks and investment trusts account for 15.4%. In contrast, in the U.S., cash and deposits account for 12.6%, while stocks and mutual funds account for 51.3%. The Japanese still seem to have a strong tendency to save rather than invest, but what is Mr. Oishi’s view?

From the high economic growth period of the 1960s to the bubble period of the early 1990s, interest rates on savings accounts were sometimes as high as 5-6%. I think the current generation in their 80s and 90s must have worked hard to save money back then.

What about Generation Z? They entered the workforce at a time when stock prices were rising due to Abenomics. Looking at the world, the U.S. stock market was rising even more. They entered the workforce at such a time, they are highly IT literate, are familiar with overseas information, and probably think that the time has come for money to grow rather than be saved.

Nowadays, people can open brokerage accounts online or with their smartphones, and I think the hurdles to investment have been lowered, which is also encouraging younger people to practice it,” he said.

Generation Z is also efficiency-conscious when it comes to asset building.

According to the results of the “Financial Literacy Survey” conducted by the Central Council for Financial Services and Public Information in 2010, 7.1% of respondents answered that they “had opportunities to receive financial education at schools, universities, and workplaces, and did so. 75.7% responded that they “did not have the opportunity to receive it.”

The results show how inadequate financial education is in Japan, where financial and economic education has finally been made compulsory in high school home economics classes since 2010.

The government launched the Organization for Promotion of Financial and Economic Education in April, and is trying to enhance financial and economic education by dispatching advisors certified by the organization to companies and schools to give lectures and provide individual consultations.

In a survey of Generation Z college students, the most common response to the question, “When choosing a company or workplace, what kind of training would you like to see provided?

Generation Z is said to be particularly conscious of time performance, and asset formation may be one of the things they want to do efficiently.

If they want to grow the same amount of money, they should invest it efficiently. For that reason, they want to acquire financial knowledge. If this can be achieved in the workplace, that would be great–I would be very happy if the consciousness of the younger generation is changing in this way.

Izumi O ishi, CFPⓇ , Senior Financial Planner certified by the Japan FP Association (NPO). She is a career consultant. After graduating from university, she joined Recruit Co. Ltd. for about 15 years before establishing her own FP firm in 2001. He has been giving lectures and training courses on economic education, career design, and asset building using familiar newspapers at universities and companies. For individuals, he provides objective financial and life planning services.

Interview and text: Sayuri Saito