The New NISA “Wasn’t Supposed to Happen! …The “investment insanity” trap perpetuated by the heated NISA press

Simulation is a “picture-perfect”

The “New NISA” will start in January ’24. Every day, news and articles related to NISA are distributed on the Internet. However, some of them are so eager to emphasize the benefits of NISA that they deceive individuals. Moreover, the guidebook of the Financial Services Agency (FSA) is also proudly mentioning it. What is the problem? Let us clarify the reality.

Excessive appeal of NISA is going too far

The media coverage of NISA (National Institute for Savings and Investment Promotion) has become heated, as the name implies, a government program that allows individuals to pay zero tax (tax rate of approximately 20%) on their investment gains. This alone is a sufficient merit, and the new NISA will also greatly expand the tax-exempt investment limit and make the tax-free investment period indefinite. There is no doubt that this is an epoch-making system that will revolutionize individual asset management.

However, in an effort to promote the benefits of this system, explanations that are misleading or, to put it bluntly, “lies” are rampant. If people believe such explanations, it is possible that many people, especially those who started investing with NISA, will later find themselves thinking, “This is not what I thought it would be! If you believe them, there is a possibility that many people, especially those who started investing with NISA, will later find themselves thinking, “This was not supposed to happen!

Do not be fooled by “asset management simulations.

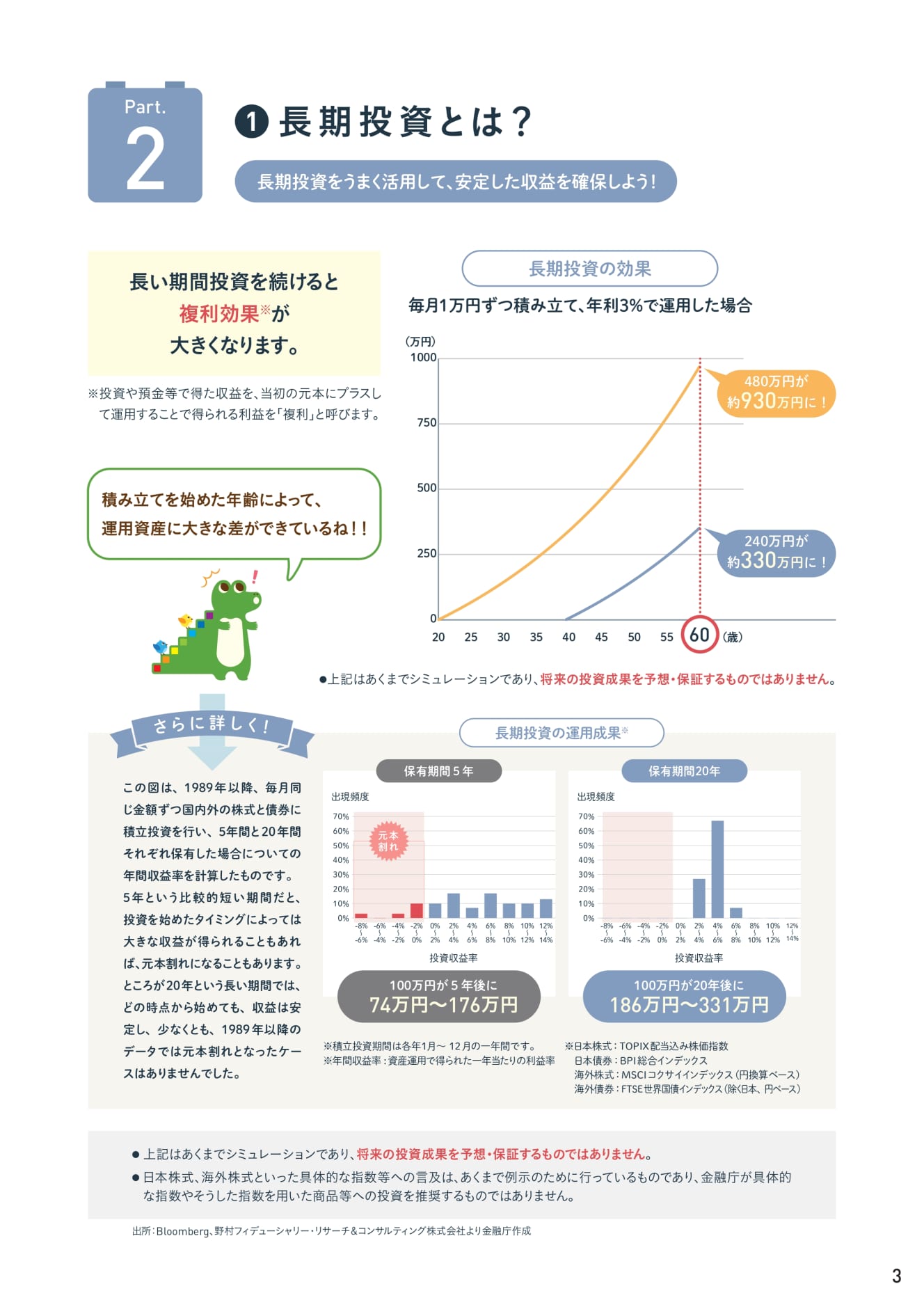

The problem is the simulation of asset management in NISA. The most common pattern is “if you accumulate and invest X amount of money every month and invest it at X% interest rate per year,” and the profit after 20 or 30 years is estimated. For example, the latest edition of the Financial Services Agency’s “Let’s Start! NISA Quick Guidebook” (the latest edition) shows a simulation of the effect of long-term investment: if 10,000 yen is set aside every month and invested at an annual interest rate of 3%, 2.4 million yen will become 3.3 million yen over 20 years, and 4.8 million yen will become 9.3 million yen over 40 years. The FSA states that the annual interest rate is 3%.

The FSA uses a conservative figure of 3% per annum for the interest rate, but other articles often set the interest rate at 5% per annum, and the article is full of such statements as “your retirement will be secure” if you invest the money for 20 or 30 years. Indeed, if one were to accumulate 30,000 yen per month and invest it for 30 years at an annual interest rate of 5%, 10.8 million yen would become approximately 25 million yen.

What is the problem with such simulations? Simulations of this kind are always based on “compound interest. The term “compound interest” is used in the sense of “investment of profits earned from investments in addition to the principal amount,” and it is assumed that profits from investments are re-invested, and as a result, profits generate new profits, and profits keep growing.

Those who do not question these simulations and explanations are in trouble. They are unaware that the term “compound interest” is being used incorrectly.

Compound interest” is irrelevant to investment.

To begin with, compound interest is a method of calculating interest rates or interest. When money is deposited or borrowed, interest accrues on the principal, but with compound interest, interest is incorporated into the principal, and the next interest accrues on the principal that incorporates the interest. Simply put, compound interest is “interest on interest. When interest is not incorporated into the principal, it is called “simple interest. With simple interest, interest does not accrue on interest.

Basically, both compound interest and simple interest are terms used for savings and loans. Bank time deposits can be compounded or simple interest, and a typical mortgage loan is compounded. The reason mortgage balances do not decrease easily is that interest is added to interest.

When calculating interest on financial instruments with compounded or simple interest, there are certain conditions that are assumed. First, the principal must be guaranteed. Second, a predetermined amount of interest must accrue steadily for a certain period of time. Without these conditions, both compound and simple interest calculations are meaningless. Time deposits and mortgages fall under these conditions.

Therefore, compound interest has nothing to do with stocks and mutual funds, which are the investment targets of NISA. This is because there is no guarantee of principal and no pre-determined interest. In other words, the aforementioned simulations are completely meaningless.

The mockery of the expression “compounding effect.”

Some may say, “It is just a simulation, so there is no need to get so worked up about it. However, a series of simulations cannot be dismissed as “theoretical. I sense an “intention” to mislead individuals.

The use of the word “compound interest,” which is used in interest calculations for time deposits and the like, seems to be an attempt to create an image that “investing with NISA will make you more money” than it really is.

There is a reason for such an illusory assumption. In many cases, when explaining asset management simulations, the expression “compound interest effect” is used instead of “compound interest” to refer to “reinvesting profits earned from investments to earn further profits. Probably, since it is an obvious mistake to say “compound interest,” the meaning is made ambiguous so that it can be interpreted as “compound interest effect” = “compound interest-like effect” so that it can be excused later.

Since it is assumed that the FSA understands the true meaning of the term, it is more “malicious” to use a phrase that misleads individuals than to use a phrase that they know nothing about.

FSA’s interpretation of “compound interest” is completely out of line.

Let’s return to reality since the conversation has become abstract. In the aforementioned FSA guidebook, there is a sub-heading that reads, “The longer you continue to invest for a longer period of time, the greater the compound interest effect. Then, as a note to the “compound interest effect,” it adds, “*The profit obtained by adding the earnings from investments, deposits, etc., to the initial principal is called ‘compound interest. This is completely out of line.

In fact, prior to this guidebook, the FSA had published an older version called “TOMOTATE NISA Quick Reference Guidebook. In the guidebook, the FSA explained that “if you continue to invest your money without receiving distributions, you can expect to see an amplification effect (compound interest effect) as the profits earned from the investment are further invested. The longer the investment period, the greater the compounding effect,” he explained modestly. This is an expression that leaves room for excuses.

In other words, in anticipation of the new NISA, the FSA has “endorsed” the interpretation that “reinvesting profits earned from investments to earn additional profits” is “compound interest” and the “compound interest effect. (It can be said that the “interest” in compound interest has somehow come to be confused with the “interest” on investment profits, instead of the original “interest” on interest or interest rates.)

Even Einstein is crying behind the grassy knoll!

The “real damage” has already been done. Individuals’ comments on social networking sites on the Internet are rife with misconceptions, such as “the sooner you fill the investment limit of the new NISA, the greater the compounding effect will be,” or “long-term investment will increase the compounding effect. All of these statements are merely stating the obvious: “Reinvesting profits and increasing the amount invested will increase the likelihood of larger future returns. Had they simply said “reinvestment of profits” instead of using the term compound interest, these misconceptions would not have been so widespread.

In investment simulations, Einstein often appears to emphasize the greatness of compound interest. He is often quoted as saying, “Compound interest is the greatest invention of mankind,” but the truth is unknown. Perhaps he never said it, or it was a light-hearted remark (Dr. Einstein was also a bit of a failure to see it). At least during Einstein’s lifetime, there were no index funds. That fact alone shows that seeking compounding effects in mutual funds and stocks is a mistake.

Preparing for Risk is Necessary to Continue Long-Term Investing

Rather than making simulations that are merely wishful thinking, it would be more meaningful to make realistic assumptions, such as “If a 5% loss occurs in the first year, a 5% increase in the second year will not return the principal amount. This is because a preparedness for risk is a “tolerance” in the event of an actual loss.

I have heard from people in the online securities industry that not a few people who attend seminars think that “NISA will give me peace of mind. You will make this much money! It is no wonder that inexperienced investors may be led to believe so by such simulations. There is a possibility that they may stop investing, saying “This is not how it was supposed to be.

As I mentioned at the beginning of this article, the NISA itself is a system created by the government that can be evaluated with open arms. The FSA has done a good job, so there is no need to play tricks on it.

Interview and text: Kenji Matsuoka

After working as a money writer and financial planner/market analyst for a securities company, he became independent in 1996. Writes articles on finance and asset management mainly for business and economic magazines. Author of "A Textbook for the First Year of Robo-Advisor Investing" and "Understanding with Rich Illustrations! Cashless Payments for the Absolute Benefit of Cashless Payments".