One Account per Person Nisa: Megabanks And Local Banks Are Not the Answer!

If you say, “I’ve always taken care of you, so…” you will regret it.

The campaign war among banks and securities companies for the “New NISA” that will start in January 2024 has reached a fever pitch, and procedures for changing from the current NISA account will begin in October. To coincide with this, each company is offering cash, points, gift certificates, etc., in order to attract as many accounts as possible. For those who are considering asset management under the new NISA, we will explain which financial institutions you should choose.

Don’t be fooled by campaigns…you can make up the difference in no time!

The rewards for opening a new NISA (New NISA Small Investment Tax Exemption Scheme) account vary in type, such as cash, points, gift certificates, etc., but in terms of amount, they are concentrated in the 1,000-2,000 yen range. You may think, “Isn’t the best deal the best deal? You may be thinking, “Why don’t I just go with the one that offers the best deal? The difference between the two is negligible, and there are more important things to focus on. Also, as we will discuss later, if a brokerage firm offers a service that rewards points based on the amount invested, even if there is a difference in the amount of the campaign, you can quickly make up the difference.

To sum up first, the best place to open an account for the newNISA is at an online securities company. There are two reasons.

1) The number of “Temporary Deposit NISA Number of “Mutual savings NISA” handled by Net Securities: 170 ~Number of “reserve deposit NISA”: Net Securities: 170 ~ 200 Mega banks and major securities companies: About 10 to 20

First, the number of investment trusts that can be invested in under the NISA is overwhelmingly greater at online securities. The new NISA has a “growth investment line” for investing in stocks and investment trusts, and a “savings investment line” for accumulating investments in investment trusts, and the lineup of investment trusts available for investment differs depending on the financial institution. The same investment targets are available as those in the current NISA, and the lineups of the “reserve investment limit” are already very different among the different institutions.

The “Tatemonate NISA” is limited to investment trusts that meet the requirements set by the Financial Services Agency, and as of September 14, 2023, a total of 240 investment trusts are eligible for the Tatemonate NISA and were covered by this program, of which 170 to 200 were offered by online securities companies, while most megabanks and major securities companies offer only 10 to 20.

Why is there such a large difference in the number of contracts handled? The reason is that some banks and securities firms have lineups that focus on mutual funds managed by their own affiliated investment management firms. Competing mutual funds are excluded. This is a major disadvantage.

There are a number of mutual funds, such as “Nikkei225-linked ” or “S&P500-linked,” that have exactly the same contents but different holding costs (i.e., trust fees ). Therefore, if there are competing products, the one with the lowest trust fee should be chosen, but if there is not a large selection, it is impossible to compare and choose. The larger the selection, the better.

Credit card Point Redemption through credit card payment is too good to be true.

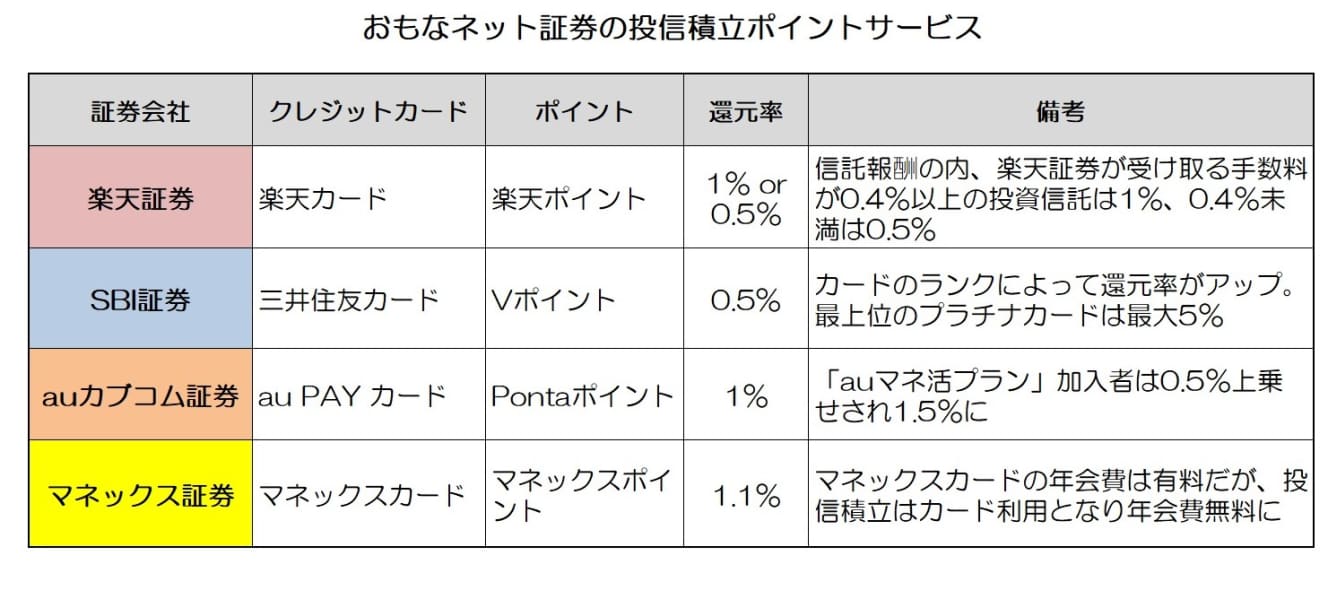

The second reason to choose online securities is that they offer a service that rewards points based on the amount invested. When you purchase financial products with credit cards or electronic money, you get points just like any other purchases. This is, in any case, a great deal.

One of the most advantageous is the point redemption for saving investment in mutual funds. When you pay with a credit card, you receive points according to the amount of money you accumulate each month. For example, if you invest 10,000 yen per month in a savings NISA, you will earn 100 points per month at a 1% rate of return. At 20,000 yen per month, you would earn 2,400 points per year.

Many users are already taking advantage of the current system under the existing “Tatemono” NISA, and the new NISA is likely to make it even more popular. Below is a summary of the types of points that can be earned and the rate of return for each online securities.

PayPay Securities also start offering point redemption.

Although not listed in the table, PayPay Securities launched a service in September offering 0.5% PayPay points when investing in mutual fund savings accounts. The effect is essentially the same as the redemption of points from credit card transactions, and naturally, the company is looking to attract users under the new NISA.

The financial division of the SoftBank Group is set to lose LINE Securities, and PayPay Securities is gaining more weight within the group. It is possible that further campaigns will be launched in the future. Those who normally live in the “SoftBank-PayPay economic zone” may want to consider it. However, please note that the lineup of mutual funds for the reserve account is still smaller than that of other online securities, and the overall strength of the company is not as good as that of other online securities.

The battle over the maximum amount of 100,000 yen that can be redeemed for points from credit card transactions

Finally, let us look at what to watch for in the future. The credit card point redemption services of various companies are capped at 50,000 yen per month, and no points are awarded for amounts spent in excess of 50,000 yen. The current system allows for an annual investment limit of 400,000 yen, or 33,333 yen per month, so the credit card transaction limit of 50,000 yen was not a major problem.

However, the new NISA’s annual limit on the freshly-minted investment limit will be increased to 1.2 million yen. Therefore, up to 100,000 yen can be accumulated per month. In other words, the new NISA’s “Growth Advance” does not allow for full point redemption.

The only exception to this is Rakuten Securities, which has a limit of 50,000 yen for point redemption through “Rakuten Cash” electronic money payment, in addition to credit card payment. When combined with Rakuten Card payments, a total of 100,000 yen is eligible for point redemption (the redemption rate for Rakuten Cash is 0.5%).

However, there is a new trend: tsumikiSecurities, a Marui Group company, will raise themaximum amount of points redeemable for credit card transactions to 100,000 yen per month starting in January2012. It will be very interesting to see if other companies follow suit. The law originally set the limit at 100,000 yen per month, so there should probably be no problem (exception to Article 148 of the Cabinet Office Ordinance).

Interview and text: Kenji Matsuoka

After working as a money writer and financial planner/market analyst for a securities company, Matsuoka became independent in 1996. He writes articles on finance and asset management mainly for business and economic magazines. Author of "A Textbook for the First Year of Robo-Advisor Investing" and "Understanding with Rich Illustrations! The Book of Absolute Benefit from Cashless Payments".