NISA’s Strongest Poyage! The Power of “Credit Card Savings” Over Mobile Phone Charges

Revisions and Megabank Alliances…What are the Promising “Common Points” for the Future?

The “deterioration” of point services continues unabated. This year, the redemption rates of well-known common points such as Rakuten points, d-payment, and Ponta have continued to deteriorate. On the other hand, a number of collaborations with megabank financial groups, such as the merger of T Point and V Point, have emerged. Until now, the theory has been to use mobile carrier-centered points, but is there a blind spot there? What is the most profitable “credit card savings plan” today? This report summarizes the trends in the industry, which has once again entered a period of upheaval, and explores the points that hold promise for the future.

The “V-Point” shock has changed the point power structure.

Common points are points that can be used for payment at multiple stores operated by different companies. Perhaps many people still think of T-points, Ponta, Rakuten points, and d-points as the four major common points. However, the reality on the ground is very different.

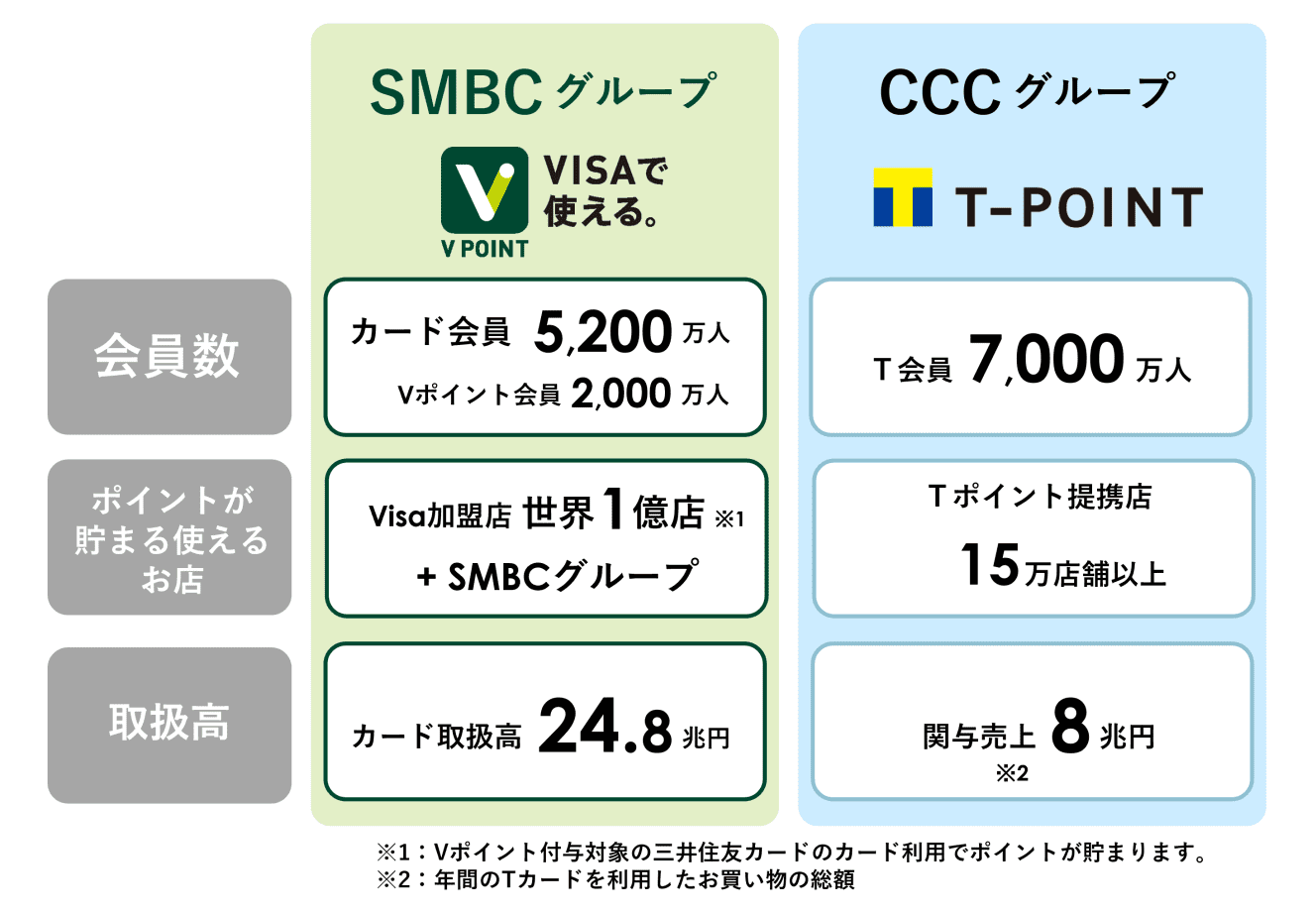

First, an “incident” will occur in February 2021. V-points, the points of Sumitomo Mitsui Card, suddenly became the fifth common point. Until then, V-points were merely points that could be earned through the use of Sumitomo Mitsui Card and transactions at Sumitomo Mitsui Banking Corporation (SMBC), and were circulated within the Sumitomo Mitsui Financial Group (SMBC Group). However, with the release of the “V-Points” application in February 2021, V-Points are now linked to Apple Pay and Google Pay.

This means that V-Points can be used for payment at any real store that is a member of Visa, which has roughly 100 million member stores worldwide. Therefore, in terms of the number of stores where V-Points can be used and the amount of payment, V-Points is not the fifth most accepted point, but the first of the five major common points. The release of the “V-Point” application was in the midst of the COVID-19 crisis, so it did not make a big splash, but this move will cause a tectonic shift in the power structure.

The “battle for supremacy” of common points is about to reach a climax.

In March 2022, SoftBank will leave the T Points camp. Until then, T Points had been earned through the various services of Yahoo! Japan, operated by Z Holdings, a SoftBank subsidiary, but a full switch was made to its own “PayPay Points “. At this point, the era of the six major common points had arrived, and T Points, the original common point system, found itself in a difficult position.

The battle for supremacy in the common point market seemed to have entered an unprecedented battle of wars, but on October 3, 2022, a surprising development occurred: a capital and business alliance between the SMBC Group and the CCC Group, which operates T-Point. The new company, in which the SMBC Group will hold 40% of the shares and the CCC Group 60%, is expected to manage the new point service. Based on the shareholding ratio, it is assumed that this capital and business alliance was initiated by the CCC Group in order to ensure the survival of T Points.

The timing of the integration and the name of the new point have not yet been decided, but within the next one to two years, the six major players will revert back to the five major players. The focus of the new points will be on the redemption rate. The V-point redemption rate for the regular card of Sumitomo Mitsui Card is 0.5%, which is lower than other common points. Probably, this part will not be changed and will land around +0.5% at the current T Point merchants. If realized, this will be a threat to the other camps, as some stores will be able to reach 1%.

It is “services that generate points” that will determine the power structure

So, which common points are promising in the future? The point to determine this is whether or not there is a service that allows a certain amount of points to be accumulated each month. This is a prerequisite for a service to become a common point. In the early days of T Points, there was TSUTAYA, a DVD rental company. T-points were accumulated for each rental, and it was commonplace to spend several thousand yen per month. Rakuten points are earned at Rakuten Ichiba (Rakuten Market ), and of course, cell phone charges are the source of points for mobile carriers.

Since cell phone bills are now as essential as utility bills, there is no room for hesitation and the main source of points is the carrier’s points, such as “d-points for docomo users. Therefore, the points of cell phone carriers were thought to be solid, but now a shadow of a shadow has begun to appear. In the past few years, cell phone rates have dropped dramatically, and the amount of points generated has been decreasing.

For example, until now, recharging “au PAY balance” with the “au PAY Card” has offered a 1% point reward, but from December 1, 2022, regular card recharge points will be eliminated. In addition, the 1% reward for using a d-card as the payment method for “d-payment” will be discontinued on December 10, 2022, and shifted to the “d-card payment benefit” with a 0.5% reward.

All of these are “major changes,” but looking at the three mobile carriers alone, PayPay’s basic redemption rate is low to begin with, so the situation is now, roughly speaking, on the same level as before. The benefit of double points for mobile payments has faded, and the rate of return for payments will converge to 1% for credit card payments. The recent trend toward deterioration of services, including other point services, has brought us to an era of low redemption rates.

Power of “credit card savings” over cell phone charges

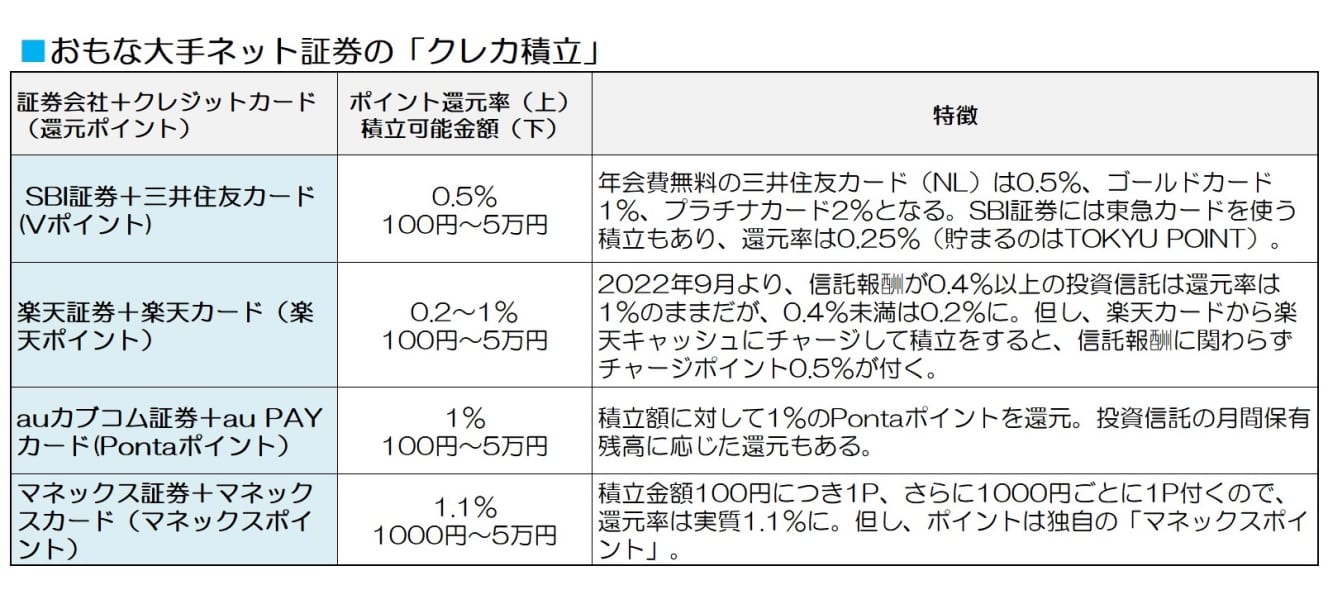

While the power of cell phone carrier points is waning, financial services are increasing their presence. More and more of them offer point redemption, and they are becoming a powerful source for generating new points. One of the most successful of these services is the “credit card savings account. Rakuten Securities introduced this service in 2018, and most major online securities firms now offer it.

Rakuten Securities has already set up more than 2 million credit card savings accounts. The total monthly amount of investment trust savings accounts exceeds 100 billion yen, and it is not surprising that 90% of these accounts are creditor savings accounts, given the trend of the amount set up. If we assume that the amount of credit card savings accounts set up is 90 billion yen, this would mean that 900 million yen worth of Rakuten points were being returned to users every month. The amount of savings is probably larger than the monthly cell phone bill for many of those who have set up accounts.

As far as we can tell, this credit card savings account is probably the most profitable of all the point-related financial services. Redeemed points can be reinvested in mutual funds and are highly investment efficient. It is no exaggeration to say that mutual fund savings is the “one choice” for asset building for the average individual, and asset management is a prerequisite, but the availability of credit card savings will become quite important when considering common points in the future.

The following is a list of major credit card savings plans offered by major online securities companies.

Campaign warfare may break out before the “New NISA” in 2024

Unfortunately, however, deterioration has begun here as well. I am sorry to say that after much agitation, it is Rakuten Securities. Shockingly, Rakuten Securities has been changing the rate of return on their investment trusts since September, depending on the level of trust fees, which is the cost of holding investment trusts. The “eMAXIS Slim U.S. Equity (S&P 500),” which is popular among individual investors, has a trust fee of less than 0.4%, so only 0.2% is attached. If you switch to saving with Rakuten Cash, you can get 0.5%, but this is down 0.5% from before. Until December 2022, the company is offering an additional 0.5% for saving with Rakuten Cash, for a total of 1% (there is also a backdoor way to charge Rakuten Cash at a discount, but we omit it here).

The table shows that the combination of “au kabu.com Securities + au PAY Card (Ponta Points)” is a step ahead, but the content of the service, including the reduction rate, can easily change depending on the situation. Rakuten Securities is also open to reviewing this service depending on the situation. Credit card savings can also be used for “NISA” (small amount investment tax exemption) accounts, and the “New NISA” will start in 2024. In the second half of next year, we may see campaign battles for the first time in a long time. It will be worth checking out what each company is up to.

DOCOMO Bank” and “LINE Bank” to be Established Soon

Let us take a look at other trends in the financial business of dpoints. First, d-points. Although there have been no significant developments recently, docomo has already announced that it will establish a joint venture with Mitsubishi UFJ Bank by the end of 2022 to launch a new digital account service. From reading the press release, it will be a “neo-bank” type of business that will not obtain a banking license, but will borrow the platform of Bank of Mitsubishi UFJ to provide banking services.

This tie-up is supposedly aimed at smoothing the distribution of users’ funds within the group, but it is hard to deny the sense of lapses. Docomo’s securities services include “Nikko Froggy + docomo” with SMBC Nikko Securities, which offers points for investment trust accumulation, but the rate of return is too low at 0.03% (no credit card accumulation).

The Softbank Group, which operates PayPay points, has two securities companies: PayPay Securities ( formerly One Tap BUY) and LINE Securities. Both are subsidiaries of the SoftBank Group, which holds more than 50% of the voting rights, so the hurdles to using the PayPay card and Visa LINE Pay credit card for credit card savings are not high. In particular, LINE Securities also supports the Nomura Mutual Aid System (TMNISA). However, both PayPay Securities and LINE Securities offer few products, making them less attractive. There is a possibility that they will expand their product lineup and release a credit card savings account before the start of the new NISA.

Incidentally, SoftBank holds a 51% stake in PayPay Securities and Mizuho Securities holds 49%, while LINE Financial holds 51% and Nomura Holdings, the holding company of Nomura Securities, holds 49% in LINE Securities. To complicate matters, LINE Financial plans to establish LINE Bank, a joint venture with Mizuho Bank, by the end of this fiscal year.

What will happen to nanaco points with “Seven Securities”?

Although not a common point system, there is an interesting move in “nanaco. Seven Bank, a Seven & i Group company, is expected to launch a securities service in partnership with Smart Plus. Seven Bank itself will not obtain a license to engage in the securities business, but will be able to invest in stocks using the platform of Smart Plus, a securities company.

The biggest advantage of this tie-up is that it will allow investors to invest in stocks directly with the money in their Seven Bank accounts. You may think, “What a big deal,” but the significance of the “integration” of bank account and securities account is not small. In the past, in order to facilitate the smooth transfer of funds between bank accounts and securities accounts, large-scale measures were taken, such as the establishment of a banking subsidiary by a securities company, or the establishment of a securities subsidiary by a bank to link the two. This was easily accomplished by incorporating securities services into banking services. For the time being, they do not seem to offer mutual funds, but it will be interesting to see if they will offer a service that earns nanaco points.

Interview and text: Kenji Matsuoka

After working as a money writer, financial planner, and market analyst for a securities company, Matsuoka became independent in 1996. He writes articles on finance and asset management mainly for business and economic magazines. Author of "A Textbook for the First Year of Robo-Advisor Investing" and "A Book of Understanding with Abundant Illustrations! A book that will definitely benefit you with cashless payment". He is also a credit card guide for the information site "All About.